SINGAPORE, Dec 3 (SMM) – Copper fundamentals continue to look supportive, while the nickel market remains tight, said Ian Roper, general manager of SMM Singapore on the outlook of base metals in 2020.

Roper shared his insights on the base metals outlook in the LME Singapore Gala, noting that it is going to be a good year for demand in 2020, as Beijing has recently brought forward 1 trillion yuan ($142.07 billion) of the 2020 local government special bonds quota to this year as it seeks to boost infrastructure spending.

"Financial conditions are increasingly accommodative, while housing demand has held up better than expected with sales surprisingly recovering as developers move to cut prices," Roper said.

“2020 will be the ‘year of completions’ as developers are pushed to finish developments and price weakness starts to appear,” he added.

A “phase one” trade deal between China and US would be a big boost to confidence as skepticism remains high onshore, Roper said. “If this can lead to a recovery of exports next year this should be a big boost to base metals.”

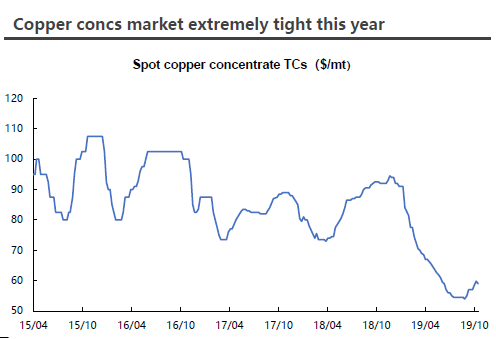

On the base metals outlook, Roper thinks that copper is tight on the raw materials front, while refined inventory is also low through the chain despite weak demand year-to-date.

“When demand picks up, copper tightness should feed through quickly to prices, however in the absence of any recovery in demand from consumer driven sectors, prices will likely continue to be buffeted by macro for the rest of the year,” Roper said.

Expectations for ongoing tightness were behind the sharp drop in annual concentrate contract prices to $62/t for 2020. Spot is likely to remain in a $50-60/t range for the year.

Antofagasta, together with the Chinese and Japanese smelters have agreed on the 2020 copper concentrate treatment charges (TC) in their long-term contracts at $62/mt, and refining charges (RC) at 6.2 cent/lb, the same levels as agreed between Chinese copper smelters and US miner Freeport-McMoRan.

On the inventory end, Chinese refined inventory is at very low levels through the supply chain even after a very weak demand environment. If demand picks up, supply of refined and raw materials will be unable to meet it, and should lead to rapid price gains.

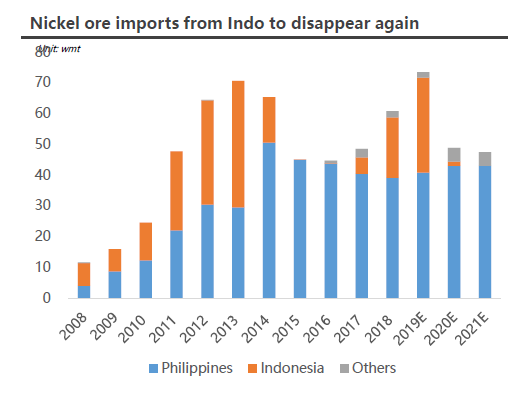

On the outlook of nickel, Roper sees a tighter nickel market in 2020, as nickel prices have surged as Indonesia has bought forward the ban on nickel ore exports from 2022 to 2020. “The nickel market will be tight next year, but the key is how much traditional nickel supply will be incentivised to return by the high prices,” he said.

A decline in Chinese NPI output is likely to happen next year. China NPI output will decline from 550,000 mt this year to around 400,000 mt - 450,000 mt next year, Roper estimated. This will depend on how much Philippine ore can recover in a high price environment. “Indonesian NPI output will lift from 350,000 mt this year to 500,000 mt next year, leaving the nickel market reasonably tight, supporting medium-term prices around $15,000/mt to incentivise more supply."

On other base metals, Roper said that aluminium demand in China has performed well but supply is yet to pick up. However as margins have improved, he expects output to lift into year end given the structural overcapacity situation remains.

Speaking about lithium, Roper noted that supply remains abundant as new processing capacity additions continue. “However the negativity toward the space on the back of EV subsidy changes may be overdone. “