SMM12 16: in the past two months, rare earth spot and A-share market performance is soft, until the beginning of this month, the rare earth market has picked up.

According to SMM, at present, the import gate of ionic rare earth mines from Myanmar to China has been closed again. The customs closure for Myanmar, the main reason may be that the Burmese government believes that Chinese enterprises do not have a legal mining license in the Burmese region, stolen mining caused damage to the local environment, and triggered a number of international incidents. The current information is that the Burmese side may indefinitely delay customs clearance until rectification and regulation.

Myanmar's ban on rare earth exports began at the end of 2018. From November 3, 2018, Yunnan Tengchong Customs closed, all resource goods from Myanmar can not be imported into China, the specific reasons for customs closure are unknown, customs clearance time is unknown.

On December 14, 2018, Tengchong Customs cleared Burmese rare earth mines for a period of five months.

On February 14, 2019, the Yunnan Tengchong Municipal Government stopped the export of rare earth-related chemical raw materials to Myanmar, covering the Diantan Port of Tengchong, as well as the Monkey Bridge and the surrounding ports at the national first-class port.

Customs clearance began on May 15, 2019, banning the import and export of all rare earth business-related commodities.

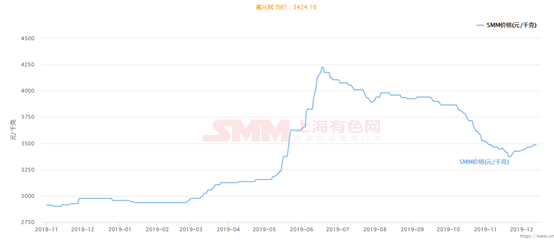

Prior to the import moratorium from Myanmar at the end of 2018, a subsequent five-month implementation period was given and officially closed on May 15, 2019. As a result, the price of medium and heavy rare earths, led by dysprosium oxide and terbium oxide, has risen sharply. Terbium oxide has risen from a low of about 2900 yuan / kg to around 4200 yuan / kg, an increase of as much as 45 per cent. Dysprosium oxide rose from about 1150 yuan / kg to a high of 2000 yuan / kg, an increase of more than 70%. In the middle and late September of 2019, the import gate of ionic rare earth mines was opened again, and the market confidence in the price of heavy rare earths was shaken, and the price of terbium and terbium was put under pressure.

According to the rare earth mining and smelting index released by the Ministry of Industry and Information Technology in 2019, on the whole, the mining index increased by 12000 tons, the smelting separation index increased by 12001 tons, and the increased mining indexes were rock and mineral type rare earth (light). As a dominant resource in China, ionic rare earth (mainly medium weight) index is the same.

Recently, the Sichuan Provincial Economic and Information Department released a message that in accordance with the relevant requirements issued by the Ministry of Industry and Information Technology and the Ministry of Natural Resources, the mining targets for the whole year will be issued to the relevant mining enterprises as soon as possible. China is producing rare earths as planned, and the policy requirements are clear.

SMM believes that the import gate of ionic rare earth mines imported from Myanmar is again closed and the current reopening time is inconclusive, and it is expected that the prices of heavy rare earth products may continue to rise sharply in the follow-up, but towards the end of the year, some businesses in the industry chain have financial pressure, and the market demand has limited support for rising prices. It is expected that the increase in heavy rare earth products in the short and medium term will be limited, and there is the possibility of a sharp rise in the year after the end of the year.

Scan QR code, apply to join SMM metal communication group, please indicate company + name + main business

![[SMM Analysis] Stainless Steel Social Inventory Saw a Slight Buildup, While High Supply Coupled with Cautious Downstream Demand Constrained Destocking](https://imgqn.smm.cn/usercenter/bFzkj20251217171724.jpg)