SMM4, March 2: at the White House New Crown virus epidemic Information Conference on March 31, Trump's speech means the end of globalization; the United States will gradually become a self-sufficient country independent of the global supply chain in the future. "We should never rely on foreign countries as our own means of survival," he said. The crisis highlights the importance of strong borders and prosperous manufacturing. Over the past three years, we have built a sound immigration system and brought manufacturing back to the United States. Now, the two parties must unite to build the United States into a fully independent and prosperous country: energy independence, manufacturing independence, economic independence, and sovereign independence of national boundaries. The United States will never be a dependent country. It will be a proud, independent and self-reliant country. The United States will advance business, but will not rely on anyone. "

In addition, recently, the top political and economic scholars in many countries have studied and judged the pattern of the post-epidemic world, and they all mentioned that the global industrial chain will be reintegrated. Their argument is that the fundamental impact of the new crown outbreak on the world financial and economic system is to raise awareness that global supply chain and distribution networks are extremely vulnerable. Globalization enables enterprises to organize production around the world and put their products on the market in a timely manner, thus reducing warehousing costs. If inventory is shelved for more than a few days, it will be considered a market failure. The supply is carefully designed to be procured and transported on a global scale. The new crown virus has proved to the world that pathogens can not only infect humans, but also destroy the entire real-time production system. Given the scale of the global losses in financial markets since February, companies are likely to emerge from the epidemic with a conservative approach to real-time production and global decentralized production. The result is that global capitalism is likely to enter a dramatic new phase: to avoid future damage, the supply chain will be closer to home and full of surplus.

However, I am personally skeptical of this view, especially for the Chinese market. As Huang Qifan said recently: China's manufacturing industry now accounts for 30% of China's GDP and nearly 30% of the global manufacturing industry. Although China is called the factory of the world, the quality of manufacturing development has not been subject to the original division of labor in the global industrial chain. Since March, the situation of resuming production in China's manufacturing industry has been uneven, and many enterprises have been unable to resume production or even face closure due to the disappearance of orders from Europe and the United States. However, we can see that some enterprises have not only not dropped their orders, but also experienced relatively large growth, such as the electronics manufacturing industry in Suzhou, Chongqing and other places. The fundamental reason is that industrial chain clusters have been formed in these places, and more than 80% of the supporting components related to electronic manufacturing are produced locally. This clustered production model reduces the risk of purchasing parts from around the world and highlights its competitiveness during the epidemic. In other words, those industries that are relatively complete in China's industrial chain clusters will produce order growth in this epidemic, and some multinational companies will also transfer orders originally intended to be produced in Europe, Asia, and other countries to such factories in China. Therefore, industrial chain clustering is an important feature of the global industrial chain reconstruction in this epidemic. The industrial chain cluster that China has formed or is about to form is the basis to attract the global high-end manufacturing industry chain to settle in China.

So for the copper industry, will it also lead to a major change in the global industrial chain as a result of the epidemic?

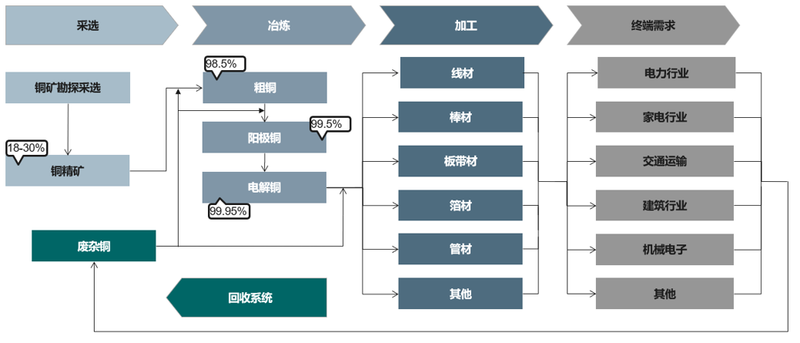

First of all: let's take a look at the division of the copper industry chain: mainly divided into mining, smelting, processing and terminal requirements.

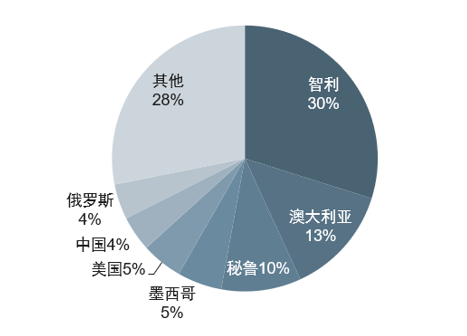

Secondly, the distribution of copper mines in the world:

Global copper mineral reserves are about 700 million tons (metal tons), mainly distributed in Chile (30 per cent), Peru (10 per cent), Australia (13 per cent), Mexico (5 per cent) and China (4 per cent). There are 11 top copper deposits (copper metal reserves ≥ 30 million tons) in the world, of which 6 are distributed in Chile and the rest in Indonesia, Mongolia, the United States, Russia and Australia.

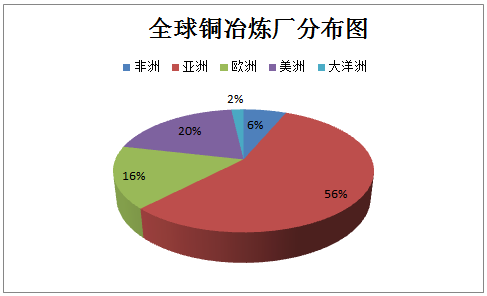

Third: global distribution of copper smelters:

In 2019, the global output of electrolytic copper was about 23.45 million tons, mainly distributed in Asia (55.9 per cent), with 8.94 million tons in China (68.2 per cent in Asia and 38.1 per cent in the world) and about 4.6 million tons in the Americas (19.6 per cent), of which the United States accounted for 1.15 million tons (25 per cent in the Americas and 4.9 per cent in the world). Chile accounted for 2.21 million tons (48.2 per cent in the Americas and 9.5 per cent in the world) and Europe (16.3 per cent) was about 3.83 million tons, with a total of 8.2 per cent in Africa and Oceania.

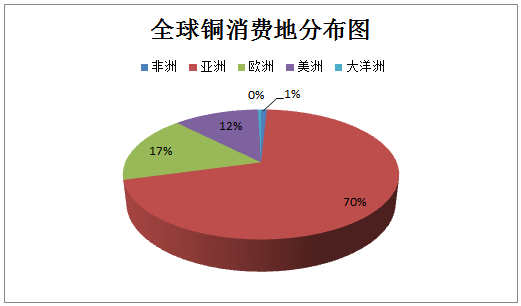

Finally: distribution of global copper consumption:

The global consumption of electrolytic copper in 2019 was about 23.46 million tonnes, mainly distributed in Asia (70.2 per cent), with 12.48 million tonnes in China (75.8 per cent in Asia, 53.2 per cent in the world) and 2.82 million tonnes in the Americas (12 per cent), of which 1.81 million tonnes in the United States (64.5 per cent in the Americas and 7.7 per cent in the world), about 3.98 million tonnes in Europe (17 per cent) and 1 per cent in Africa and Oceania.

To sum up, there is a serious mismatch in the global copper industry chain, with mines mainly distributed in Latin America (45%), smelters mainly in Asia (55.9%), and consumption mainly in Asia (70.2%). At present, the main flow of the industrial chain is from Latin America to Asia, smelting and consumption in Asia. China needs to import large amounts of copper ore and electrolytic copper; the US smelting end can basically produce and sell itself (1.33 million tons of ore, 1.15 million tons of smelting and 1.81 million tons of consumption), but hundreds of thousands of shortfalls in consumption need to be imported from the rest of the Americas.

Because the global copper resources will not be excavated in a large number of places in the short term, the mining and consumption areas are quite far away, and the power system of the mining areas is relatively unstable, we believe that the flow of industries from the mining end to the smelting end will not change as a result of the epidemic. Some changes may occur at the consumer end, and a complete industrial chain of finished products from design to production will be closer to the place of consumption, among which China is beneficial to durable goods such as automobiles. Up to now, a small number of accessories are not produced at home but must be imported, and the possibility of building a factory in China will be greatly improved in the future. What is disadvantageous to China is that domestic exports of products such as household appliances will be affected by anti-dumping on the one hand and traffic disruptions on the other hand, so the probability of this part of production capacity coming out in the future is very high.

Overall, we believe that affected by the buttocks determine the head, as long as the main place of global copper consumption is still in Asia and China, the general flow of the global copper industry chain will not change, there will only be minor repairs.

"Click to attend the 15th China International Copper Industry chain Summit"