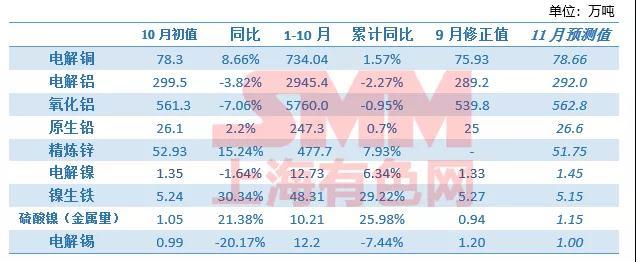

Overview of basic Metal production in China in October 2019

Electrolytic copper

In October 2019, SMM China's electrolytic copper production was 783000 tons, an increase of 3.12% over the previous month, an increase of 8.66% over the same period last year. From January to October, the cumulative output was 7.3404 million tons, up 1.57% from the same period last year. The actual output in October was 778300 tons higher than expected in September, mainly because the output of Jiangxi Copper, Tongling Nonferrous Metals, Yunnan Copper and Jinchuan Group was higher than planned, and to a certain extent, it also reflected the demand of some smelters to catch up with the production plan at the end of the year.

The 200000 tons / year production capacity of Chifengyun Copper Phase II was put into production on October 2, and the first batch of electrolytic copper was produced on October 10. Heilongjiang Zijin Copper Industry gradually climbed production capacity of 150000 tons / year, and the silver non-ferrous copper smelting technology improvement project 200000 tons / year returned to normal operation, all of which provided increments for the output of electrolytic copper in October. And although copper concentrate TC, crude copper processing fees and sulphuric acid prices remain depressed, smelters are close to the spot break-even point, but no smelter has shrunk refining capacity as a result. In addition, the import approval volume of waste copper was reduced by more than 80% in the fourth quarter, and the supply of domestic scrap copper is also tight according to SMM research. Some smelters using recycled copper as raw materials reflect that it is difficult to complete the planned volume in November.

In November, according to the production schedule of smelters, the output of some smelters is still affected by the tight supply of waste copper and anode copper, but the new smelting capacity continues to climb production, and the increase or decrease of the two is basically a hedge. SMM expects domestic electrolytic copper production to rise to 786600 tons in November, an increase of 5.43% over the same period last year, and a cumulative increase of 1.94% to 8.127 million tons.

Alumina

SMM data show that in October (31 days), China's alumina production was 5.863 million tons, including 5.613 million tons of metallurgical grade alumina and 181000 tons of metallurgical grade daily output, a slight increase of 0.63 percent over the previous month. China's total alumina production from January to October 2019 was 57.6 million tons, down 0.95 per cent from the same period last year. The month-on-month increment in October mainly came from Shanxi, where the technological transformation ended. The enterprises that cut production in October (Jiaotou letter, Sanmenxia Hope, Jinzhong Hope, etc.) failed to maintain a strong price, so they maintained the operation level in September, and individual enterprises such as Xiaoyi Huaxing were still restrained because of the lack of domestic ore.

In November (30 days), Sanmenxia hopes to increase its operating capacity. Jingxi Tiangui Phase 1 is expected to contribute some of the increment to the month, and the operating capacity of metallurgical grade alumina will rise to 66.089 million tons by the first ten days of November. SMM expects alumina production to rise to 5.878 million tons in November, including 5.628 million tons for metallurgical grade alumina and 188000 tons for metallurgical grade daily production.

Electrolytic aluminum

China produced 2.995 million tonnes of electrolytic aluminium in October, down 3.82 per cent from a year earlier, and 29.454 million tonnes from January to October 2019, down 2.27 per cent from a year earlier, according to SMM. The reduction in domestic electrolytic aluminum production capacity from August to September continued to have a negative impact on the output and capacity in October. By the end of October, the domestic electrolytic aluminum operating capacity was 35.39 million tons, although the operating capacity increased slightly by 340000 tons over September, but the country's actual contribution to production in that month was still lower than that of nearly 119000 tons in the same period last year. There is no significant increase in new and resumed production capacity in October, and according to the current pace of resumption and commissioning of new production capacity, the scale of new production in November is expected to remain at a relatively low level. SMM expects domestic electrolytic aluminum production to be 2.92 million tons in November (30 days), continuing to maintain negative year-on-year growth, with a growth rate of minus 1.32 per cent.

According to the inventory level from January to October, SMM accumulated 416000 tons of electrolytic aluminum in the first 10 months of this year, and the actual consumption growth rate of cumulative electrolytic aluminum was minus 1.75%. Real estate and cars continue to inhibit raw aluminum consumption. In the process of conversion of raw aluminum consumption structure, the new bright spot of raw aluminum consumption in a single month is not prominent.

Primary lead

In October 2019, the national output of primary lead was 261000 tons, up 4.6% from the previous month and 2.2% from the same period last year, and from January to October 2019, the output of primary lead increased by 0.7% compared with the same period last year.

According to SMM research, in October, most of the primary lead smelting enterprises were in a state of recovery, such as Jiangxi Copper Industry, Xing'an Silver lead, Yunnan Mengzi and other smelting enterprises, and the amount of recovery after maintenance was more than 15000 tons. During the period, heavy pollution weather appeared in the surrounding areas of Beijing, Tianjin and Hebei at the beginning of October and the end of October. Hebei, Henan and other places launched orange early warning, and some smelting enterprises had production limits. at the same time, because the major enterprises have a certain reserve for crude lead, so the impact on the output of refined lead is limited. In October, the month-on-month increment of primary lead production in China was more than 10,000 tons.

Looking ahead to November, primary lead production is expected to continue an upward trend. The main reason lies in Henan Jinli, Xingan silver lead and Haicheng integrity and other enterprises after maintenance recovery. At the same time, imported ores hit the domestic market, and lead concentrate processing fees continued to rise (Pb60 imported TC in November to US $90-120 / dry ton; SMM lead concentrate Pb 50 processing fee area price generally traded to 2000 yuan / metal ton, part to 2200 yuan / metal ton), and appeared in the traditional winter storage period, for the primary lead smelter to provide a better profit basis, to promote enterprises in the lead price down in the market, still maintain a good production enthusiasm, refined lead production further released. In addition, Hunan Jingui, Henan Xinling, Yunnan Chihong has equipment inspection. As a result, SMM expects native lead production to rise slightly in November.

Refined zinc

In October 2019, the output of SMM refined zinc in China was 529300 tons, an increase of 2.64% over the previous month and 15.24% over the same period last year. SMM research sample capacity of 6.085 million tons. From January to October, the cumulative output was 4.777 million tons, an increase of 7.93 percent over the same period last year.

Since April 2019, domestic smelters have broken through the bottleneck of production capacity, and the output trend has shown a unilateral upward trend of 45 degrees. According to SMM research, domestic refined zinc production continued to climb in October, breaking through the all-time high again. From the investigation of enterprises, it is not difficult to find that, driven by high profits, smelting enterprises generally have a high utilization rate of production capacity, and some refineries increase the amount of materials and delay the maintenance time in order to obtain more profits. From the point of view of sub-enterprises, in October, after the resumption of production in the south of Hechi and Zhongjin Lingnan in Guangxi, the output returned to the conventional level. At the same time, the Zhongjinling Nandan Xiaxia Refinery and the Shaanxi zinc industry broke through the capacity bottleneck. To sum up, the domestic refined zinc output continued to rise in October.

In November, domestic zinc ingot production is expected to fall back to 517500 tons, down 2.21 per cent from a month earlier and up 13.40 per cent from a year earlier. Cumulative production from January to November is expected to reach 5.294 million tons, an increase of 8.44 percent over the same period last year. The main reasons are: Henan Yuguang, Wenshan zinc indium and other refineries began maintenance in November.

Electrolytic nickel

In October 2019, the natural monthly output of electrolytic nickel in China was 13500 tons, down 1.64 percent from the same period last year. In October, the national output of electrolytic nickel increased by 1.5% over September. According to the preliminary survey of SMM, the output of a smelter in Gansu increased slightly in October, Jilin smelter continued to stop production in October, or restart production as soon as January next year, and the production situation of other electrolytic nickel smelters remained stable in September. Production of electrolytic nickel is expected to rise to 14500 tons in November, mainly from Gansu, where discharge output is increasing to make up for the impact of previous overhauls, while production at other smelters is expected to hold steady.

Nickel pig iron

National production of nickel pig iron fell 0.64 per cent to 52400 nickel tons in October from a month earlier, up 30.34 per cent from a year earlier, slightly lower than in September. All the enterprises that can be started under high profits are running normally, but the overhaul of a high nickel pig iron enterprise in Jiangsu has not been restored, and the power restriction in Inner Mongolia still has a small impact on the output of some manufacturers. In terms of grade, the output of high nickel pig iron decreased by 0.64% to 45800 nickel tons. In October, low nickel pig iron production decreased by 0.65 per cent to 6600 nickel tons compared with the previous month. The market of 200 series stainless steel is not good. Low nickel pig iron enterprises continue to overhaul in October or have just resumed production at full capacity, and are expected to resume in November.

National production of nickel pig iron is expected to decrease by 1.81 per cent to 51500 nickel tons in November from a month earlier, up 23.35 per cent from a year earlier, of which high nickel pig iron production decreased by 3.19 per cent to 44400 nickel tons. The low nickel pig iron ring increased by 7.8% to 7100 nickel tons, mainly due to the resumption of production by maintenance manufacturers.

Nickel sulfate

In October, China's nickel sulfate output was 10454 tons of metal, and the physical amount was 47500 tons, an increase of 11.18 percent over the previous month and 21.38 percent over the same period last year. The increase in nickel sulfate production this month was mainly due to an increase in the production of nickel sulfate from nickel beans. The premium of battery grade nickel sulfate to nickel bean was expanded to more than 10000 yuan / ton, which stimulated the precursor factory to buy domestic nickel bean spot to produce liquid nickel sulfate. The increase in the use of nickel beans combined with the decline in demand in the new energy industry, the demand for circulating nickel sulfate in the market is poor, and some nickel sulfate plants have further reduced production. National nickel sulfate production may continue to pick up in November, with an increase of 9.57 per cent to 50100 tons in kind over the previous month, equivalent to 11454 tons of metal, mainly due to the release of new production capacity and the resumption of some electroplating grade nickel sulfate production.

Refined tin

Refined tin production in October was 9972 tons, down 17 per cent from September. The domestic refined tin production decreased sharply in October, mainly due to the equipment overhaul of Yunnan Tin Industry Co., Ltd. and individual smelters in Guangxi, resulting in a sharp decline in refined tin production in October. In addition, some smelters in Jiangxi are still in a state of shutdown. In addition, due to the shortage of raw materials, the output of smelters throughout the country has been reduced to varying degrees. In November, Yunnan tin smelters will continue to overhaul their equipment for less than a month, smelters in Guangxi will resume production, and raw material shortages in Jiangxi, Yunnan and other regions will persist. It is initially expected that refined tin production in November will be stable compared with October, about 10000 tons.

Output of metal products in October 2019

Description:

1. The value with * is the corrected value, and the value in italics is the predicted value.

2. The output of nickel pig iron refers to the data after the physical amount of metal is converted into metal.

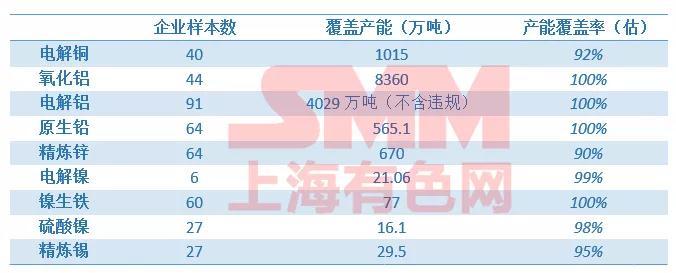

Research methodology:

1) Research methods

SMM production research is conducted by professional analysts by telephone, field research and other means, regularly carry out monthly tracking of Chinese metal production enterprises, and issue a report on Chinese metal production.

In the process of research, ensure the basic coverage proportion of the sample, and continue to expand; at the same time, consider the size of production capacity, geographical distribution, enterprise nature and other details of the reasonable selection and distribution of samples, so that each sub-item data is representative.

Production data include last month's output (initial value), the previous month's output (revised value) and the forecast for the current month's output. In general, SMM rarely modifies the output, that is, the correction value = the initial value, but still retains the possibility of correction.

Before the 10th of each month through the SMM official website (www.smm.cn), WeChat subscription account (Today Nonferrous), mobile phone station (m.smm.cn) and other official channels to the public.

2) sample introduction

"Click to sign up for a thousand people event in China's non-ferrous metals industry.

Scan QR code, apply to join SMM metal communication group, please indicate company + name + main business