"SMM rare Earth Weekly report" released, the weekly report SMM will select one of the hot topics, prices, market or major changes in the industrial chain information released into a document for your reference.

The prices of rare earth products have been mixed this week. In terms of light rare earths, the market turnover of praseodymium-neodymium oxide this week is lower than that of last week, and the inquiry order and the actual transaction situation are generally weak. Due to the market demand upstream merchants gradually cut prices, praseodymium neodymium oxide prices gradually fell, Friday praseodymium neodymium oxide quotation 26.6-269000 yuan / ton. In terms of medium and heavy rare earths, the prices of dysprosium oxide and terbium oxide rose sharply this week compared with last week. The recent acquisition and storage expectations have attracted much attention from the market. Myanmar's ionic rare earth ore imports are relatively low compared with the same period last year, and the market is expected to maintain a relatively low level of ionic rare earth ore imports that may be caused by the upcoming rainy season in Myanmar, the impact of tightening of rare earth mineral raw material supply and market storage expectations, upstream merchants actively raise quotations, market enquiries and transactions have warmed up. Dysprosium, terbium prices are supported by the actual transaction situation, the performance is relatively strong and rising day by day. Dysprosium oxide 193-1.95 million yuan / ton and terbium oxide 415-4.2 million yuan / ton on Friday.

"apply for free access to the SMM metal industry chain database

Catalogue of "SMM rare Earth Industry chain Weekly report" in this issue

Main points of this issue's weekly report

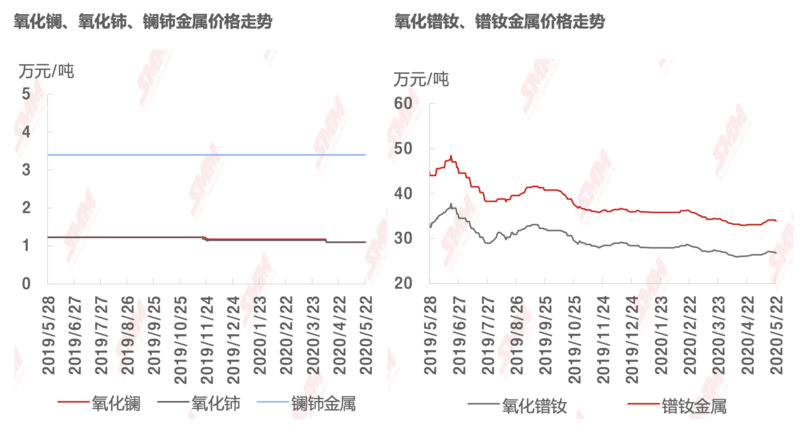

Prices of major rare earths in China

Market Review and Forecast: rare Earth prices this week (5.19mur5.23) and next week's Forecast

Hot spots in rare Earth Industry

Political policy

Scan the QR code application report for free and join the SMM rare earth industry chain exchange group

The contents of the "SMM China rare Earth Industry chain routine report" include: market review and forecast, rare earth industry hot spots, overseas market hot spots, rare earth upstream and downstream industry hot spots, political policies, weekly update interpretation of hot events, focusing on the contradictions that have changed greatly during the week. "View details

![Tight Supply and Recovering Demand Drove Magnesium Prices to Rise Steadily This Week, Breaking Above 17,500 [SMM Magnesium Weekly Review]](https://imgqn.smm.cn/usercenter/xLlnY20251217171724.jpeg)