SMM2 28: the US dollar began to rebound late yesterday, mainly because investors became more cautious about the US-China trade negotiations. Speaking at a hearing of the House ways and means Committee on Sino-US trade issues on Wednesday, US Trade Representative Lettershitzer said that the world's two largest economies have a long way to go to comprehensively improve trade exchanges in the future. There are still many major issues to be addressed in order to reach an agreement and ensure its future implementation. But the outlook for the dollar remains negative after Federal Reserve Chairman Powell stressed patience with interest rate rises in his two-day testimony to Congress. On the oil side, EIA data showed a sharp drop in crude stocks, the biggest drop since July 2018, an unexpected drop in US crude stocks and a surge in crude oil prices in defiance of Mr Trump's accusations by OPEC. The dollar closed at 96.148, up 0.1%. Most of the external metal markets were red, with lead up nearly 1.7%, nickel up nearly 1%, copper up nearly 0.8%, aluminum and zinc up nearly 0.3%, and tin closing down nearly 0.3%. Most of the domestic people also rose, Shanghai lead closed up nearly 1.1%, Shanghai nickel closed up nearly 0.6%, thread closed up nearly 0.5%, Shanghai zinc closed up nearly 0.3%, Shanghai copper and Shanghai aluminum closed up nearly 0.2%, Shanghai and tin closed down nearly 0.2%.

For its part, Powell reiterated the need to be patient with future interest rate adjustments, noting that the US economy faces some "countercurrent and contradictory signals." Analysts expect growth to slow by the end of the year, when the Fed is likely to cut interest rates and launch more quantitative easing. "the baseline outlook is good, but the slowdown in overseas economic growth is a drag on the US economy, and we are likely to feel that more in the coming months," he said. We have the conditions for good prospects, our committee is indeed monitoring the opposite trends and risks, and for now, we will be patient with our policies and allow time to clarify everything. "

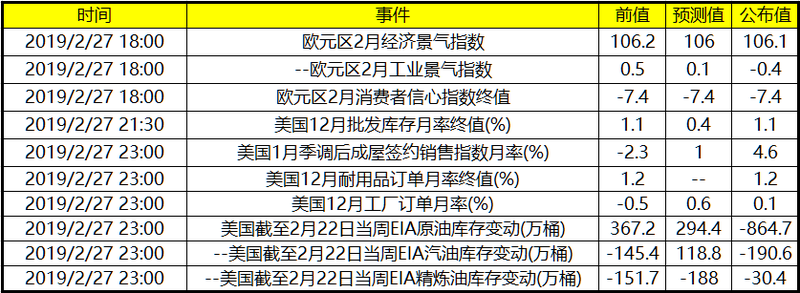

In terms of data, the euro zone's economic sentiment index for February was 106.2, expected to be 106, and today's value is 106.1. Eurozone industrial sentiment index for February, previous value: 0.5 (revised: 0.6), expected: 0.1, current value:-0.4. The final value of the euro zone consumer confidence index for February, the previous value:-7.4, expected:-7.4, today's value:-7.4.

Weidmann, ECB governing committee and president of the Bundesbank, is in no hurry to adjust the ECB's forward-looking guidelines. The basic expectation is still to normalize monetary policy. It is unreasonable to question Germany's medium-term economic prospects. It takes a reasonable reason to implement the new TLTRO.

Us wholesale inventory month-on-month final value in December, previous value: 1.1%, expected: 0.4%, current value: 1.1%. United States merchandise Trade account for December ($100 million), previous value:-705 (revised:-772), expected:-739, current value:-795.

U. S. trade account data for December: due to falling exports, imports continue to increase, the U. S. commodity trade deficit rose sharply in December, reaching an all-time high. The U.S. trade deficit soared to $79.5 billion in December from $70.5 billion the previous month, well above expectations of $73.6 billion, according to the Commerce Department. Exports fell 2.8% from a month earlier to $135.718 billion.

Us durable goods orders for December month-on-month final value, previous value: 1.2%, expected: -, current value: 1.2%. Us factory orders month-on-month in December, previous value:-0.6% (revised:-0.5%), expected: 0.6%, current value: 0.1%.

December factory order rate: December factory order rate rose slightly due to weaker demand for mechanical and electronic equipment and parts. The growth of manufacturing orders has slowed as the stimulus to capital expenditure from tax reform has abated. In addition, export orders have been affected by a stronger dollar and slowing economic growth in Europe, and lower oil prices have also affected purchases of crude oil and natural gas drilling equipment.

U.S. oil production rose 100000 barrels a day to 12.1 million barrels a day, a record high in a week, according to the U.S. Energy Information Administration (EIA):). Capacity utilization at refineries on the east coast fell to 60%, the lowest since 2012. In the week of February 22, U. S. oil imports hit a one-week low since 1996. Net oil imports from the United States hit a one-week low. The United States imports 346000 barrels of oil a day from Saudi Arabia, a one-week low. Cushing crude stocks hit a weekly high since December 2017.

Financial blog zero hedge review of US EIA data for the week: this morning's API data showed an unexpected drop in US crude stocks after Saudi Arabia hinted that OPEC and allies would continue to cut production. WTI crude oil rose. Vince Piazza, an energy analyst, said the balance of the crude oil market had tightened as OPEC cut production. EIA data also showed a sharp drop in crude stocks, the biggest drop since July 2018. Although the number of US drilling began to decline, US crude oil production is still at a high of 12 million barrels per day. After the release of the EIA data, WTI crude continued to pull higher.

Important overnight financial data are as follows: