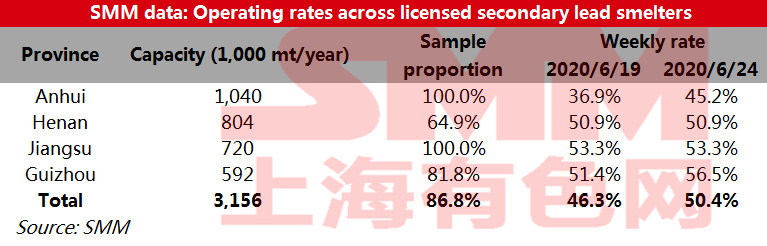

SHANGHAI, Jun 24 (SMM) – The average operating rate across licensed smelters of secondary lead in major producing areas edged up this week, driven by the resumption of work at Anhui Dahua and Guizhou Jinlong. Tight supply of feedstock battery scrap, however, continued to cap any increase in operations in Henan and Jiangsu.

An SMM survey showed that operating rates across licensed smelters of secondary lead in Jiangsu, Anhui, Henan and Guizhou averaged 50.4% in the week ended June 24, up 4.1 percentage points from the previous week.

The respective rates in Henan and Jiangsu held unchanged on the week at 50.9% and 53.3%, as the shortage of battery scrap prevented local smelters from ramping up production.

The average operating rate in Anhui stood at 45.2%, 8.3 percentage points higher from a week ago, lifted by a rise in daily output at Anhui Dahua.

In Guizhou, Jinglong smelter finished maintenance and normalised production, raising the average operating rate in Guizhou by 5.1 percentage points on the week to 56.5%.

![SHFE lead 2607 traded above the daily average line intraday, recording a three-day winning streak [Lead Brief Review]](https://imgqn.smm.cn/usercenter/yqTpQ20251217171721.jpeg)

![[SMM Sulfur Flash] Spot Sulfur Transactions Slide, Shandong Refinery Quotes Decline](https://imgqn.smm.cn/usercenter/HhNHP20251217171708.jpg)