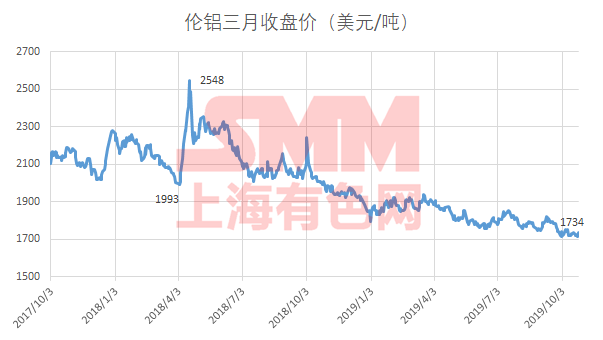

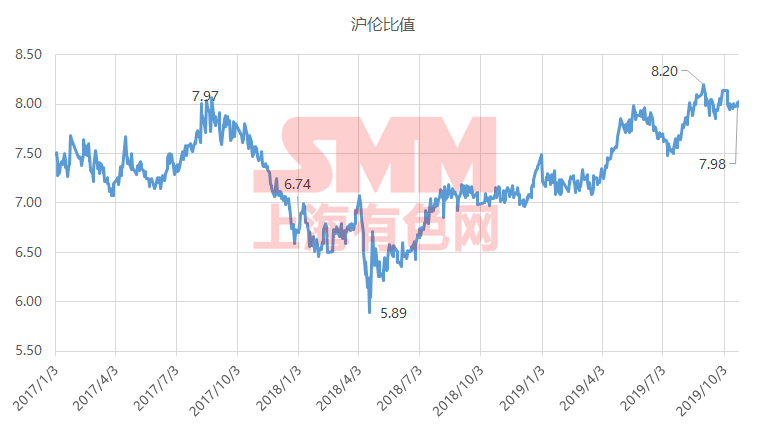

SMM, Oct. 28: from the closing price of Lun aluminum in March, from May 2018, Lun aluminum from April, May to 2548 U.S. dollars / ton has been in the shock decline channel, the corresponding Shanghai-London ratio also rose from 2018 range of 5: 6 to the current 8 or so. Many market participants in investment and industry are looking for the direction of internal and external ratios. At present, the market is more consistent that the Shanghai-London ratio has reached an absolute high level, internal and external positive or there are opportunities, then this paper starts from the financial statements, looking for the cost change trend of overseas electrolytic aluminum plants.

Lunalco has been looking for the bottom after the rally brought about by sanctions against Rusal in April 2018

Source: SMM

The ratio of Shanghai to Lun reached a new high

Source: SMM

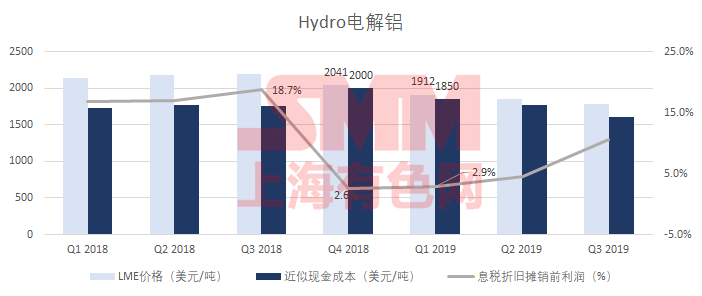

Hydro: the price of electrolytic aluminum went down, but the profit margin was repaired in 2019

Source: company announcement SMM (note that the approximate cash cost used in this data is the company's cost of deducting EBIDTA according to the LME price, which is understood as excluding depreciation, amortization, financing costs and tax production costs)

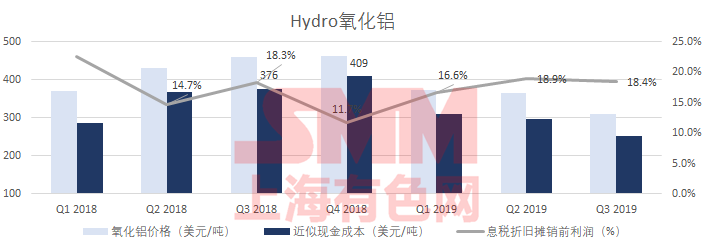

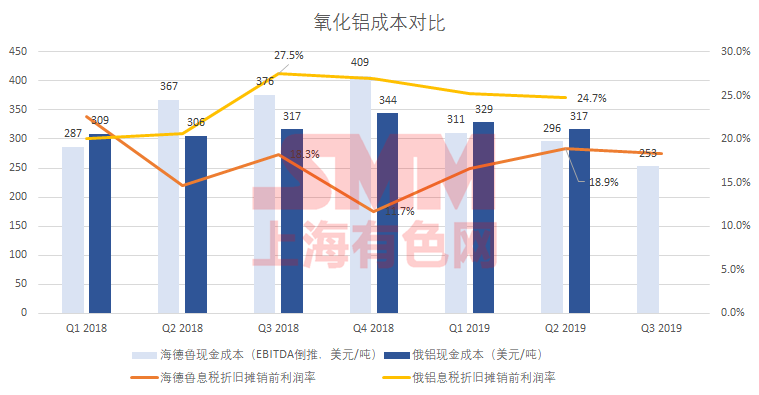

Hydro: alumina costs have fallen to nearly two-year lows, but profit margins are high

Source: company announcement SMM (note that the approximate cash cost used in this data is the cost of deducting EBIDTA from the price of alumina actually sold, understood as excluding depreciation, amortization, financing costs and tax production costs)

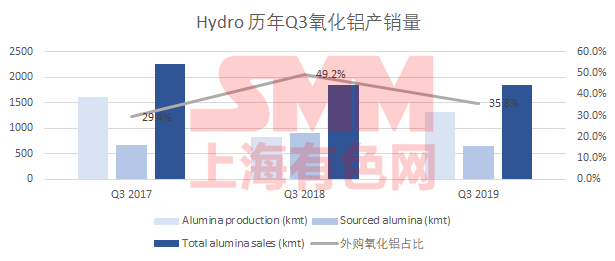

Hydro's alumina outsourcing ratio returned to normal in 2019

Source: company announcement SMM

The operating rate of the Hydro Alunorte alumina plant has fallen to 50 per cent since March 2018, and the supply of alumina to Rusal has also been restricted since March. Alumina prices rose steadily throughout 2018, with Hydro outsourced alumina accounting for 53.5 per cent of Q2 in 2018 from 29 per cent in 2017. At present, as of 2019 Q3, Hydro's proportion of purchased alumina has returned to 35%, slightly higher than the 29% of 2017 Q3, and its alumina production recovered to 1.32 million tons in 2019, accounting for 82% of 2017 Q3 production, which is basically in line with the official target of about 80%.

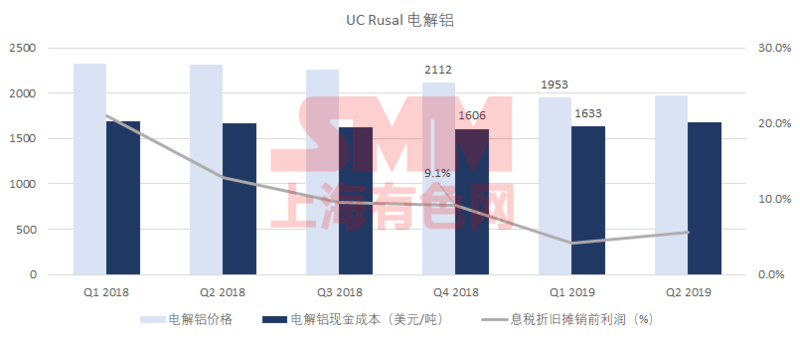

Source: company announcement SMM (note that the electrolytic aluminum used in this icon is the official cash cost of Rusal and the price is the actual sales price of electrolytic aluminum)

Rusal's profit margin was relatively stable in 2018, bottomed out in 2019 Q1 and operated at a low level until half a year in 2019. Its cash costs changed little, and profits were mainly compressed because of the downward price of electrolytic aluminum.

Source: company announcement SMM

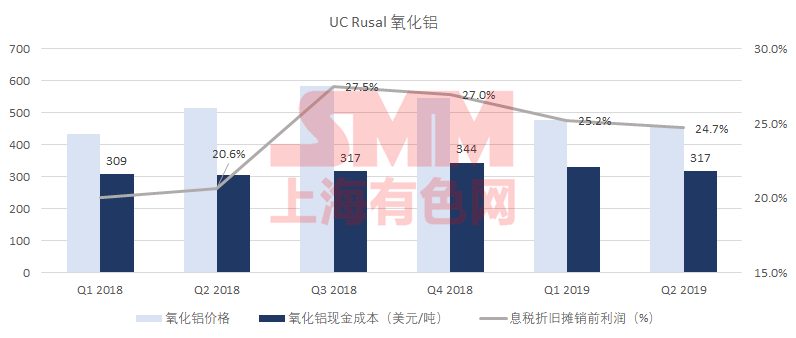

The cost of alumina in Russia is also relatively stable, and profits have increased significantly after the prices of Q3 and Q4 markets rose in 2018.

Source: company announcement SMM

Source: company announcement SMM

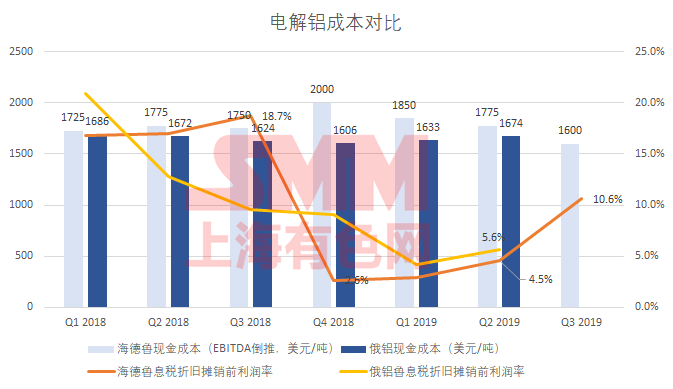

A horizontal comparison of the cost changes of electrolytic aluminum and alumina between Russian aluminum and Haide Road shows that in 2018, the price of Q4 alumina reached the peak, and the profits of alumina and electrolytic aluminum increased month-on-month, while Hydro's alumina and electrolytic aluminum profits dropped off the cliff. From this, it can be found that the increase in alumina prices in 2018 is more driven by supply contraction than by cost. Have a stable self-contained alumina to become a profit safety pad.

In addition, Hydro's cash cost is expected to fall to the same level as Rusal by 2019. Q1 itself has an advantage over Rusal in 2018. With the release of Q3 self-produced alumina, the cost advantage recovers, and the profit of electrolytic aluminum is also repaired. Judging from the cost and profit changes in Hydro, the impact of alumina shortages and rising prices caused by the supply contraction in 2018 has been largely erased.

Back to the price of aluminum, as of the third quarter of 2019, the alumina costs of Hydro and Rusal were falling in 2019, and the cost decline of Hydro was more obvious, mainly by replacing the purchased alumina with self-contained alumina. The decline in the cost of Rusal may be more due to the decline in the cost of raw materials, and the decline in the cost of Rusal is of more reference value. Judging from the historical cost of Rusal, the cost of alumina is very close to the bottom.

Hydro's electrolytic aluminum profits went the opposite way with LME aluminum prices in 2019. Hydro's electrolytic aluminum and alumina profits have been repaired as prices fall, but it can be found that alumina profits have run into bottlenecks. Currently, the Australian alumina FOB price is $280, just $30 from the cash cost, compared with the current disk price of $1733 and the cash cost of $130 from Hydro.

Summary: the price of alumina is already very close to the cash cost, only $30 from the cash loss, so there is some support on the cost of overseas electrolytic aluminum; Electrolytic aluminum profits are actually better than 2019 Q1, Q2, this round of aluminum exploration space is more by the price of alumina, if the consumer end and trade environment continue to be unable to improve, overseas electrolytic aluminum profits may be further squeezed, but only about $130 from the cash cost.

(SMM SMM Liang Xuan 021-5166 6922)