Price of SMM lead products on May 11th

May 11 SMM domestic well-known recycled lead enterprises waste battery procurement quotation

May 11 SMM lead Market Trends

Shanghai market Jinsha lead 14105-14145 yuan / ton, Shanghai lead 2006 contract price 260-300 yuan / ton, Wuxi market south lead 14095-14125 yuan / ton, Shanghai lead 2006 contract 250-280 yuan / ton quotation. Lead weak decline, and due to the spot market circulation supply increase, primary lead and recycled lead factory shipment discount expansion (to SMM1# lead average price), the downstream just need to favor this kind of supply, the holder quotes the water to cut by half compared with last week, still obtains the partial transaction.

South China lead in Guangdong market is 14100 yuan / ton, the average price of SMM1# lead is up 50 yuan / ton. Henan Yuguang, Wanyang and other smelters are mainly Jiaochang single, Jinli, Wanyang 14000 yuan / ton, the average price of SMM1# lead discount 30 yuan / ton (traders); Hunan Shuikoushan 14100 yuan / ton, the average price of SMM1# lead rose 50 yuan / ton; Hunan Jingui 13950 yuan / ton, the average price of SMM1# lead discount 100 yuan / ton. Jiang copper 14150 yuan / ton, SMM1# lead average price flat water quotation. Yunnan small factory 13800 yuan 13850 yuan / ton, the average price of SMM1# lead discount 200 yuan 250 yuan / ton quotation. Today, the price of loose orders in the market continues to fall, and trading in the primary lead market is light, and the market is dominated by recycled lead trading.

Shanghai lead weak shock, waste battery quotation is difficult to follow the lead price, recycled lead market trading in general, among them, including tax recycled lead mainstream transaction price of SMM1# lead discount 150-200 yuan / ton factory, some areas quoted to the SMM1# lead average price discount 250 yuan / ton or more, compared with the beginning of last week has expanded.

The terminal consumption of electric battery market is light, most dealers are not optimistic about the future, procurement depends on demand, and the other main model 48v12Ah is maintained at 220 Mel 240 yuan / group.

In 2019, global trade disputes escalated, the global economy was under pressure, and central banks began a wave of interest rate cuts. At the same time, the meeting of the political Bureau of the CPC Central Committee stressed that at present and for some time to come, the basic trend of China's economic stability and long-term improvement has not changed, and 2020 is also the year for China to build a well-off society in an all-round way and the end of the 13th five-year Plan. Against this background, the new crown virus is raging all over the world, and how to achieve stable economic growth in China is worth looking forward to.

In the zinc market, overseas mines will increase production step by step in 2019, but the increase in domestic mine production will be repeatedly hindered. In the first quarter of 2020, zinc prices fell through the mine cost line, mine profits plummeted, and how smelters and mine profits will be distributed in 2020. can overseas mines be expected to be put into production under the disturbance of the epidemic situation? In addition, the output of domestic zinc refining smelters broke through the bottleneck and set a new record in 2019, but under the disturbance at the supply end of zinc mines in 2020, can the capacity utilization rate of smelters maintain a high load? Whether the infrastructure investment under the tone of "stabilizing the economy" in 2020 can exceed the expected performance, whether the super-seasonal performance of the galvanizing industry can still be expected, and whether the contradiction between supply and demand of zinc may reverse in 2020, paying attention to and laying out structural opportunities is another option. Can zinc prices pick up in 2020?

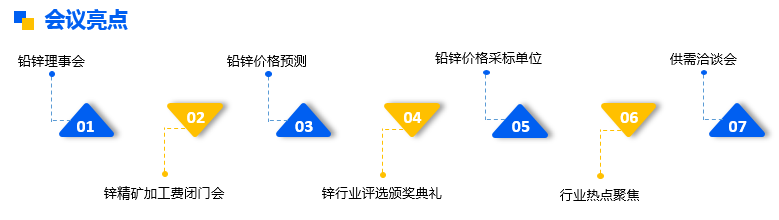

In view of the above topics, SMM will invite industry bigwigs, industry professionals, upstream and downstream enterprises of the industry chain to hold the "2020 (15th) lead and Zinc Summit" in Changsha to discuss the current situation and problems faced by the industry, as well as future development prospects, and analyze the fundamentals and the future trend of zinc prices.

"Click to sign up for SMM" 2020 (15th) lead and Zinc Summit

Scan the QR code to sign up for the lead and zinc summit and fill in the personal information at the end of the page, and the conference staff will contact you later!