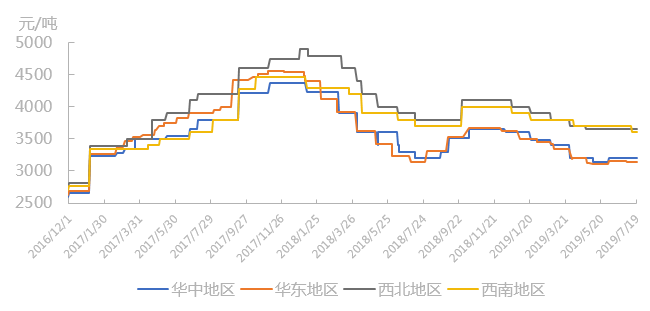

In 2019, the price of commercial prebaked anode continued to go down during this period, and the basic purchase price of Weiqiao prebaked anode also experienced seven price adjustments. The ex-factory price of its anode was 3045 yuan / ton in July, down 415 yuan / ton compared with January. Can the anode market take a turn for the better in the second half of the year?

First of all, from the cost point of view, the price of petroleum coke, the main raw material of the anode, fell-up-down in the first half of the year. After the Spring Festival, the petroleum coke market ushered in a short peak season from March to May. However, since late May, the prices of anode petroleum coke in local refineries and Sinopec have fallen one after another. It is expected that this wave of decline will continue at least until the end of this year's high temperature weather, and it is difficult for the cost end to support the anode price.

On the supply side, the start-up rate of commercial prebaked anode enterprises in June was 65.3%, which was slightly higher than that in May. From a regional point of view, the opening rate of enterprises in central China is still low, Henan small and medium-sized carbon plants according to the order situation, production is not stable, Hubei enterprises operating rate has increased, mainly due to the near southwest, South China aluminum enterprises demand has increased, but due to the Yangtze River along the environmental protection strict inspection, serious port raw materials, finished products loading and unloading speed; East China operating rate rose slightly compared with the previous month, the increment is mainly contributed by large carbon enterprises in Shandong Province.

On the demand side, electrolytic aluminum enterprises purchase anodes on demand, and electrolytic aluminum enterprises due to low profits, the release rate of new and resumed production capacity is relatively slow. From January to June 2019, the domestic electrolytic aluminum production capacity was 14.797 million tons, down 1.6% from the same period last year. It is expected that there will be no significant increase in the anode demand side in the second half of the year, making it difficult to promote the rise of anode prices.

In addition to the fundamentals, there is an uncertainty that can not be ignored in the second half of the year-autumn and winter environmental protection inspection, which will significantly narrow the supply of commercial anodes? SMM believes that the high probability will not reproduce the crazy hoarding market, most of the anode production enterprises that have started at present have completed environmental protection transformation, and although the environmental protection inspection has become stricter, but the policy formulation is no longer "across the board", but more flexible, so that enterprises have more breathing space, so that there will not be a shortage of supply. From the price trend chart can also be seen, anode prices will not rise and fall again in 2017-2018, is gradually showing a narrow range of fluctuations, return to rationality.

SMM Li Hao (021 5166 6863)