SMM6, 20 June: on June 18, 2019, Hiro invited Wang Rui, a senior analyst in the SMM aluminum industry, to conduct a conference call to interpret in detail the pricing and balance of alumina, inventory and cost of electrolytic aluminum, external demand and domestic demand, balance and trend of electrolytic aluminum, and so on. "the actual consumption of electrolytic aluminum in China grew by 7.9% in 2016 and 9.1% in 2017," he said. Consumption grew by 3.9% in 2018; China's electrolytic aluminum consumption is expected to grow by 3.0% in 2019. China's electrolytic aluminum production grew by 3.9% in 2016, 14.2% in 2017 and-0.6% in 2018. China's electrolytic aluminum production is expected to grow by 2.24% in 2019. By the end of 2019, inventory is expected to return to the level of 70-800000 tons, and inventory pressure continues to ease in the context of supply-side reform. "

"View the recording of this conference call

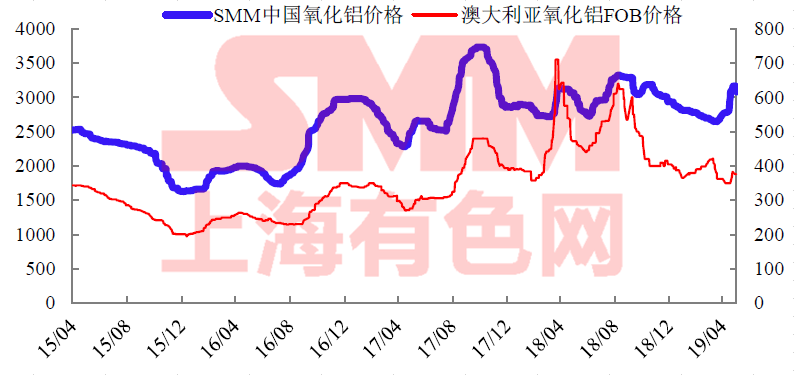

Cost and balance of Alumina

According to SMM statistics, China imported a total of 37.318 million tons of bauxite from January to April 2019, an increase of 40.1 percent over the same period last year, and the immediate cost of alumina enterprises fell by 70 yuan per ton in May compared with March. At present, it is estimated that the average complete cost of alumina is about 2610 yuan / ton, which is about 50 yuan / ton lower than that in March. Among them, Shanxi 2860 yuan / ton, Henan 2890 yuan / ton around. The overall surplus in the third quarter is expected to be about 300000 tons.

Limited Increment of Alumina imports overall surplus in the third quarter

"Click to view the historical price of SMM alumina

After the Spring Festival, the trend of domestic and overseas alumina prices continued to deviate, rising first and then falling overseas, and then rising at home. At present, the alumina import window has been opened. China imported a total of 37.318 million tons of bauxite from January to April 2019, an increase of 40.1 percent over the same period last year.

Although EGA has been put into production, it will still take about a month for Hydro to return to production step by step, but it will still take time for Hydro to return to production step by step. At present, the pattern of supply and demand in the overseas market is tight and balanced, and there will not be too many sources of goods to impact the domestic market in the short term. In April, 18800 tons were exported and 56800 tons imported. About 180000 of new imports were added from July to August.

After the delay of new domestic production capacity, the pace of resumption of production capacity is relatively fast. In 2019, the resumption of production and new alumina production capacity is about 4.4 million tons, but the progress is slow, expected to resume production in June 4 million tons; Norway Hydro resumed production delayed.

A slight shortage of 21000 tons of alumina is expected in June, but there is still an overall surplus in the third quarter.

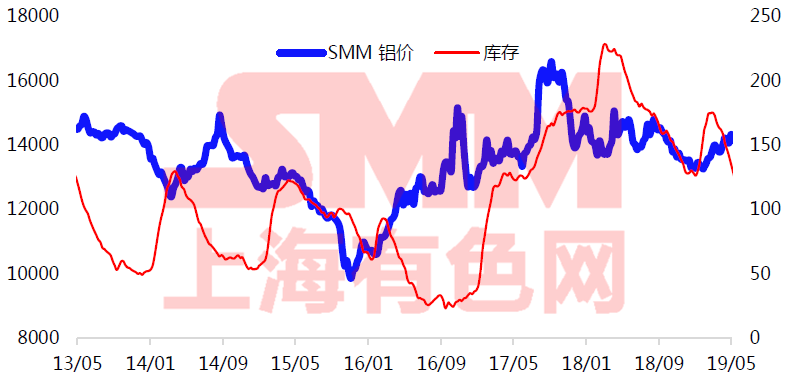

Electrolytic aluminum inventory, profit and production capacity

"View the SMM exclusive database

After the festival inventory changes are basically in line with expectations: SMM data show that as of June 13, SMM statistics of domestic electrolytic aluminum social inventory (including SHFE) totaled 1.118 million tons, down 30, 000 tons from last week. Compared with 1.302 million tons at the beginning of the year, the current electrolytic aluminum inventory has been reduced by 184000 tons, compared with the high of 1.756 million tons at the beginning of the Spring Festival. June-August is the traditional off-season for domestic electrolytic aluminum consumption, and the superimposed export orders show signs of falling. It is expected that the speed of going to storage will slow down. In August, there may be a short period of accumulation. Last year, the stock will be 60-700000 tons, and the stock is expected to drop to 70-800000 tons by the end of the year. From a seasonal point of view, this year's peak consumer season is super-seasonal.

Spring is generally the stage of repairing the profits of aluminum plants: there are obvious seasonal changes in demand in the electrolytic aluminum industry, and there are also seasonal changes in the profits of the industry. The complete average cost of electrolytic aluminum based on the quotation of SMM aluminum related raw and auxiliary materials raises the complete average cost of electrolysis of aluminum related raw and auxiliary materials to 14400 yuan / ton, the average loss of the industry is 400 yuan / ton, but the price of alumina increases too fast, the actual purchasing cost of electrolytic aluminum is not consistent with the quotation, and the average profit and loss level of the industry is still around 50 yuan / ton.

The release rate of new production capacity is still slow: the new capacity is released slowly, with a plan of about 3.06 million tons for the whole year, but the probability is between 200,250 and 250. at present, the progress of resuming production is relatively slow, with the completion of 50, 000 tons of hydropower in the west, and a small amount of resumption of production in Dongxing and extremely slow Weiqiao has been suspended after the maintenance of Yunan headquarters, with a total production capacity of about 350000 tons so far this year.

External demand and domestic demand

In 2019, the economic growth of Europe and the United States has a slowdown trend, overseas consumption will be weaker than domestic, real estate-driven consumption logic is gradually cashed in.

In 2019, the growth rate of domestic consumption will be stronger than that of overseas: 2019 the growth rate of domestic consumption will be stronger than that of overseas, and the logic of real estate-driven consumption will gradually materialize; consumption in Guangdong has improved obviously since April, and the output of aluminum bars and ingots has increased obviously. orders from construction aluminum profile enterprises have improved significantly, but there are signs of weakness in June compared with the previous month; the main drag on consumption in the second half of the year is aluminum and products export orders and cars.

Real estate-driven consumption logic is being cashed in step by step:

In May, the PMI index of the aluminum plate and strip industry was 50.63%, down nearly 7 percentage points from the previous month and 2 percentage points from the same period last year. In terms of sub-items, the index of new orders is basically on the 50-strong line.

PMI, an aluminum foil company, fell 5.5 percentage points in May from April, with the index of new orders still above 50 per cent, while the index of new export orders remained below 50.

Overall orders for construction profiles improved further in May from April, but the index of new orders fell slightly to 49.4%.

The performance of the industrial profile market in May was not as good as that of April, mainly due to the heavy blow to the automobile profile market. June was basically flat.

PMI, a cable company, was 50.2 per cent in May, up nearly 7 percentage points from a year earlier, hovering at the Kurong dividing line, and is expected to maintain its May start rate in June.

In May, the original alloy PMI fell 16.4 percentage points from the previous month to 41.1%, with new orders and production indices below 50%.

The recycled aluminum alloy PMI continued to be below 50 per cent in May, and the recycled aluminum PMI is expected to remain below 50 per cent next month, but is up from this month.

Unforged aluminum and aluminum data began to weaken in April 2019:

Exports totaled 1.442 million tons in the first quarter of 2019, up 13.6% from a year earlier, but it is worth noting that the Shanghai-London ratio averaged 6.7 in the first quarter of 2018, compared with an average of around 7.3 in the first quarter of 2019. In April, it began to fall back to 498000 tons, down 48000 tons from the previous month, and the year-on-year growth rate slowed to 10.4 percent. In May, it was 500000 tons, basically unchanged from the previous month.

One. Export data are sometimes delayed relative to the signing time, with some long orders issued in March, some orders signed in January and production orders from February to March.

II. Expansion of overseas customers last year, for the following reasons: 1. Under the tight monetary policy, the repayment situation of overseas customers is obviously better than that of domestic customers. two。 Take advantage of the historically low price difference between internal and external prices, add new overseas customers, and optimize the customer structure.

Three. When the ratio rebounded, regular aluminum exports did not lose money, but profits were squeezed.

4. The rapid decline in domestic aluminum processing fees, especially the hot rolled coil, has also driven the increase in the proportion of export orders.

However, as the ratio continues to rise, the enthusiasm of enterprises to give priority to overseas orders is weakening, the decline of export orders is only a matter of time, and there is a good chance that there will be feedback on the export data (departure volume) in the second half of the year.

Exports for the whole year are expected to fall slightly by 20-300000 tons compared with the same period last year. Pay more attention to the export of aluminum products (wheels, cans, doors and windows, parts, etc.).

Summary of viewpoints

SMM believes that the long-term trend is still cautiously bullish on aluminum prices, which will weaken in the short term, and the greater risk comes from the inflection point of cost and the uncertainty of demand.

The shift in pricing logic since September 2018: crowding out industry profits-making losses-hitting absolute prices (alumina)-repairing losses-profit in stages under peak season expectations-absolute price increases driven by rapidly rising costs-cost downward expectations superimposed by weak demand expectations.

Viewpoint: the supply rise is weaker than expected, the industry is in the storage cycle, we maintain a cautious view of aluminum prices in the long period, and there is a pullback risk in the short term under the expectation of weaker demand. Under the pressure of overseas alumina prices, the export reduction of aluminum in China is limited, and the US economy has not seen obvious upward signals yet, so the weakness is difficult to change.

Strategy: the relative strength of the non-ferrous plate is still recommended to Shanghai aluminum as a multi-match, the early anti-set position can be closed gradually, but for the time being, it is not recommended to set up with the inside and outside.

SMM teamed up with Hiro to create a high-end report on the metal industry

In order to improve, improve the macro level of in-depth research, and provide more advanced services to customers and friends, SMM teamed up with the top domestic macro research institution, Hiro Mi Road, to create a high-end report that is compatible with macro and metal industry research-"SMM- Mizhiro Metal High end report". Combining the advantages of fundamental research and macro research in the metal industry, the two sides speed up data fusion, while providing industry chain information, study and judge the impact of macro-market and track the circulation and linkage of funds in the metal market, explore market operation opportunities, and provide trading strategies and direction guidance for investors.

A brief introduction to Hiro Tsai Mi Tao:

It is one of the top independent research institutions in China's capital market, providing macroeconomic, broad asset, emerging industries and corporate analysis and investment strategy services to domestic and foreign institutional investors. The company's core team has an excellent educational background and an average of more than 8 years of financial research or industry experience, and has held core business or management positions in influential investment advisers in the current market.

In the aspect of macroeconomic research, this paper analyzes China's economy from the perspective of first-hand data and globalization, and forecasts and tracks the economic data in an all-round way. We should make a forward-looking review of macroeconomic and industrial policies and grasp the cyclical and structural changes in the economy. Using the perspective of globalization and analytical framework, this paper forecasts the trends of the United States, Europe and major emerging market economies. A top-down prospective study of bond and stock markets in major economies. An investment clock perspective based on macroeconomic and policy cycles provides advice on the allocation of large categories of assets such as stock markets, bond markets, interest rate derivatives, industrial commodities, precious metals and agricultural products.

Details of this aluminum report:

If you are interested in the SMM- Hiro in-depth study report, you can apply for a trial

Contact: miss Wu

Tel: 13795448891

"Click to sign up for this summit

Scan QR code and apply to join SMM metal exchange group, please indicate company + name + main business