SMM, July 19 / PRNewswire-Asianet /-

Zinc prices rose at the bottom this week, temporarily away from the low level of ten thousand nine points of view, based on macro, fundamental analysis, the period of zinc back up power is insufficient, or difficult to further rise.

First set the macro tone: because inflation is still far from the 2% target, in July the Federal Reserve is expected to join the easing camp to start cutting interest rates (a 25 basis point cut is expected to be close to 100%), which is good for non-ferrous metals, and the market has laid out the expectations of interest rate cuts ahead of time. The macro view is good.

Let's look at the fundamentals:

1) supply side. Smelter production has swung within a narrow range around the peak of the year, as some refineries have not yet been overhauled this year in the third quarter, and the smelter output adjustment is expected to continue, but the zinc ingot supply will shift to loose in the long run. The adjustment of the expected difference in zinc supply does not constitute a back-up power, but only affects the fluency of the decline.

2) consumption side. July is in the off-season of absolute supply during the year, the starting rate of the three primary consumer sectors of zinc is expected to record the same month-on-month decline, deduced from the terminal upward: real estate, cars, consumer goods are no bright spot, and infrastructure power due to the differentiation of capital problems, short-term has not seen a trend change, zinc consumption at the bottom is stable, short-term prices have no driving force.

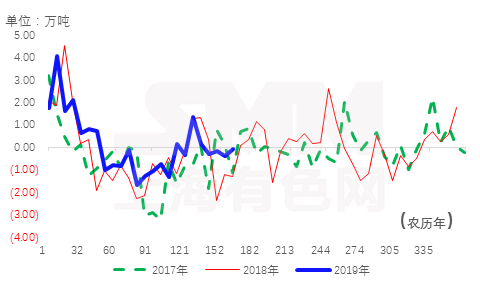

3) inventory. From the point of view of comprehensive supply and demand, there is no accident that the zinc social inventory increased in July, but the zinc social inventory has declined for four consecutive weeks since the beginning of July, the deviation is more obvious, mainly contributed by the decline of Shanghai and Tianjin. According to SMM, this change is closely related to the production status of mainstream circulation brand refineries in Shanghai and Tianjin.

The main circulation brands in Shanghai are: Qin Zinc / Yuguang / Shuangyan / Chihong / Red Heron-V / Copper Crown. Among them, copper crown and Qin zinc were overhauled at the end of June and early July, and Yuguang began to be overhauled in early July. Although the impact of output is limited by month, due to the influence of daily and weekly distribution and the angle of transportation, due to the low inventory volume of finished products in the refinery itself, it is normal for short-term maintenance refineries to tighten the supply of mobile goods to the market. At the same time, Red Heron-V (Chengzhou Mining and Metallurgical) is also mainly in circulation in East China, but it is difficult to recover in the short term after stagnation at the end of May. On the other hand, import replenishment also has a greater impact on the liquidity of the Shanghai stock market. Since the end of June, the decline in inventory in the bonded area has slowed down synchronously; generally speaking, the decline in inventory is mainly caused by the reduction in short-term supply. According to SMM, Qin zinc / copper crown has been overhauled last week, Yuguang will also be overhauled in the near future, from the point of view of production to transport, the actual arrival of goods into the market next week is expected to increase (mainly contributed by domestic brands).

The main circulation brands in Tianjin are Zijin / Hongye / lark / Silver / West Mine / Hulunbeir Chihong. From July to August, refineries in Inner Mongolia, which have not yet been overhauled during the year, will begin to be overhauled one after another, similar to the Shanghai stock market. Due to the impact of maintenance and transportation of goods, the market liquidity will fall into a temporary tension and will not be sustained.

The Cantonese style in the second half of the year does not exist this problem, inventory recorded a continuous increase.

Generally speaking, there is no continuity in the recording and reduction of zinc social inventory, which only leads to the delay of accumulation, which is similar to the impact on the supply side, and does not constitute a driving force for return, but affects the degree of fluency of the decline, that is, the lack of confidence in short and short positions temporarily stops the surplus and leaves the field to wait and see. It is shown that the return of zinc positions coincides with the upward movement of zinc positions in the current cycle, and the strength of filling gaps near the 40-day moving average has increased. It is expected that the zinc price will jump to a greater pressure on the 40-day moving average. The upward path is unsustainable in the short term.