According to customs data released in late July and June, China imported about 16.0716 million tons of manganese ore (legal quantity) by the first half of 2019, with an import value of about US $3.226994 billion. (for the convenience of reading the data, some of the following text and column charts are mainly in kilotons and tens of thousands of US dollars)

General Review on the demand for imported Manganese ores:

The price of Si-mn alloy fluctuated greatly in the first half of the year. This year's demand-side logic mainly depends on the following volume points:

The profits of downstream steel mills and alloy mills directly establish the price trend of manganese ore. In addition to relying on occasional and short-term story speculation, the supply and demand structure of manganese ore has become the lifeline of manganese ore price and traders' profits. In the unfathomable manganese ore market in 2019, a series of data such as the quantity of imported manganese ore, the proportion of mineral market, the trend of supply and demand and so on are the contents of the market. The SMM data are collated and analyzed, shared and discussed with people in the industry.

General Review on the supply of imported Manganese ores:

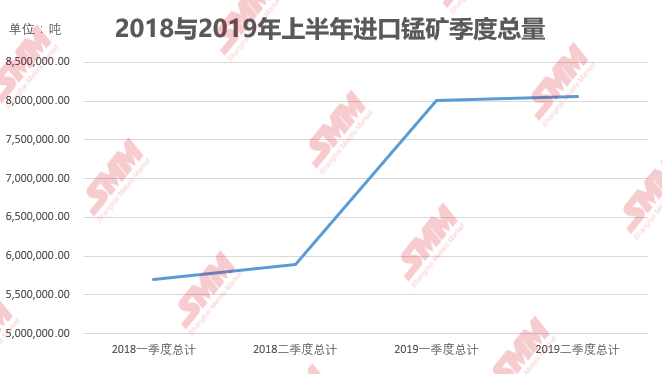

From January to June 2019, China imported about 16071.6 kilotons of manganese ore (legal quantity), with an import value of about US $3.226994 billion.

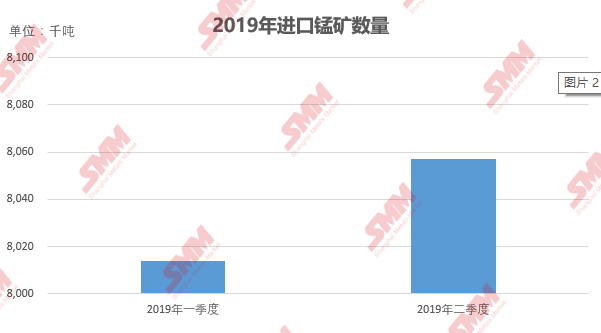

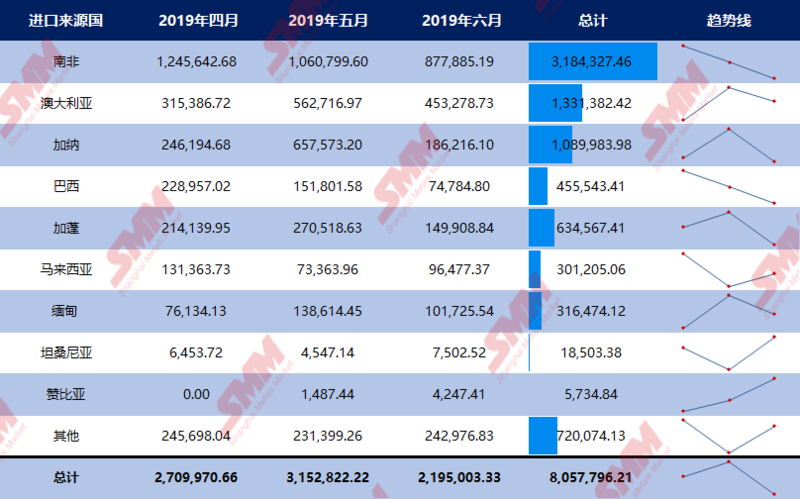

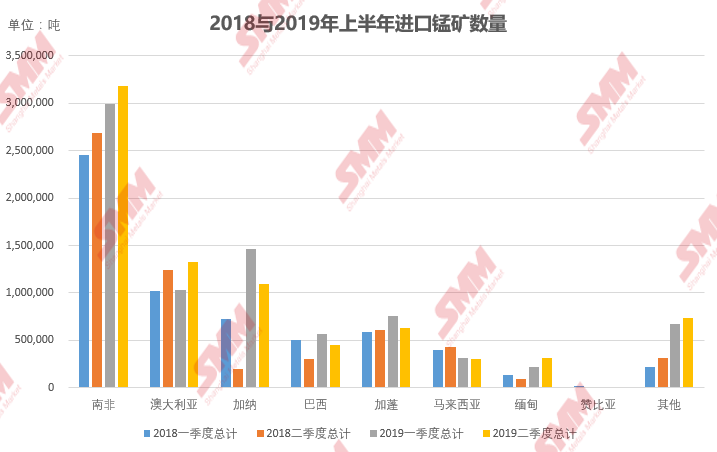

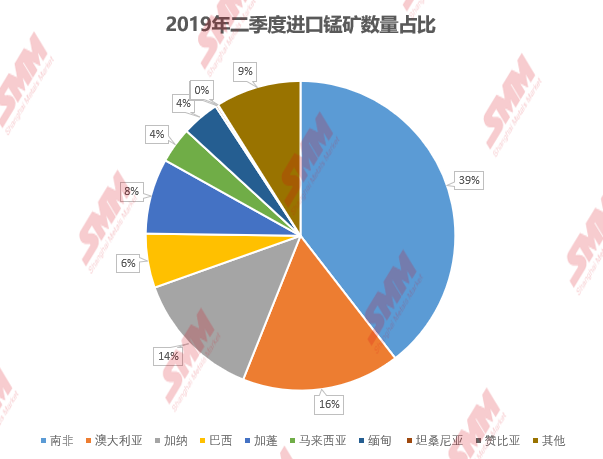

In the second quarter of 2019, both the import quantity and the import amount increased compared with the first quarter, and the quantity of manganese ore imported in the first quarter of 2019 was about 8014 thousand tons. The amount of manganese ore imported in the second quarter was about 8057 kilotons, an increase of 0.54 percent over the quarter-on-quarter comparison, of which the Australian mine increased by 29.47 percent, the South African mine increased by 6.48 percent, the Gabon mine decreased by 15.68 percent, the Brazilian mine decreased by 19.31 percent, and the Ghanaian mine decreased by 25.64 percent.

Total imports in June were 2.195 million tons, down 30.38 percent from May, an increase of 11.15 percent over the same period last year, including 20.77 per cent in Australia, 17.24 per cent in South Africa, 33.2 per cent in Gabon, 36.3 per cent in Brazil and 71.68 per cent in Ghana.

Unit: ton

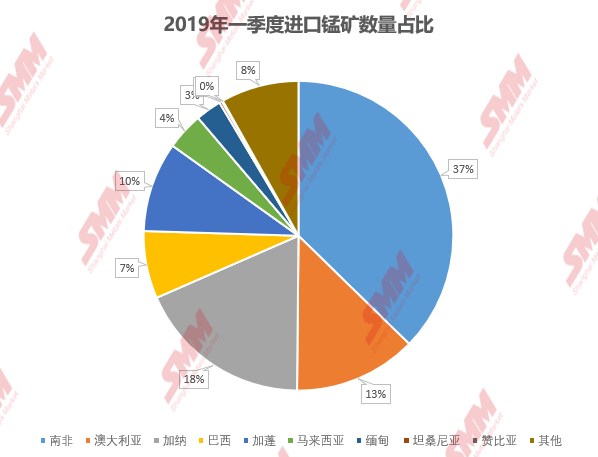

The total amount of manganese ore imported from January to June 2019 was 38.68% higher than that of 2018, and the total amount of manganese ore imported in the first quarter of 2019 increased by 40.61% compared with the same period last year, including 22.12% in South Africa, 0.68% in Australia, 101.54% in Ghana, 11.37% in Brazil, 27.46% in Gabon and 22.92% in Malaysia. In the second quarter of 2019, the total amount of manganese ore imported increased by 0.55% compared with the same period last year, including 6.48% in South Africa, 29.47% in Australia, 25.64% in Ghana, 19.31% in Brazil, 15.68% in Gabon and 3.39% in Malaysia.

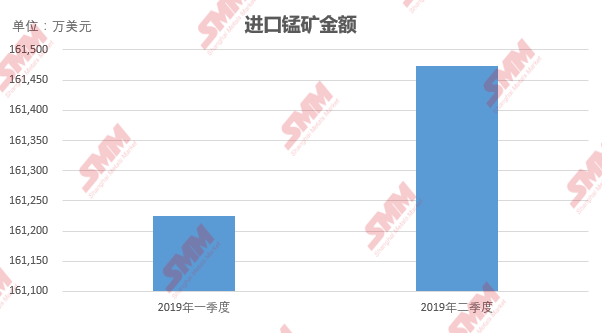

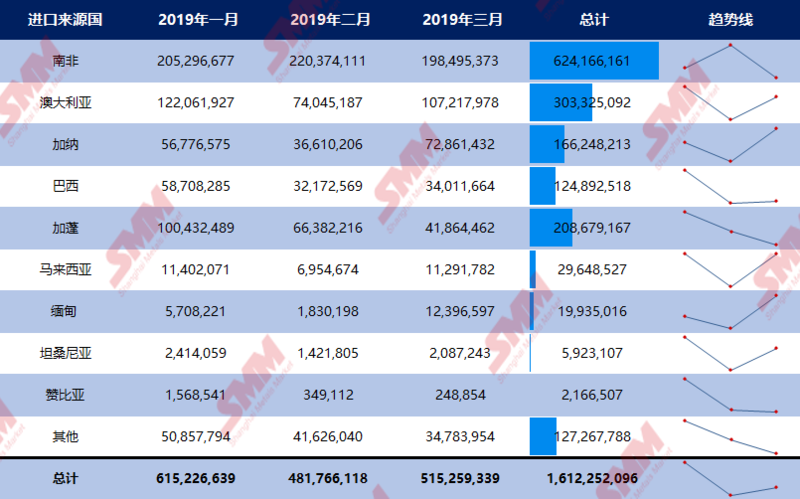

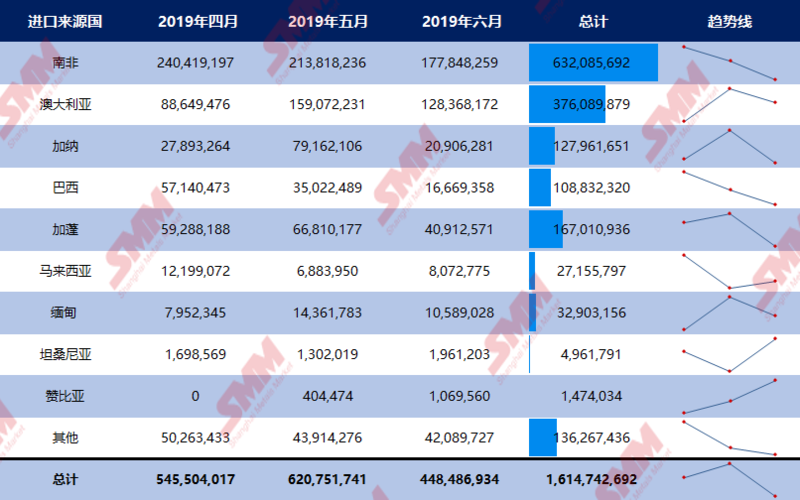

Manganese imports were about $162.25 million in the first quarter of 2019 and about $1.61474 billion in the second quarter.

Market trend of imported manganese ore:

Stimulated by the high expectation of the terminal market in the first quarter of this year, the market from downstream steel mills to middle-end manganese alloy plants to imported manganese ore has been more or less favorable, and the actual market performance has even exceeded expectations. In the case of the relative prosperity of the whole industrial chain, China's imported manganese ore market in 2019 presents the following characteristics:

High demand-as the downstream alloy industry is gradually picking up after the "de-capacity" period since 2014, the level of demand is high, coupled with the exuberance of downstream demand this year, China's manganese imports have maintained a high level;

High attention-under the high demand, China's strong demand for imported manganese mines and weak bargaining power have attracted the attention of other mainstream mines overseas, and sustained imports may lead to a small oversupply. However, due to the strong bargaining power of overseas mines, the high pursuit of profits has also made the quotation to China has been at a high level. Domestic traders are also constantly improving import results and adjusting trade strategies and even pricing methods in order to gain domestic market share.

June 2019 domestic Silicon and Manganese Import companies ranked top30

Baosteel Resource holding (Shanghai) Co., Ltd.

Xiamen international trade group co., Ltd.

Beijing Dexin Yida Trading Co., Ltd.

Shanxi Yuanfeng Zhitong Industrial Co., Ltd.

Chengda products (Xiamen) Co., Ltd.

Xiamen Xiangyu Logistics Group Co., Ltd.

Wo Jian international engineering co., Ltd.

Ningxia Tianyuan Manganese Group Co., Ltd.

Xishuangbanna Ruihang Trading Co., Ltd.

Zhejiang Shang Zhongtuo Group Co., Ltd.

Jianfa Logistics Group Co., Ltd.

China Mineral Resources Co., Ltd.

Sumida international technology trading co., Ltd.

Dushan Jinmeng Manganese Industry Co., Ltd.

Chongqing Bosai Mining (Group) Co., Ltd.

Glencore co., Ltd.

Jianfa Logistics (Tianjin) Co., Ltd.

Hangzhou Steel Foreign Economic and Trade Co., Ltd.

Shuai Special International Trade (Shanghai) Co., Ltd.

Henan Xibao Metallurgical material Group Co., Ltd.

Wenling Hengpeng International Trading Co., Ltd.

Guizhou material Group International Trade Co., Ltd.

China Nonferrous Metals Import and Export Jiangxi Co., Ltd.

Guangxi Beigang Resources Development Co., Ltd.

Guangxi Hengxiang Industry and Trade Co., Ltd.

China Geology and Mining Co., Ltd.

Baosteel Resource holding (Shanghai) Co., Ltd.

Guangxi large Manganese Industry Group Co., Ltd.

Xiamen Haiyi International Trading Co., Ltd.

Top30 ranking of domestic Silicon and Manganese Import companies in 2018

Beijing Dexin Yida Trading Co., Ltd.

Xiamen Xiangyu Logistics Group Co., Ltd.

Baosteel Resource holding (Shanghai) Co., Ltd.

Beijing Jingyuan Xialong Trading Co., Ltd.

Jianfa Logistics (Shanghai) Co., Ltd.

Jianfa Logistics Group Co., Ltd.

Ningxia Tianyuan Manganese Group Co., Ltd.

Chongqing Bosai Mining (Group) Co., Ltd.

Hangzhou Steel Foreign Economic and Trade Co., Ltd.

China Mineral Resources Co., Ltd.

Qingdao Wanfeng Shuangcheng International Trading Co., Ltd.

Shuai Special International Trade (Shanghai) Co., Ltd.

Ningxia Shengyan Industrial Group Energy Circular economy Co., Ltd.

Sumida international technology trading co., Ltd.

Shanxi Oriental Resources Development Co., Ltd.

China Aviation International Mineral Resources Co., Ltd.

Glencore co., Ltd.

Wo Jian international engineering co., Ltd.

Guangxi Hengxiang Industry and Trade Co., Ltd.

Tianjin Haorui Mineral Resources Co., Ltd.

Guangxi Jinmeng Manganese Industry Co., Ltd.

Guangxi large Manganese Industry Group Co., Ltd.

Henan Xibao Metallurgical material Group Co., Ltd.

Guizhou material Group International Trade Co., Ltd.

Jiaocheng Yiwang Ferroalloy Co., Ltd.

Tangshan Caofeidian Zhonggang Industrial Co., Ltd.

Ningxia Huaxia Logistics Co., Ltd.

Jianfa Logistics (Tianjin) Industrial Co., Ltd.

Citic Jinzhou metal co., Ltd.

Xiamen Shengmao Co., Ltd.

As the high temperature of China's manganese mine market has not decreased this year, and the number of ore varieties and grades has been increasing, SMM will recently expand and subdivide the manganese ore price points of the website, and welcome opinions and suggestions from relevant industries. Our company will open the way, Channaya, absorb the opinions of all parties, constantly improve the quotation mechanism, and provide more accurate price reference for the market. (contact person and contact information attached at the end of the article)

There are risks-based on the overall stable production capacity of southern silicon and manganese manufacturers, after the first quarter of 2019, re-producing silicon and manganese manufacturers have returned to the market one after another, rich manganese slag manufacturers also because of 2019 industrial guidance catalogue or will transform small furnace into large furnace, so the demand of southern manganese mine market may maintain a small upward trend in the second half of the year, and the pressure of large surplus supply is relatively small. Due to uncertain factors such as power limitation, maintenance and accidents in the northern silicon and manganese market, as well as the idea of increasing the export of new minerals and increasing production to China in South Africa and the world, Tianjin Port maintains the largest manganese ore import port in China, and the incremental pressure of manganese ore will mainly be borne by Tianjin Port. Therefore, the northern manganese mining market may continue to be plagued by the risk of imbalance between supply and demand throughout the year.

Domestic manganese ore traders have been losing money since late April, the market is wailing, and a small number of second-hand traders have to leave gloomily. Some people can't help wondering: is the manganese mine market sick? In this regard, SMM summed up the following three reasons:

1. China's strong demand for imported manganese mines and weak bargaining power have attracted the attention of other mainstream mines overseas. Sustained imports may lead to a small surplus in supply, but because of the strong bargaining power of overseas mines, the high pursuit of profits makes the quotation to China has been at a high level, and the cost pressure of traders is greater.

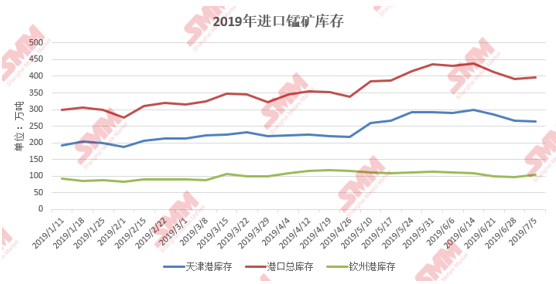

Second, in the past three years, the total inventory of imported manganese mine ports in June this year reached an all-time high, strong inventory led to the imbalance between supply and demand, but also led to the weakening of the bargaining power of traders;

High-pressure competition, under the general situation of the overall economic environment, traders throw goods at a low price from time to time; at the same time, under the continuous attention of the domestic manganese mine market, the import volume of non-mainstream minerals such as Zambia, Senegal, Kenya, Mozambique and so on is slowly increasing, to a certain extent, impact the market supply pattern. Under the "three high" symptoms of high cost, high inventory and high pressure, the broken window effect of the market gradually appears, even if the downstream alloy demand improves obviously in May and June this year, the rising trend of port manganese mine price is still slightly weak, and the comprehensive profit margin is still general ([SMM analysis] from January to June 2019, manganese ore into the "three high" market health to be adjusted https://news.smm.cn/news/100949231);

Replaceable-due to the further expansion of demand, more and more overseas mines will pay attention to China, and the types of domestic manganese ores are also increasing, which makes the choice of downstream alloy plants more diverse. Under the condition that the supply index of manganese ore is in line with alloy production, cost control is the core for alloy factories to choose manganese ore. Therefore, the barriers to the entry of non-mainstream mines into the Chinese market have been weakened to a certain extent, and the division of market share may usher in a watershed.

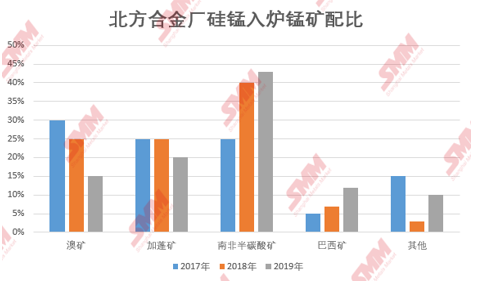

According to SMM research, at present, the proportion of Australian ore charge in the northern alloy market has declined, and the proportion of relatively low-cost ores such as semi-carbonic acid and Brazil has gradually increased. Other minerals include imported non-mainstream minerals and domestic low-grade manganese ores. The decline of "other minerals" from 2017 to 2018 is mainly due to the elimination of domestic manganese ores in the main northern producing areas, while other non-mainstream ores have not yet entered the Chinese market in large quantities.

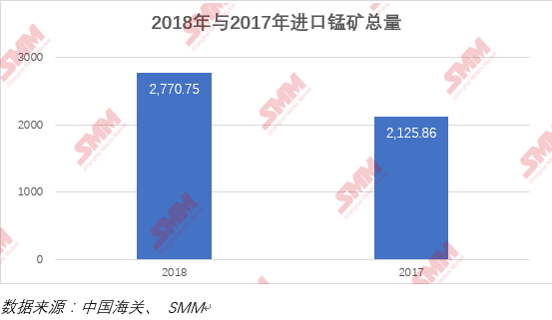

Compared with last year, the total amount of manganese ore imported in 2018 was 27.7075 million tons, compared with 21.2586 million tons in 2017, an increase of 644.89 tons from the previous month, an increase of 30.33 percent, and the average monthly import volume increased by 537400 tons over the same period last year.

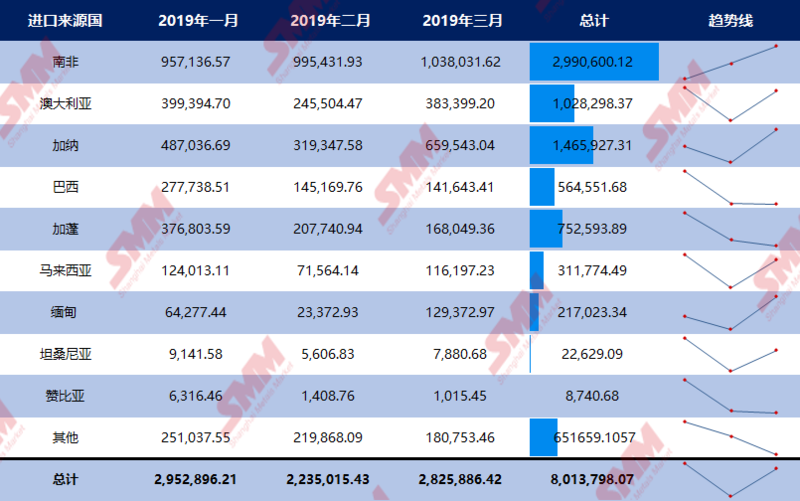

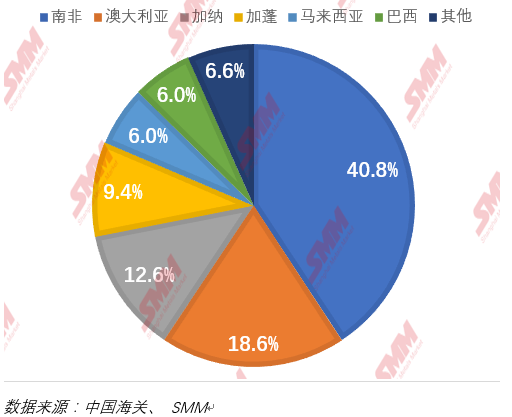

Among them, the six countries that exported the largest amount of manganese ore to China in 2018 were South Africa 11.2622 million tons, Australia 5.1384 million tons, Ghana 3.1498 million tons, Gabon 2.6054 million tons, Brazil 1.6652 million tons, Malaysia 1.652 million tons, accounting for 25.7999 million tons, accounting for 91 percent of the total imports, an increase of 1.8347 million tons over 2017. Among them, South Africa has always maintained a leading position, accounting for 40.8% of the total imports in 2018.

Historical market review: in 2017, the silicon and manganese industry is going through an adjustment stage, environmental protection policies reduce the production capacity of silicon and manganese manufacturers, the silicon and manganese market fluctuated in the first half of 2018, and ushered in a "bull market" in the second half of the year. On the one hand, some of the production capacity of environmental protection inspection and withdrawal caused a partial gap in the spot market. Therefore, from June 2018, manganese ore imports began to increase gradually; At the same time, the new rebar standard, which came into effect in November, has increased the consumption coefficient of silicon-manganese alloy in the iron and steel industry. At this time, steel prices are also very strong, and steel prices accept higher prices for raw materials. Silicon-manganese alloy prices have successfully pulled up and remained at a high level of more than 8000 yuan per ton for many months. Rising prices have stimulated the production of new production capacity that is already on the sidelines, and a number of new production lines were put into production in the second half of the year. It quickly made up for the gap caused by the increase in demand, and the silicon and manganese market entered a state of booming supply and demand, which greatly stimulated the demand for manganese ore imports. Manganese ore imports performed brilliantly in the fourth quarter of 2018, with a total import volume of 8.50603 million tons, accounting for about 31 per cent of the total imports for the whole of 2018.

Monthly market review of imported manganese ores from January to June 2019:

In January 2019, the market price of China's imported manganese ore fell first and then stabilized. Within a month, affected by the favorable factors of the downstream Si-mn alloy manufacturers before the Spring Festival, the port manganese ore transaction atmosphere is OK, but because the port manganese ore inventory is also at a higher level, in order to ship the goods smoothly, importers have to reduce prices and lose money. At the end of the month, as the holiday approached, port trading gradually stalled, although prices are still showing signs of falling, but the main operators have basically no operation.

In February 2019, the market price of China's imported manganese ore was slightly higher. After the Spring Festival holiday, some manganese ore traders began to raise spot quotations tentatively in order to cope with the post-festival replenishment demand of some alloy plants. In the northern region, due to the previous poor market after the festival, some small and medium-sized alloy factories have relatively few supplies before the Spring Festival, so some of the procurement demand after the festival is released, the trading volume is not large, but the transaction center of gravity has slightly increased. Although the southern market also has a high price mentality, but the cost of small and medium-sized alloy plants is higher than the northern alloy plant, the rhythm of resuming production after the festival is also relatively not active, so the rise of the center of gravity is not obvious.

In March 2019, the price of manganese ore was stable as a whole, and the mainstream price did not fluctuate obviously. On the supply side, the overstock of manganese ore is more obvious in the two mainstream ports. Due to the low alloy transaction price at the beginning of the month, the profit of downstream alloy manufacturers is meagre or even upside down. Although there is an inquiry, the overall demand for manganese ore is less. Some manufacturers store manganese ore looking forward to falling mood; For miners, the ore arrived in early March is basically February shipment of goods, the cost is the lowest level in recent months, compared with the spot price, the profit space is more obvious, miners are in no hurry to reduce prices and digest inventory. In the middle of the month, the inventory of manganese ore is still at a high level, but the price has not been loosened. On the one hand, the high price sentiment of the downstream silicon-manganese alloy plant and the drive of the market news have brought a turnaround to the downstream profit, and the manganese ore price has been supported. On the other hand, the reduction of value-added tax will reduce the cost of manganese ore importers and may increase the profit space for the future market. At the end of the month, the overall quotation of overseas mines to China did not rise or fall sharply, while the price of manganese ore was supported, at the same time, affected by the increase of the quotation of downstream alloy mills and the rise of the bidding price of some steel mills, some miners made a tentative small bid, but because the mainstream steel mills have not yet been priced, the higher price of the alloy has not yet been fully established, and the standing price behavior of the miners has not been generally recognized by the market, and the price of manganese ore remains stable.

The value-added tax in China has been reduced to 13% since April 1, 2019, so the price of imported manganese ore has been slightly reduced at the beginning of the month, but it has not affected the profits of miners. At the beginning of the month, due to the beginning of the downstream alloy steel move, the mining demand of the alloy factory increased, and the inventory decreased slightly, but due to the continuous high inventory of manganese ore in the whole port, the downstream alloy manufacturers intended to suppress the mining price, and then the downstream manufacturers gradually launched a game with the miners. In the middle of the month, the alloy quotation was lower than that of last week, the trading atmosphere list, the overall market downstream was weak, and the high price of manganese ore was not accepted and a large number of intentional suppression of ore price existed, which led to the demand side of manganese ore turning to desolation. Manganese ore trading volume is relatively flat, multi-alloy factory to inquire, wait-and-see atmosphere gradually thickens; At the end of the month, manganese ore prices again, some traders zero profit or even upside down shipment, in order to solve the cash flow and high inventory pressure.

At the beginning of May 2019, International Labour Day returned from four days short holiday, the manganese mine market slightly changed the sustained price and transaction double downturn market in the second half of April, the transaction rhythm accelerated, the trading volume increased, but the overall manganese mine market price remained low and consolidated, and some minerals also showed a slight downward trend again. In the middle of the month, the import manganese mine port inventory surge, Tianjin Port inventory increase is the most obvious, manganese ore traders under the pressure of cash flow, pressure shipment, most of the minerals hanging upside down for sale; At the end of the month, the port inventory continued to be high, the price of Tianjin Port Manganese Mine continued to fall, and the price of Qinzhou Port Manganese Mine in the south was relatively stable, but the overall trading volume did not increase significantly, mainly due to the fact that the profit space of the downstream alloy factory was thin and the willingness to produce was poor. The demand for manganese ore in the upper reaches is general.

In early June 2019, due to the influence of the increase of steel recruitment scalars in the downstream alloy market, the terminal demand is expected to improve compared with May, and the inquiry atmosphere of port manganese ore is better, but because many alloy factories hoard more port manganese ore inventory, the short-term spot demand is general. At the same time, the quotation of overseas mines to China began one after another in July, and the downward trend of the quotation is inevitable. The alloy factory is more certain that the price of manganese ore will continue to fall in the future, and at the same time, it will also try to lower the price at the same time. At the same time, the port inquiry atmosphere is better, at the same time, the wait-and-see mentality is also very strong. On the supply side, the inventory situation of the mainstream ports in the south and north is not optimistic. The manganese mine inventory in Tianjin Port is about 3 million tons and that in Qinzhou Port is about 1.05 million tons, which is smaller than that of last month and is still at a high level as a whole. Among them, some storage arrangements were made in early June, with the addition of about 10000 tons of bulk, about 116000 tons of semi-carbonic acid in South Africa, and about 41640 tons in Australia. Under the background that the supply still exceeds demand, the three mainstream Canon imports of manganese oxide ores have been quoted at a low price, with a reduction of 0.5yuan per tonne. The main purpose is to clear the backlog of stocks as soon as possible and at the same time facilitate futures price negotiations with overseas mines. It is to increase the bargaining power to the price of manganese ore in the future; In the middle of the month, the rise in alloy prices failed to lead to a rise in mineral prices, mainly due to the weakening of the bargaining power of mines caused by excessive inventories. 46% of the price of Tianjin Port and Macao Block was 51-52 yuan / tonnage, 1 yuan / tonnage lower than before, and the price of semi-carbonic acid in South Africa was 45.5-46 yuan / tonnage, 0.5 yuan / tonnage lower than before. The price of imported manganese ore from Qinzhou Port in the south fell slightly at the same time in Tianjin Port. At the end of the month, under the background of the continuous improvement of alloy profits, the miners collectively pushed up the price, and the quotation was raised by 2 to 3 yuan per ton, but the actual transaction price only increased by 1 to 1.5 yuan per ton, and the steel price was good at the end of the month. The profit of the alloy factory increased slightly again, and it was imperative for the miners to push up the price again.

Overall, the problem of oversupply of manganese mines is very worrying at this stage. If the prosperity of the industry is good, even if there is a surplus of manganese ore, it will only be reflected in the improvement of profit margins of manganese alloy enterprises. However, if the prosperity of the steel industry declines, the surplus of manganese ore will be more obvious, the price war at the raw material side will briefly push up the profits of the alloy plant, and lead to the surplus at the subsequent alloy end, and the price of manganese and silicon will be closer to lower cost.

Manganese mines are spitting up from last year's high profits, and the excess haze is lingering. The large oversupply of manganese mines is evident in the fact that this year the manganese mines are paying off their debts for last year's unreasonably high prices. Stimulated by the new thread standard for downstream silicon and manganese demand in the fourth quarter of last year, the manganese industry chain ushered in a "rocket" price increase from top to bottom, a large number of capacity recovery, production increased significantly, but after the tuyere passed, although the price has fallen, but the supply remains rigid. The increase in manganese ore imports and stocks this year is very high, both breaking historical records.

In this context, in addition to the increase in the total amount of manganese ore imports and oversupply, another prominent phenomenon is that China's manganese ore imports from various countries have increased significantly. This suggests that last year's rise in manganese prices has prompted manganese mining companies around the world to resume production and has directly contributed to the accumulation of China's manganese imports and port stocks this year. We believe that even in the event of a sharp fall in prices, the current situation of high imports will have little room for improvement in the second half of the year, which will make it difficult for costs to find a solid bottom.

In addition, it is worth mentioning that a few days ago, Tianjin Customs staff carried out a water gauge weight on the "Taibo" wheel loaded with more than 40,000 tons of South African manganese mines, marking the completion of the inspection of bulk manganese mines in Tianjin Port in the first half of the year. In the first half of this year, a total of 14.213 million tons of bulk manganese ore were imported by Tianjin Customs, ranking first in the country, an increase of 87.9 percent over the same period last year, and the import volume reached a new high. According to statistics, since 2011, Tianjin Port bulk manganese ore imports have been in the first place in China, accounting for about 85% of the total imports. The main source countries are South Africa, Australia, Brazil, Gabon, Malaysia and so on. In the past two years, the quantity of manganese ore from South Africa is relatively high in Tianjin Port. In the first half of the year, the import volume of bulk manganese ore in South Africa reached 4.807 million tons, accounting for 33.8%. In addition, Ivorian manganese mines have sprung up this year, with imports increasing by 272.7 per cent. With the continuous increase of manganese ore import in Tianjin Port, the phenomenon of short weight also occurs from time to time. 504th batches of short weight occurred in the first half of the year, involving about US $16.132 million. Tianjin Customs reminds the domestic consignee that when signing a trade contract, it should pay attention to reserving the right of final inspection and claim for the arrival of the goods, making a claim in a timely manner, and feedback the claim to the local customs. At the same time, pay attention to the choice of the shipping company to ensure that the goods are loaded on the cargo ship which is in good condition, the ship constant is accurate and stable. (Tianjin Customs ranks first in China in bulk manganese ore imports in the first half of the year https://news.smm.cn/news/100953432)

Contact: Liu Yuqiao 021 51666804

Yu Wen 021 51666840