SMM7, March 3: with the formal end of the transition period of financial subsidies for new energy vehicles in 2019, the domestic market will also formally implement the new standards of a substantial retreat as a whole, and due to the abolition of the "whitelist" of power batteries, the competition in the new energy vehicle industry is also becoming more and more intense, the washing of dishes in the industry is also accelerating, the possibility of small enterprises being washed out is constantly magnified, and large enterprises are also facing the competitive pressure of enterprises similar to their own size. But from the new energy vehicle data for May, it seems that the "battle" at the depot has only just begun. At the same time, the development pressure of new energy battery production enterprises will also have a great impact on the production and operation of upstream raw material production enterprises.

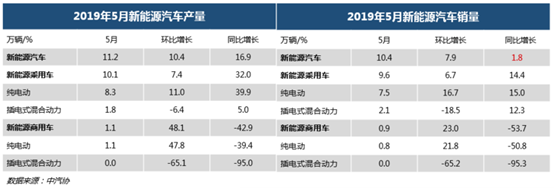

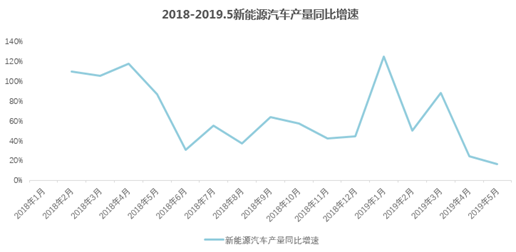

In May, the production of new energy vehicles was 112000, up 10.4 percent from the previous month, up 16.9 percent from the same period last year, and sales reached 104000 vehicles, up 7.9 percent from the previous month, up only 1.8 percent from the same period last year. Although production and sales of new energy vehicles are still growing, it is already the slowest year-on-year growth rate since 2018.

New Energy vehicle Battery production in May 2019

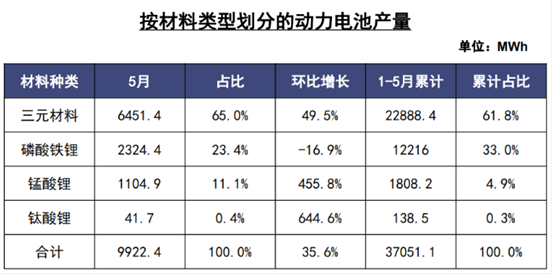

The transition period for new energy subsidies is coming to an end, in addition, the third quarter is usually the off-season of the industry, given that the current mainframe and battery plants are in the process of reshuffling, the strategic directions will be quite different this year. We expect downstream demand for new energy to remain weak in the third quarter, focusing on the implementation of the follow-up double points policy. It is worth noting that in high nickel, the proportion of 8-series products rose to 11%. The positive material factory said that it was the demand raised by the leading battery factory for the preparation of products after the Spring Festival next year, and the demand for 8-series products is expected to grow slowly in the future. In May 2019, the national production of lithium iron phosphate was 8400 tons, down 0.1 per cent from the previous month and up 78.9 per cent from the same period last year. At present, the industry concentration of lithium iron phosphate tends to be stable, and the main demand is still power batteries, but a considerable part of the production capacity has been used in the field of energy storage batteries and consumer batteries. In May 2019, the national production of lithium manganate was 5400 tons, up 0.1 per cent from the previous month and 16.7 per cent from the same period last year. Due to the low energy density and cheap price, the demand structure of lithium manganate in 2018 is mainly consumer batteries. We expect that with the maturity of doping technology in the future, superimposed enterprise cost reduction pressure, the demand structure of lithium manganate can be further optimized in the future, and the demand for high-end lithium manganate may increase.

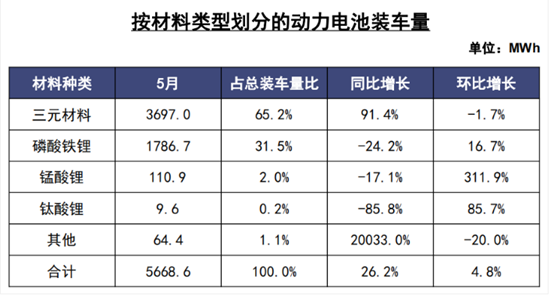

Loading capacity of Power batteries in China in May 2019

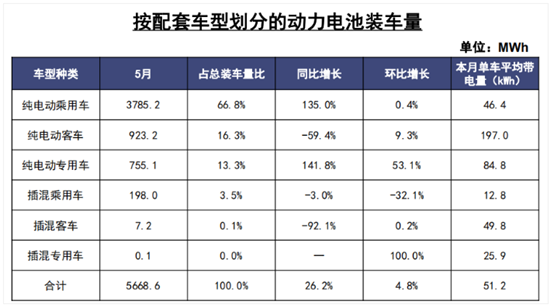

New energy data in May released this week, the development of the new energy vehicle industry in line with expectations, affected by the decline of subsidies, the year-on-year growth rate has slowed. At the same time, SMM power battery installation data show that the total installed capacity of power batteries in May was 5.68GWh, a slight increase of 4.94% from the previous month and an increase of 22.3% from the same period last year. Among them, the installed capacity of ternary battery is 3.75GWh, accounting for 66.1%, and the installed capacity of lithium iron phosphate battery is 1.73GWh, accounting for 30.5%.

Whether it is the production and sales of new energy vehicles or the installation of power batteries, the year-on-year growth rate has been declining since January this year. On the one hand, it reflects that the demand of the new energy industry has been released ahead of schedule; on the other hand, the phased pain of subsidy retreat is still there. How to effectively balance between alleviating the pressure of cash flow and promoting technology research and development is an urgent problem for power battery enterprises this year.

New energy data in May released this week, the development of the new energy vehicle industry in line with expectations, affected by the decline of subsidies, the year-on-year growth rate has slowed. At the same time, SMM power battery installation data show that the total installed capacity of power batteries in May was 5.68GWh, a slight increase of 4.94% from the previous month and an increase of 22.3% from the same period last year. Among them, the installed capacity of ternary battery is 3.75GWh, accounting for 66.1%, and the installed capacity of lithium iron phosphate battery is 1.73GWh, accounting for 30.5%.

Whether it is the production and sales of new energy vehicles or the installation of power batteries, the year-on-year growth rate has been declining since January this year. On the one hand, it reflects that the demand of the new energy industry has been released ahead of schedule; on the other hand, the phased pain of subsidy retreat is still there. How to effectively balance between alleviating the pressure of cash flow and promoting technology research and development is an urgent problem for power battery enterprises this year.

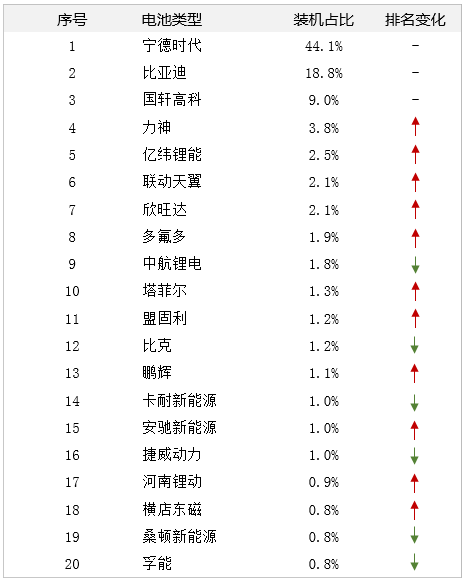

Market share of Power batteries in May 2019

With the exception of TOP3's power battery companies, the ranking of power battery companies changed in May. This also shows that at present, all enterprises are undergoing transformation and change, and it is not easy to get a solid place in the power battery market. Although BYD was still second in the ranking of power battery installations in May, its market share actually fell 10.5% from a month earlier. Although BYD is currently the industry chain integrity of a relatively high degree of enterprise, but because the downstream customer share is still concentrated in the group itself, affected by the group car production and sales volume, the future can continue to expand downstream customers.

As for batteries, China produced 20500 tons of ternary materials in May 2019, down 5 percent from a month earlier and up 64 percent from a year earlier, according to SMM. At the end of the subsidized transition period and safety concerns, manufacturers in Beijing, Zhejiang, Jiangsu and Hunan reduced their orders and reduced production to varying degrees in May. Reducers say signs of a pick-up in demand are unclear.

It is worth noting that in high nickel, the proportion of 8-series products rose to 11%. The positive material factory said that it was the demand raised by the leading battery factory for the preparation of products after the Spring Festival next year, and the demand for 8-series products is expected to grow slowly in the future. In May 2019, the national production of lithium iron phosphate was 8400 tons, down 0.1 per cent from the previous month and up 78.9 per cent from the same period last year. At present, the industry concentration of lithium iron phosphate tends to be stable, and the main demand is still power batteries, but a considerable part of the production capacity has been used in the field of energy storage batteries and consumer batteries. In May 2019, the national production of lithium manganate was 5400 tons, up 0.1 per cent from the previous month and 16.7 per cent from the same period last year. Due to the low energy density and cheap price, the demand structure of lithium manganate in 2018 is mainly consumer batteries. We expect that with the maturity of doping technology in the future, superimposed enterprise cost reduction pressure, the demand structure of lithium manganate can be further optimized in the future, and the demand for high-end lithium manganate may increase. In June, due to the impact of the price reduction of the "National five" models, the market demand for new energy passenger cars shifted, and the production of ternary power batteries was reduced by more than expected. Industry demand is blocked, power battery production is reduced, and the inventory level of upstream positive materials is directly raised. In contrast, as the new energy bus market tends to be saturated, the low mileage passenger car market is less affected by the price reduction of the "National five" models, and the energy storage market demand is gradually starting. The superposition of the three market factors has a positive impact on the production of stable lithium iron phosphate batteries. The overall output of the leading battery factory has been reduced by more than 1/3. At present, the overall operating rate of the power battery industry is less than 30%.

In terms of consumer batteries, the market demand for electric bicycles and electric tools is more optimistic in the near future, which provides a certain support for the output of ternary batteries and lithium manganate batteries. In the traditional 3C market, due to the downstream consumers are still waiting for the progress of 5G, there is little possibility of new and replacement demand this year. It is expected that the demand will remain stable in the second half of the year, and the production of lithium cobalt acid battery will not change much.

With the poor performance of downstream market demand, power battery enterprises and upstream material market began to appear chain effect. According to SMM, there have been a number of power battery enterprises have reduced production to varying degrees, the industry seems to have reached the bottleneck stage of development. Since late May, the cathode material factory has been notified of the reduction of orders from battery companies in June, and the reduction plan is expected to continue into the third quarter. Among these battery companies, including the two leading battery companies, C and B, have been reducing production by about 1 to 3 since June, controlling the start-up rate. In addition, battery factories in Guangdong, Jiangsu and Jiangxi have reduced production to varying degrees.

Battery raw material market

Electrolytic cobalt

In early June, the foreign media cobalt quotation continued to decline, while the domestic mainstream producers have not adjusted their quotations under the influence of low consumption. Although the domestic speculative market is still in the first place, the downstream terminals are mainly waiting and watching under the lack of confidence in the latter situation. Importers say that import costs are high, and falling prices on their own initiative cannot improve sales, so both sides of the transaction hesitated this week, and the actual transaction is weak. In the second week of June, domestic cobalt trading is sporadic, downstream only rigid demand procurement, manufacturers under cost pressure to quote strong, market transactions are difficult. The third week of domestic metal cobalt spot and speculative disk market double downturn, the big factory quotation is strong, but the downstream wait-and-see mood is heavy, the purchase is cautious, the importer in order to promote the transaction, no longer firm quotation. At the end of the month, foreign media prices continued to decline, big factory quotations are strong, intended to wait for foreign media prices to fall to the same level at home and then adjust the quotation according to the market situation. Although the downstream buyer has a wait-and-see mentality, but at the end of the month, this week a small number of prices due to rigid demand, trading prices fell slightly.

June has ended, the subsidy transition period has also ended, the leading effect of the power industry has become more and more significant, Ningde era as a high-quality capacity bargaining power, at present, R & D investment should be put in the first place; BYD industrial chain is complete, the pressure to reduce costs is relatively small. Conduction to the upstream positive material factory, but also gradually affected by the leading effect, the operating rate of each enterprise is different. Most of the main factories are in a wait-and-see situation, the pressure to reduce costs in the industry is still there, or some models may face price increases. At the same time, the industry demand has been released ahead of time, and due to the recent frequent safety accidents of new energy vehicles, downstream demand is not good.

At present, passenger cars are the main growth point of new energy vehicles, and the slowing growth rate will directly affect the demand for ternary batteries. In contrast, lithium iron phosphate batteries are increasing in the market share of special purpose vehicles. In addition, the energy storage market helps stabilize demand. Since late May, the cathode material factory has received the battery enterprise order reduction notice in June, the reduction plan is expected to continue into the third quarter, a leading battery enterprise has begun to officially enter the "high nickel + iron lithium" development route.

For the power battery industry, this year may be a year of reshuffle, adjustment and transformation.

In the market environment and standards, there are not many enterprises to maintain the original price, as of the evening of June 27, only Weima, Xiaopeng, Changan new energy and other car prices remain unchanged.

On the morning of June 28, BYD also announced that all its EV models for sale would remain unchanged after the 2018 subsidy, with a maximum subsidy of 99000 for its models for sale. The current consumer base for BYD's new energy models is larger than other companies, and maintaining subsidised prices in 2018 also guarantees the interests of more potential consumers of new energy. Because BYD's whole industrial chain layout, especially in the core battery aspect has the complete whole industrial chain, has become the BYD can determine the product price important weapon.

SMM believes that the slowdown in the development of the new energy vehicle industry is mainly affected by three factors:

First, industry demand was released earlier than expected at the end of last year and early this year because the new energy subsidy policy was released later than expected.

Secondly, the implementation of the "National six" is just around the corner, and a large number of "National five" inventory vehicles have begun to promote sales in the near future. On the one hand, there are a large number of "national five" inventory vehicles in the four key consumer cities of new energy vehicles in the north, and on the other hand, the prices of new energy vehicles have been raised one after another because of subsidies. This also directly leads to the transfer of part of the new energy consumption demand, has the substitution effect to the new energy vehicle, has increased its shipping pressure.

Finally, there have been a number of safety accidents in the new energy industry since the beginning of the year. Especially after the fire broke out in Tesla, Weilai and other well-known new energy vehicles, it has dealt a serious blow to the confidence of consumers to buy new energy vehicles.

"Click to enter the registration page

Scan QR code and apply to join SMM metal exchange group, please indicate company + name + main business