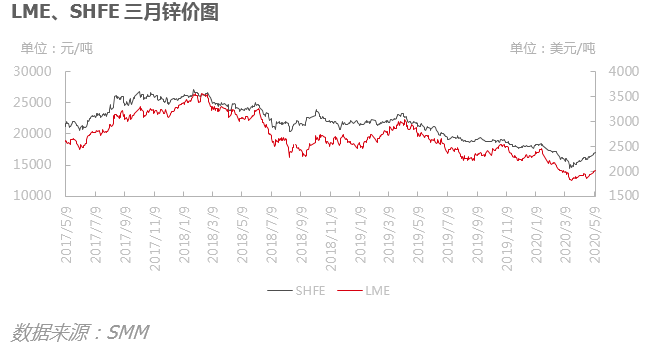

SMM5 month 12: since mid-April Shanghai zinc shock upward, the trend is relatively strong, the performance is better than Lun zinc. In mid-April, demand continued to recover in the lower reaches of the country, especially in the case of infrastructure orders, which led to the continuous degeneration of domestic inventories. At the same time, the price technology was supported by the 5-and 10-day moving averages, the lower support was rammed, and the main contracts fluctuated higher. After repeated explorations, the price broke 16000 yuan / ton. After the May Day holiday, the global multi-regional plan began to restore the economy in May, and the market expectations for demand recovery were strengthening. at the same time, due to tight mine supply in May and June, smelters increased their willingness to enter the market ahead of time, and their willingness to enter the market was strong, driving zinc prices to increase their positions. Shanghai zinc three even Yang trend was strong, once broke through the 17000 yuan / ton integer barrier, and the price recovered all the decline since March. SMM believes that for zinc, zinc prices will remain strong due to the reduction of mines and the continuation of the recovery of consumption. In the medium term, it is necessary to guard against the fact that after the rebound of zinc prices, mines may increase sales of zinc mines, resulting in reduced pressure on refinery raw material stocks.

Selected contents of monthly report

Zinc price monthly forecast: in May, the impact of overseas mining enterprises has not yet ended, although the Peruvian government has allowed domestic mining enterprises to resume production, but due to difficulties in the resumption of staff and other problems, Peruvian mines have not yet seen a restart, superimposed cross-border transport still has an impact, it is expected that the global zinc mine will still be scarce in May. At present, there is a shortage of raw materials in smelters in overseas countries. If the impact of the mine continues, the problem at the end of the mine will be transmitted to the smelting end. On the demand side, after Europe, the United States, Japan and other countries have successively issued plans to relax the blockade and restart the economy, and European and American car companies have also entered the resumption of work and production, the market has picked up expectations of demand recovery. In summary, for Lun Zinc, the short-term supply and demand structure has changed, the supply shortage superimposed global demand will gradually recover, driving the market bullish sentiment is becoming stronger, it is expected that Lun Zinc will maintain a strong shock, and the internal and external price ratio is expected to narrow slightly.

As far as domestic supply is concerned, in April, mining enterprises have gradually resumed work and production. However, due to the large decline in zinc prices in the early stage, some mines are in a state of loss, resulting in the weakening of the willingness to ship the mines. Some mines only produce and do not sell or reduce sales to force smelters to lower processing fees, and domestic minerals are still in short supply. For refineries, in April, with the supplement of imported mines in the early stage, mainly resumed production and increased production, refined zinc production still recorded an increase of 13000 tons. In May, the impact of the overseas epidemic will gradually emerge, the amount of imported minerals will be lower than in April, the larger drop in superimposed processing fees has led to the compression of refinery profits, and some refineries have advanced this year's maintenance plan to May-June. Refined zinc production is expected to fall slightly in May compared with the previous month. On the demand side, the demand of various plates was divided in April, in which the overall operating rate of galvanized enterprises rose to a high level under the recovery growth of demand, in which engineering orders continued to improve; die casting zinc alloy enterprises suffered from the loss of export orders, the overall order was significantly weaker, compared with the operating rate in March, there was a V-shaped reversal; and the operating rate of zinc oxide enterprises remained low shock, the overall decline compared with the same period last year. In May, under the power of infrastructure projects, galvanizing needs to maintain a high level, and the improvement of car sales data may lead to its related downstream consumption. It is expected that domestic zinc consumption will remain in May, driving social inventory to continue to go to the warehouse. However, after the rebound of zinc prices is stronger, the willingness to receive goods downstream is weaker than in the previous period, or lead to a slowdown in the intensity of going to the warehouse. That is to say, for zinc, due to the reduction of the mine end and the continuation of the recovery of consumption, zinc prices will remain strong; in the medium term, it is necessary to guard against the rebound of zinc prices, mines may increase sales of zinc mines, resulting in the reduction of refinery raw material inventory pressure.

"Click to view the SMM zinc industry chain database

More:

Summary of SMM Zinc concentrate Industry data

SMM zinc refining industry data summary

The sustained domestic performance of the rebound in zinc prices in the two cities is more eye-catching.

Operating rate of domestic zinc concentrate enterprises

Comparative chart of zinc concentrate production in 2019 and 2020

Average inventory days of raw materials in zinc smelting enterprises

Operating rate of domestic zinc refining enterprises

Monthly operating rate of Top 20 Zinc Refining Enterprises

Zinc Social inventory in Shanghai, Guangdong and Tianjin

Monthly operating rate of galvanizing enterprises

Monthly operating rate of Die casting Zinc Alloy Enterprises

Monthly operating rate of zinc oxide enterprises

Downstream raw material inventory level

"Click order to view the details of the report

In 2019, global trade disputes escalated, the global economy was under pressure, and central banks began a wave of interest rate cuts. At the same time, the meeting of the political Bureau of the CPC Central Committee stressed that at present and for some time to come, the basic trend of China's economic stability and long-term improvement has not changed, and 2020 is also the year for China to build a well-off society in an all-round way and the end of the 13th five-year Plan. Against this background, the new crown virus is raging all over the world, and how to achieve stable economic growth in China is worth looking forward to.

In the zinc market, overseas mines will increase production step by step in 2019, but the increase in domestic mine production will be repeatedly hindered. In the first quarter of 2020, zinc prices fell through the mine cost line, mine profits plummeted, and how smelters and mine profits will be distributed in 2020. can overseas mines be expected to be put into production under the disturbance of the epidemic situation? In addition, the output of domestic zinc refining smelters broke through the bottleneck and set a new record in 2019, but under the disturbance at the supply end of zinc mines in 2020, can the capacity utilization rate of smelters maintain a high load? Whether the infrastructure investment under the tone of "stabilizing the economy" in 2020 can exceed the expected performance, whether the super-seasonal performance of the galvanizing industry can still be expected, and whether the contradiction between supply and demand of zinc may reverse in 2020, paying attention to and laying out structural opportunities is another option. Can zinc prices pick up in 2020?

In view of the above topics, SMM will invite industry bigwigs, industry professionals, upstream and downstream enterprises of the industry chain to hold the "2020 (15th) lead and Zinc Summit" in Changsha to discuss the current situation and problems faced by the industry, as well as future development prospects, and analyze the fundamentals and the future trend of zinc prices.

"Click to sign up for SMM" 2020 (15th) lead and Zinc Summit

Scan the QR code in the picture to sign up for the lead-zinc summit and fill in the personal information on the last page. The meeting staff will contact you later!