SMM June 25 News:

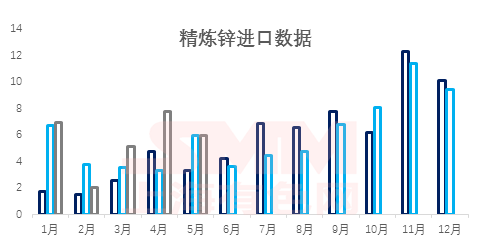

According to the latest customs data from the General Administration of Customs, the import volume of refined zinc in May 2019 was 59300 tons, down 23.57 percent from the previous month, up 0.32 percent from the same period last year, and a total of 277600 tons from January to May 2019, up 19.66 percent from the same period last year.

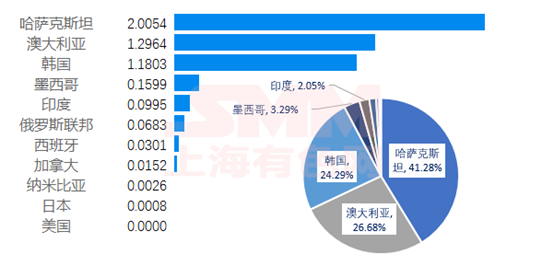

According to customs data, the first five countries to import refined zinc in May 2019 were Kazakhstan (41.28%), Australia (26.68%), South Korea (24.29%), Mexico (3.29%) and India (2.05%). Of these, 59% of Kazakhstan's imports were 1 # zinc, while Australia, South Korea and Kazakhstan accounted for about 92% of the total imports in May. It can be inferred that zinc imports in May are mainly composed of long foreign trade orders.

2 # zinc is not included in the statistics. According to customs data, 2 # zinc imported 10700 tons in May, of which 9900 tons were imported from the United Arab Emirates. According to SMM, due to quality reasons, 2 # zinc is relatively narrow in the domestic market. Only a small number of downstream enterprises will carefully choose 2 # zinc production below the absolute price advantage. The main reason is that 2 # zinc is more serious than 0 # zinc lead and iron content, and since 2018, The monthly import volume of zinc is mostly around 12000 tons, this time a large number of imports or inflows for special reasons, there is no sustainability in the follow-up, this import volume can be taken into account. After excluding the import of 9900 tons of zinc from the United Arab Emirates, the import of refined zinc in May 2019 was 49400 tons, down 36.37 percent from the previous month and 16.48 percent from the same period last year. From January to May 2019, the cumulative import was 267600 tons, up 15.38 percent from the same period last year.

The average Shanghai-London ratio in May was 7.7, slightly higher than that in April 7.62, and the monthly average import loss increased by about 170 yuan / ton to around 1610 yuan / ton. In May, the overseas Back continued to refresh the high value to about US $161 / ton, reaching the level of the Zhuzhou smelter event in that year. Under this background, the LME zinc inventory did not further increase, and the overseas spot contradiction intensified. On the other hand, after the bottleneck of zinc smelting supply was broken, the supply would enter the accelerated recovery period and dominate the domestic market. In addition, the zinc operation in the next phase of macro-bearish extrusion was more weak, and the differentiation and deduction of internal and external fundamentals made the import zinc inflow window more narrow. In the second half of the month, the domestic fundamentals changed, and with the reduction of warehouse receipts and the impact of unexpected events in the smelter, the expected difference adjustment appeared in the recovery of zinc supply, and the contradiction between supply and demand in recent / far months was highlighted. The strong rise in zinc in recent months made the squeeze guess come true. The revision of the Shanghai-London ratio, combined with the profit growth brought about by the accelerated expansion of the domestic monthly difference, all made effective compensation for the import loss, which is conducive to the transfer of bonded area inventories to China. However, from a time point of view, it is not conducive to a substantial increase in imports.

In June, with the end of delivery, the Shanghai-London ratio was revised down rapidly, and the import loss remained at a high level. From a fundamental point of view, the domestic supply will and has returned to a higher level, and the transformation to inventory accumulation is only a matter of time, and the balance between domestic supply and demand will be reached first. At this time, the demand for imports will weaken, and overseas zinc ingots will turn to LME warehouses. From the point of view of transmission logic, it is difficult to open room for internal and external price comparison, and the activity of zinc foreign trade will continue to cool down. Imports in June may be little different from those in May (excluding the high level of 2 # zinc in May, which is calculated to be less than 50,000 tons).