SMM6 22-month news: from the 6th week after the Spring Festival inventory inflection point appeared, SMM statistics national electrolytic aluminum sub-regional social inventory from the beginning of the year high of 1.754 million tons to the current 1.081 million tons, down 670000 tons, a decrease of 38%. From the historical experience, in most cases, there is a negative correlation between aluminum ingot inventory and aluminum price, but in fact, aluminum price has fallen from its highest point since the end of May, but inventory has remained degenerated and failed to maintain the support of aluminum price. What is the reason for this? How will prices and inventories be interpreted in the second half of the year? We try to summarize some rules by reviewing the inventory and price changes over the years.

In most cases, there is a negative correlation between social inventory and price of electrolytic aluminum.

Source: SMM

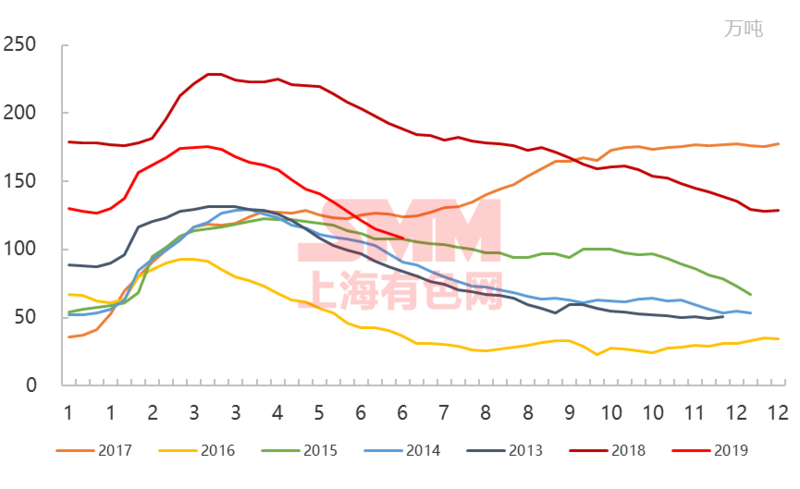

2014: in 2014, domestic spot inventory and spot aluminum prices showed a relatively obvious negative correlation. In April 2014, there was a wave of reduction in electrolytic aluminum production. In line with the domestic economic stimulus policy, aluminum prices once rose to 15000 yuan / ton. At the end of the year, due to the limited actual demand and the release of new production capacity in the fourth quarter, the price fell. The price is ahead of the inventory change under the active accumulation of inventory caused by the reduction of production and the increase of production.

2015: supply exceeded demand in the first three quarters of 2015, social aluminum ingot stocks remained high, and prices continued to fall until November, when the bottom was 9600 yuan per ton. At the end of the year, the production reduction scale of electrolytic aluminum expanded, the production reduction effect quickly caused the inventory of aluminum ingots to fall to less than 700000 tons in December, the spot supply of aluminum ingots became tight, and the aluminum price rebounded synchronously.

2016: after the collapse of aluminum prices in 2015 and the removal of production capacity at the end of the year, domestic electrolytic aluminum prices in 2016 ushered in a full-year repair rebound, especially after the second quarter, the recovery in consumption led to the passive and large loss of electrolytic aluminum, with the lowest annual inventory of 244000 tons, which appeared in October. The increase in profits spurred a restart and the release of new capacity, with inventories at an inflection point in November and aluminium prices peaking at colleagues.

2017: 2017 is relatively special. In the context of supply-side reform, a large amount of money has pushed up aluminum prices, while profit-driven new and resumed production capacity is almost the same as reduced production capacity, factory inventory has accelerated to society, and aluminum prices and inventories have risen at the same time. Aluminum prices rose to a high of 16600 yuan per ton, with inventories approaching 2 million tons by the end of the year.

2018: 2018 price and inventory did not show a strong negative correlation, prices showed range fluctuations throughout the year, highs appeared in January, April and September, prices are periodically affected by export and cost and other factors. During the year, domestic aluminum ingot stocks rose and fell, and continued to decline after the inflection point in March. In 2018, the overall built capacity of domestic electrolysis maintained an upward trend. Excluding the illegal production capacity, the overall built capacity rebounded to 42.55 million tons, an increase of 1.67 million tons, or 4.1 per cent, over the end of 2017.

To sum up, it is not difficult to find that before 2017, inventory is low from a long period, so the price is relatively sensitive to inventory changes, and there is a close negative correlation between inventory and price. After the large accumulation of inventory in 2017, the impact of the absolute change of inventory on the price is weakened, and the price fluctuation range becomes smaller.

2019: thanks to the centralized reduction of electrolytic aluminum production at the end of 2018, and the slow delivery of new production capacity in 2019, it is expected that it will continue to go to the warehouse in the second half of 2019. The dominant factor in aluminum prices in the second half of the year will be the trend of terminal consumption such as costs and real estate.

SMM data: comparison of inventory changes of Aluminum ingots in China from 2013 to 2019

Source: SMM

(SMM Shanghai Nonferrous net Liang Xuan 021 5166 6922)