SMM 2020/7/2:

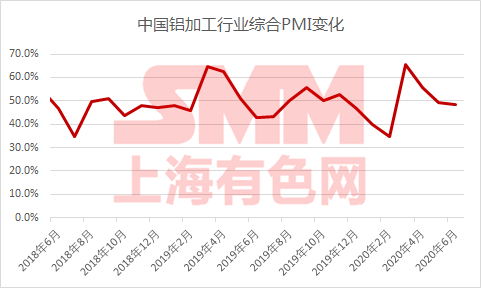

According to the statistics of SMM survey, the composite PMI of China's aluminum processing industry was 48.3 in June, down 0.9 percent from the previous month, 5.4 percent from the same period last year, and a decline for three consecutive months up to June. The details are shown in the following figure. According to the overall situation of the survey, it is expected that the comprehensive PMI of the aluminum processing industry in July is still below 50.

Source: SMM

Take a look at the sub-sections:

Aluminum strip: the comprehensive PMI of aluminum plate and strip was around 44.17 in June, which was 2.9% higher than that in May. According to the feedback of aluminum plate and strip enterprises, due to the support of the backlog of orders, the overall operating rate was stable in June, but the new orders did not rebound sharply in June after the gradual reduction in late May, and the market demand in June was obviously lower than that in April-May. In terms of product structure, orders for building-related plates and strips such as PS plates and decorative panels in June are relatively stable, automotive plates are still weak, and order feedback for cans and ring materials is good, due to the weather entering the summer, the demand for beer and beverage increases, and the demand for related plates and strips increases accordingly; in terms of domestic and foreign trade, the lack of stamina of domestic trade began to decline, although foreign trade orders did not increase significantly, but they did not further deteriorate. In terms of inventory, because the aluminum price in June is higher than that in May, the downstream buyers are afraid to buy goods, and the inventory level of raw materials is slightly lower than that in May, and the high aluminum price affects the enthusiasm of picking up goods downstream, and some manufacturers report that the inventory of finished products has increased. With regard to the situation in July, considering that it is difficult for the aluminum strip market to pick up during the off-season of traditional consumption, PMI is expected to remain below 50.

Aluminum foil: the composite PMI of aluminum foil in June was around 64.45, which was 2.66% higher than that in May. The aluminum foil industry recorded a rebound, mainly due to the increase in market demand for products such as air-conditioning foil, food soft package foil and container foil after the summer, and the increase in new orders and backlog orders for large aluminum foil companies in Jiangsu and Hunan, resulting in an increase in operating rate. but other products such as battery foil and electronic foil are still weak. Part of the feedback from export enterprises, although the epidemic affected foreign demand, but with the resumption of the foreign economy, the decline in foreign orders significantly narrowed, and the export of food foil container foil enterprises was not greatly affected in summer. In addition, the enterprise feedback, due to the low aluminum prices in April-May has been part of the hoarding, in the context of the current high aluminum prices, do not tend to continue to hoard goods, buy goods to become cautious, raw material inventory slightly lower than in the previous period. In terms of the situation in July, it is expected that the prosperity of the aluminum foil market will remain stable, and the probability is still above the boom and bust line.

Building profiles: in June, the PMI of building profiles decreased slightly compared with the previous month. The output of some enterprises reached a high in April and May, while six production declined. Many enterprises reported that the backlog of orders and new orders also decreased significantly in June, summer demand seasonally weakened, and production continued to decline in July. In terms of inventory, enterprises need to settle accounts at the end of the month and half a year, it is slightly difficult for project customers to pay back, products are actively delivered so as not to take up too much money, raw materials are affected by rising aluminum prices, and more on-demand stock is available. Procurement and inventory have also been reduced.

Industrial profiles: PMI of industrial profiles weakened month-on-month in June. After a strong rebound in May, the persistence of orders was insufficient, the increment of new orders for industrial profiles such as rail transit, photovoltaic, 5G, and automobiles declined, and exports also performed poorly under the impact of the second outbreak of overseas epidemics. Inventory is stable and slightly lower, and enterprises continue to adjust according to orders. The situation of enterprises of different sizes is divided, and the orders of a small number of large enterprises are good, while the production and sales of some small and medium-sized enterprises are relatively unsatisfactory, and the expectation for July is slightly pessimistic.

Aluminum cable: the PMI index of aluminum cable in June was 47.7, down 5.4 percent from May. According to the research, cable enterprises still give priority to the production of pre-year orders in June, but some enterprises report that near the end of the month, 90% of the national grid tender orders received since the end of last year have been basically completed, and the current problem is that the performance of new orders is inadequate. as the national network did not publish a large number of UHV-related tenders in the first half of the year, the amount of other newly announced aluminum bids is relatively small. The operating rate of the cable industry in June is basically the same as that in May, because next month's production is mainly orders received after March this year, and it is expected that the operating rate will decline in July. In addition, due to the concentrated delivery date for the national network's early orders from May to June, the enterprise said that the inventory of finished products decreased in June. In terms of raw materials, because there are many cable companies to maintain value, and aluminum prices are high, downstream more on-demand procurement, hoarding awareness is not strong. Taken together, the cable PMI is expected to remain below 50 next month.

Recycled aluminum alloy: in June, the PMI of the recycled aluminum industry remained below the rise and fall line, while PMI remained slightly at 46.7%. After entering June, the supply of waste aluminum is no longer the biggest factor affecting the rebound of the operating rate of recycled aluminum enterprises, due to weak demand at home and abroad, coupled with the impact of imported aluminum alloy ingots, the output of domestic enterprises continues to decline. From the overall consumption point of view, July is the traditional off-season of the recycled aluminum industry, more than half of the enterprises expressed concern about new orders in July, while the implementation of the new standard of imported waste aluminum is still unclear, the impact of imported aluminum alloy ingots in July is still not to be underestimated, and it is expected that the PMI of the recycled aluminum industry will continue to be below the line of prosperity and decline in July.

Primary aluminum alloy: due to the reduction of production in some factories, the primary aluminum alloy PMI fell back below the rise and fall line to 42.2 in June, a decrease of 10.1% compared with the previous month. Fear of high aluminum prices and concerns about future demand have led downstream aluminum wheel factories to purchase cautiously, while alloy factories that sell and target production have cut production accordingly. The export of aluminum wheels on the demand side has not yet recovered, and the domestic vehicle factory will take a high-temperature vacation for two weeks from July to August, and most wheel factories also have plans to reduce or stop production, so the reduction of demand for primary aluminum alloy in July is a high probability event, and it is expected that the original aluminum alloy PMI will continue to be below the rise and fall line next month.