LONDON, Oct 30 (SMM) – Copper fundamentals look very supportive as supply remained tight on the raw materials front and refined inventory also stood at lows through the chain, despite weak demand year to date, said Ian Roper, general manager of SMM Singapore.

“If demand picks up, copper tightness should feed through quickly to prices,” Roper shared his insights at the SMM London Metals Seminar on Tuesday October 29. “However in the absence of any recovery in demand from consumer-driven sectors, prices will likely continue to be buffeted by macro for the rest of the year.”

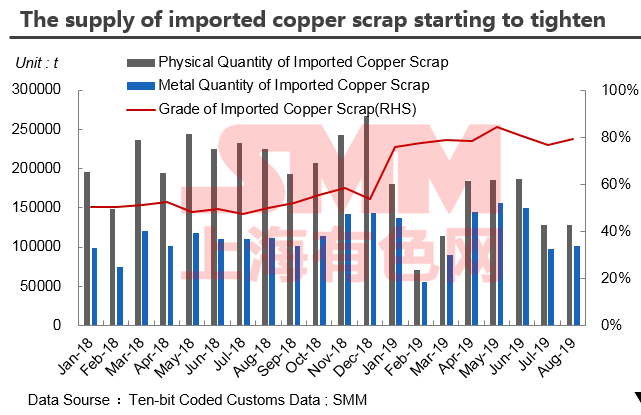

On scrap, some proportion of high-quality copper scrap is very likely to be reclassified as a resource before the import of copper scrap was banned by end 2020, Roper said. But the key question is at what cutoff grade this will be, and clarity on this is unlikely to be seen in 2019, he added.

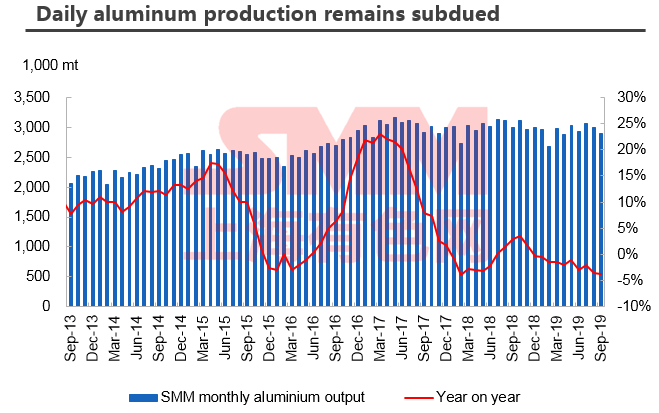

For the prospect of other base metals, Roper expected the ramp-up of new and idled capacity in the fourth quarter on positive margins to limit the upside potential of aluminium prices, even if the macro demand situation improved.

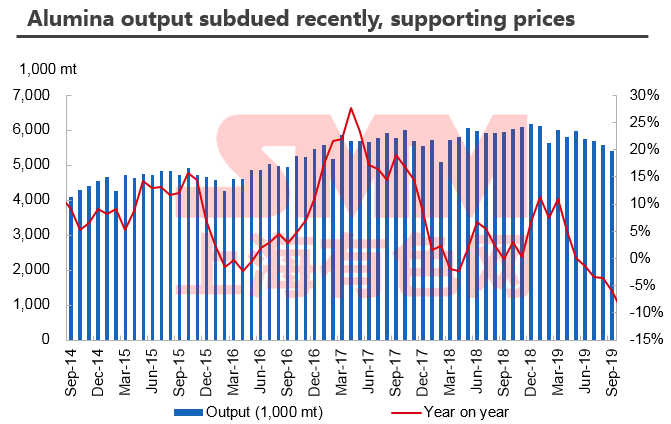

With domestic refinery closures, alumina prices have found a floor around 2,600 yuan/mt ($280-320/mt import equivalent). “As we have long expected, this should put an end to the cost compression story globally,” Roper said.

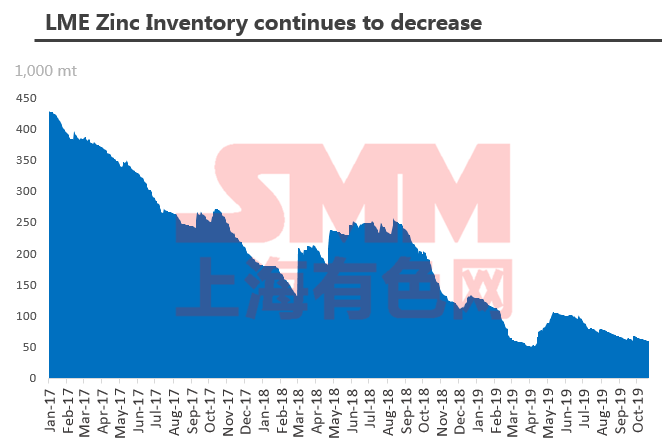

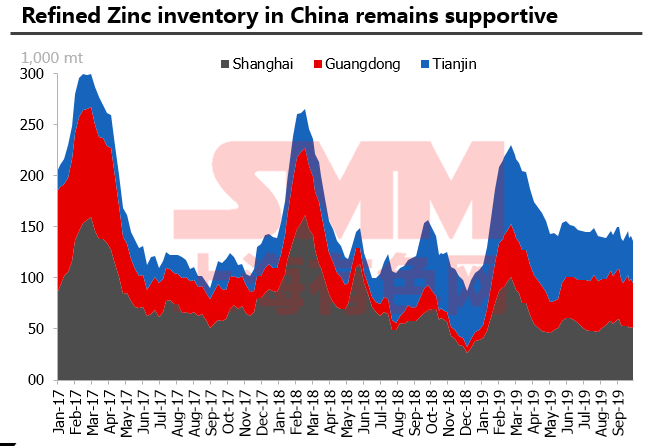

Speaking about zinc, Roper said, "Prices have fallen back to the levels we forecasted at the start of the year as the Chinese smelters finally raised output since May.”

Roper saw zinc prices likely overshooting to the downside if refined inventory starts to lift, but “equally any auto stimulus would likely be more positively reflected in zinc prices given the metals reliance on that sector.”

On the looming ore supply disruption from Indonesia, Chinese NPI output will drop from 550,000 mt this year, to around 400,000 mt, Roper estimated, adding that the swing factor will be how much Philippine ore can recover in a high price environment.

“Indonesian NPI output should lift to as high as 500,000 mt next year from 300,000 mt this year, leaving the nickel market reasonably tight, supporting medium-term prices around $15,000/mt to incentivise more supply.”

![This Week, Platinum and Palladium Experienced Significant Pullbacks, End-Use Demand Recovered, and Spot Market Trading Was Normal [SMM Platinum and Palladium Weekly Review]](https://imgqn.smm.cn/usercenter/obeMy20251217171735.jpg)

![Silver Prices Continue to Pull Back, Suppliers Remain Reluctant to Sell, Spot Market Premiums Hard to Decline [SMM Daily Review]](https://imgqn.smm.cn/usercenter/LVqfJ20251217171736.jpg)