SMM7 March 3: most of the non-ferrous metals market performed well this week. Shanghai Copper and Shanghai Nickel continued to rise this week, of which Shanghai Copper once rose to 49570 yuan / ton, a high in nearly six months. from a fundamental point of view, supply-side disturbances intensified. Recently, all smelting operations in Chile's national copper Chuquicamata mine have been temporarily suspended, and the epidemic situation in the country is grim, and copper stocks continue to decline at present. Although July-August is the off-season for wire and cable consumption, it is also expected by the market; while the supply-side disturbance continues, the tight pattern of copper supply and demand remains unchanged, forming a continuous strong support for copper prices. In addition, shanghai nickel suddenly rose on Friday, up more than 3% during the day, shanghai tin continued to rise slowly, shanghai lead rose and fell, shanghai zinc continued to shake.

In terms of nickel, the US reported a sharp increase in ADP employment, and EIA crude oil inventories fell more than expected this week, while US non-farm data once again boosted sentiment in the nickel market, with nickel prices rising sharply in Shanghai and Lun in early trading on Friday. However, the weak fundamentals of the nickel market have not been improved at present. With the arrival of the off-season downstream of stainless steel from July to August, domestic demand is weak and lack of obvious benefits, and the industry is generally pessimistic about the late market. Stainless steel profits are poor and the late supply of nickel pig iron in Indonesia continues to increase, under the influence of this recent nickel pig iron market shows a slight weakening trend. Nickel spot trading is still poor, high nickel prices shock so that traders do nothing. Technically, if Shanghai Nickel cannot effectively repair the jump gap of 106000 yuan / ton above, it will still hold the firm above the 100, 000 mark, and the market will still be viewed as a range shock in the short term.

Copper:

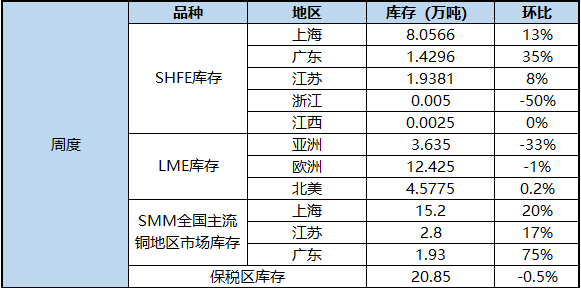

The epidemic in South America has not been effectively controlled, and the supply of mines will continue to be at risk in the future. Due to the massive inflow of imported copper into China this week, social inventories in the three places increased by 37300 tons to 199300 tons month-on-month, and domestic social inventories rose for the first time since mid-March. The price difference of fine waste has widened to more than 2000 yuan / ton, it is difficult to sell refined copper rods, scrap copper continues to squeeze refined copper consumption, and high copper prices also restrain the purchasing rhythm of copper downstream. This week, the discount for electrolytic copper goods has fallen rapidly from RMB190RMB / ton last week to the lowest discount of RMB10 / ton. At present, the import window has been closed, the inflow of imported copper will decrease next week, and the domestic stock accumulation is expected to decrease compared with the previous week, but the seasonal off-season superimposed scrap copper consumption is strong, and the domestic short-term accumulation trend is difficult to change. Global inventories continue to decline, the logic of low inventories continues, global capital easing and the stable performance of domestic economic consumption will continue to be the two strong supports of copper prices. Copper prices will remain strong in the short term. Next week, Lun Copper is expected to run at US $6200 per ton, while Shanghai Copper will run at RMB 50,000 per ton at 48600.

Aluminum:

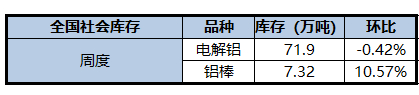

The arrival of goods increased significantly, with aluminum rod inventory increasing by 6900 tons to 73200 tons compared with last Wednesday. Inventory in Wuxi, Changzhou, Huzhou and Nanchang all increased to varying degrees, only inventory in Foshan continued to decline. SMM statistics domestic electrolytic aluminum social inventory fell by 3000 tons to 719000 tons compared with the previous Wednesday.

Lead:

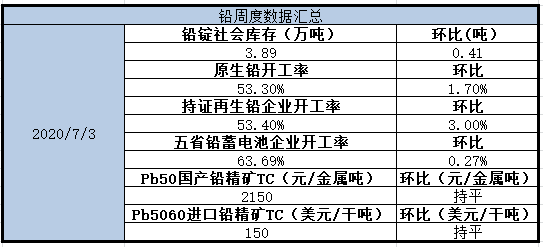

In terms of lead fundamentals, the market expects the supply of delivery to be close to 20,000 tons, the smelter's current spot discount is gradually expanding, and social inventory continues to accumulate. From the traditional trading logic of lead, lead fundamentals are relatively weak, but due to low lead precipitation funds and serious capital control, it is not ruled out that the main funds will continue to enter the market to drive up prices in the short term, so from the perspective of lead fundamentals, the current high level is more likely to fall.

Zinc:

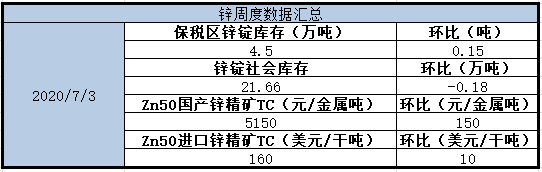

In terms of Shanghai zinc, Shanghai zinc maintained a range of shocks this week. The performance of overseas employment data is eye-catching, and the macro mood has obviously picked up, but the boost for Shanghai zinc is relatively limited, mainly because the fundamental support is still weak. Next week, with the increase in domestic zinc concentrate supply, smelters' raw material stocks rebounded. Under last week's mining and metallurgical negotiations, zinc concentrate processing fees were raised for the first time in a year, with local increases of around 100m / t, boosting smelters' willingness to produce. In addition, Xing'an copper and zinc production resumes, Chifeng medium color enters the overhaul, and imported zinc is affected by ratio downwards. it is expected that it will be difficult to increase the inflow of imported zinc next week, which is basically the same as this week, so on the whole, the increment on the supply side is still greater than the reduction. From the consumer point of view, with the end of the rush brought by the semi-annual report, the orders of most galvanized enterprises fell, the start of galvanized sheet enterprises was relatively stable, the orders of galvanized pipe and other structural enterprises were more differentiated, and the profits of small and medium-sized enterprises were poor; alloy enterprises weakened again, the smelter squeezed orders and domestic demand came together, and the orders remained weak. The zinc oxide plate is stable and good, and the warming of the automobile plate drives the zinc oxide enterprises to start work. On the whole, there is still no bright spot on the consumer side. From a technical point of view, the lower 20-day moving average support is stronger, but the MACD index is about to become a dead cross, indicating that Shanghai zinc may have downward momentum. Although the fundamentals are weak, the macro positive mood is strong, and it is expected that Lun Zinc may fluctuate in the range of the 20-day moving average. Overall, Lun Zinc is expected to run at US $2,050 per ton next week; 2008 of the main contract for Shanghai Zinc is expected to run at 16550 Mel 17150 yuan / ton, and the spot side is expected to raise water around 40 Mel 80 yuan / ton in July.

Nickel:

During the week, the nickel price basically fluctuated around the previous position, and the fundamentals were weak but mostly known news, such as the increase in the supply of nickel pig iron and the pressure on stainless steel market shipments in the off-season, etc., on the whole, the short-term contradiction is not obvious; in the macro aspect, some overseas data are bright, and in the major links, we can see that overseas countries are still following the logic of consumer recovery, coupled with the fact that national policies support enterprises to a certain extent, and the macro side is relatively preferred. Under the comprehensive action, the nickel price fluctuates in the range. Due to the sharp rise in nickel prices on Friday, and there are no obvious positive factors in the fundamentals, including the protest by residents near Weda Bay on Friday, which seems to be hyped, the effect on the market may be limited, and the mindset of shorting when going high is obviously enhanced.

On the inventory side, as of Friday, inventories in the first phase of the week increased by 431 tons to 29422 tons, with the increase still coming from delivery depots in the Shanghai area. Due to poor trading in the spot market, the willingness of the holder to deliver the position is still strong. In terms of hidden inventory in East China, there are nearly 500 tons of nickel beans in storage this week, and the current inventory of nickel beans is about 3900 tons; on the other hand, after some spot nickel plates are shipped to the delivery warehouse, some of the pre-holiday transactions are overlaid and released one after another this week. as a result, the overall hidden inventory in East China has dropped by 849 tons to 12622 tons. There is still little trading in the bonded area, but after the arrival of the long-term goods in Hong Kong, there has been a small increase of 100 tons to 16100 tons. It is reported that there will be more than a thousand tons of nickel board customs clearance next week, domestic inventory may be accumulated again.

Tin:

This week Shanghai tin 2009 contracts showed an overall upward trend of concussion. At the beginning of the week, tin opened at 137920 yuan / ton in Shanghai. At the beginning of the week, weak demand in the lower reaches of the week pulled down spot prices. Futures prices fell somewhat, reaching the lowest point of 136680 yuan / ton in the week, and then bottomed out. Bulls entered the market, giving up the decline and rising at the beginning of the week. The horizontal market fluctuated in the middle of the week, and its bulls continued to enter the market on Friday from the night market, reaching a weekly high of 140240 yuan / ton in the morning. After briefly breaking the pressure level of 140000 yuan / ton, it fell back to close at 139790 yuan / ton. The weekly level rose 1700 yuan / ton, or 1.23%, with 116000 hands traded and 29161 positions, an increase of 25521 hands. During the week, the main force of tin in Shanghai is positive, the physical part is above all weekly lines, and the lower shadow line is supported by the 5-week moving average. In terms of indicators, the opening of weekly MACD indicators is still upward, while that of daily MACD indicators is downward, but there is a trend that the two lines intersect and form a golden fork. The daily and weekly K lines are close to the upper track of the Bollinger belt. By today's close, Shanghai tin returned to the high level of the platform before the return year, because the gap of the decline in the epidemic has been basically made up, and the downside space is limited in the short term. Bulls continue to enter the market today, considering its position cost, it is expected that the upper pressure will be near the year-ago high of 140500 yuan / ton in the short term.

The spot price of Shanghai and tin as a whole showed a fluctuating upward trend this week. Affected by weak demand at the beginning of the week, the uplink was weak, downstream transactions warmed up, and a small amount of inventory. Then the average price rebounded to around 139250 yuan / ton following the futures, and in the middle of the week, the horizontal plate fluctuated, the center of gravity did not deviate greatly, and the spot price remained stable. Because the price is at a high level, the transaction atmosphere in the spot market is weak, and the willingness to receive goods downstream is general. Purchase on demand. To Friday, prices rebounded, the average price rose to 140250 yuan / ton, downstream enterprises are more willing to receive goods, the market turnover is light. Overall, the trading atmosphere in the one-week tin spot market in Shanghai is weak. The price quoted on Friday is 138000Lue 141,500 yuan / ton, with an average price of 140250 yuan / ton, up 750 yuan / ton from last Wednesday's price. In terms of liter discount, due to the continuous rise in tin prices superimposed by downstream fear of high demand, the overall liter discount this week has dropped significantly compared with last week, Yunxi has dropped from 2500mur3000 yuan / ton to 1000mur1500 yuan / ton, ordinary cloud word from 1500 yuan / ton to 1000 yuan / ton, small brand from 500 yuan / ton to near level water.

2020 China Ni-Cr stainless Steel Industry Market and Application Development Forum

Scan the QR code, apply for participation or join the SMM metal exchange group