Money Metals News Service June 8th, 2017

The market has no clue that it has severely undervalued the price of gold. While Central bank intervention has worked hard at capping the gold price, the “Great Gold Supply Disconnect” will most certainly remedy that situation. This gold supply disconnect took place after the gold price peaked in 2011.

That being said, the world is speeding recklessly towards an epic market catastrophe. No, this isn’t hype... I wish it was. But, unfortunately, the poor folks who continue to believe their STOCK, BOND & REAL ESTATE portfolios will provide them with a healthy retirement in the future, have no idea that their true values evaporated many years ago. However, the market just hasn’t BAKED THEM INTO THE CAKE YET... LOL.

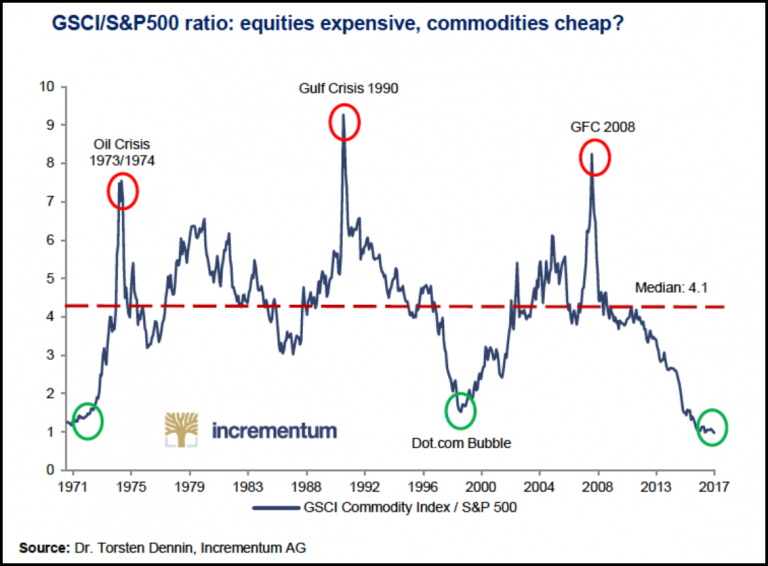

Before we get to the Gold Supply Disconnect, let’s look at this wonderful chart that shows the carnage taking place in the commodity market. This is “Commodity Index” divided by the S&P 500 Index:

This chart shows that the commodity index is at the lowest ratio to the S&P 500 since 1971. Thus, the commodity prices have reached a 50 year low versus the S&P 500. Moreover, the commodity index is lowest ratio (below 1.0) when we compare it to the average median which is 4.1, shown as the red dotted line on the chart. Now, either commodity prices are too low, or the S&P 500 and its illegitimate older brother, the Dow Jones Index are severely over-inflated.

I would like to remind investors, without a properly functioning commodity supply market, companies wouldn’t be able to produce and manufacture their products. Which means, energy and commodities are the foundation of our markets.

Of course, if an individual still had a semi-functioning brain-stem and wasn’t one of the millions of Americans now suffering from serious BRAIN DAMAGE, they would realize that the stock markets are in record bubble territory.

Now, another thing that it totally overlooked by most Americans and the Mainstream analyst community is how the falling oil price is gutting the U.S. and global oil industry. Today, we received news of one of the largest U.S. gasoline and distillate inventory builds in the past five months. However, if we look at the total U.S. Oil/Product SPR inventory, it rose the most since August 2015.

This had a wonderful impact on the price of U.S. crude oil...... which is now down $2.15 to $46.05 a barrel. This low oil price continues to gut the U.S. oil industry even though the media suggests that the Shale Oil Industry is now profitable at $20-$40 a barrel. I will be publishing an article shortly on the Permian Basin in Texas, which is now the Darling of Wall Street and the U.S. shale oil Industry. Everyone is jumping into the Permian to make that big money... or so they believe.

Regardless... collapse is on its way because the very energy we use to run everything is rapidly disintegrating. And without energy, the global gold supply would most certainly evaporate into thin air.

THE GREAT GOLD DISCONNECT: How The Market Has Severely Undervalued The Gold Price

The Fed and Central bank magicians have fooled the audience with a clever slight of hand that a newly printed $100 bill, which costs 13 cents each to produce, is worth $100 in gold, it isn’t. However, the skyrocketing gold price hasn’t been BAKED INTO THE CAKE YET, but it will.

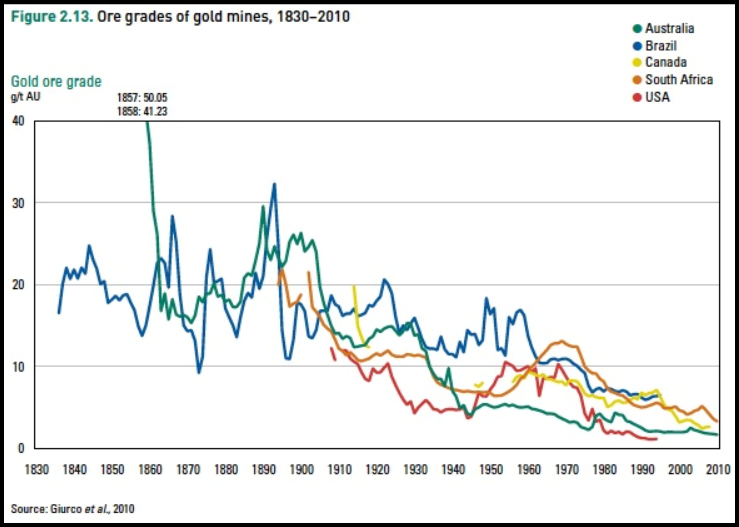

Before I show you the Gold Supply Disconnect, let’s look at this interesting chart which show the falling ore grades of five different gold producing countries:

At one time (1900), the average gold ore grade in the world was over 20 grams per ton... 32 grams equals one troy ounce. Today, the top gold miners are struggling to produce gold at a little more than 1.2 grams per ton. Back when Nixon dropped the U.S. Dollar-Gold peg in 1971, the average gold ore grade from these five countries was approximately 8-10 grams per ton... nearly EIGHT TIMES higher than today.

When means, the gold mining industry is now producing the most expensive gold dust in history.... and doing so for mere peanuts.

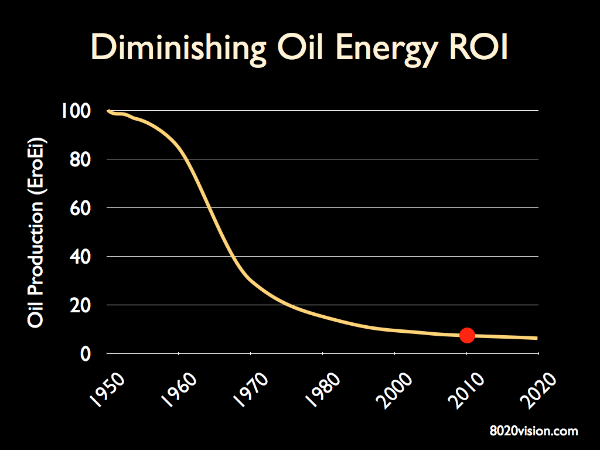

Furthermore, we also have the falling EROI – Energy Returned On Investment of oil that is used to extract and produce gold:

Thus, falling global gold ore grades and the declining EROI of oil means it costs a great deal more to produce gold today than it did in the 1900’s and especially in the past 15 years. However, the profitability and the share prices of the top five gold miners have suffered greatly since the gold price peaked in 2011.

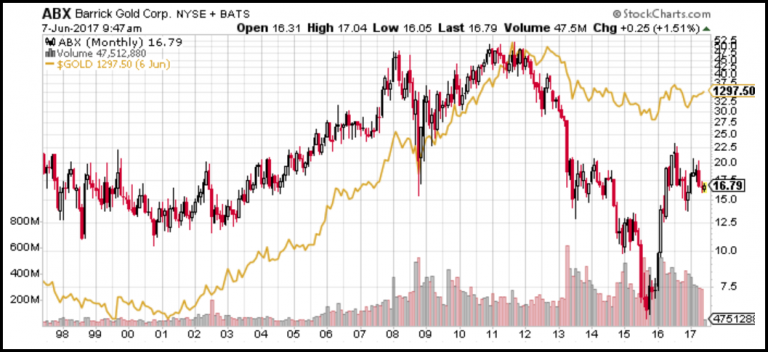

If we take a look at the next five charts, we can see that the gold miners share prices have under-performed the gold price since the beginning of 2012:

BARRICK GOLD

NEWMONT

ANGLO-GOLD

GOLDCORP

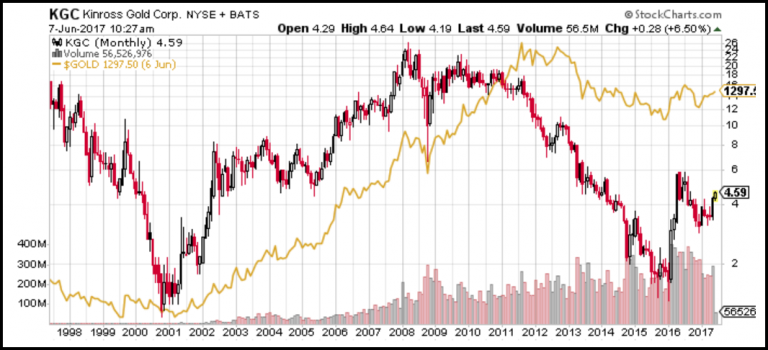

KINROSS GOLD

You will notice in all five charts, the price of gold (Gold color) was underneath all the gold mining companies stock price trend up until 2011. Then after 2012, the Great Gold Disconnect took place as the gold price is now higher than these companies share prices. Some of these gold miners share prices are much lower than the gold price trend, such as Kinross Gold, AngloGold and Barrick.

What is quite amazing is that Kinross (ranked 5th largest gold miner) produced 2.7 million oz of gold in 2016, and its share price is currently trading at less than $5. Think about that. Kinross produced $3.8 billion worth of gold in 2016, and its share price is trading at less than $5 a share. Now, compare that to the first chart in article (above) which shows the commodity index trading at a 50 year low versus the S&P 500 Index.

What we have today is a totally insane and hyper-inflated STOCK, BOND and REAL ESTATE market, and a severely under-valued gold market price and gold mining shares.

The investors of the world believe the hyper-inflated values of STOCK, BONDS and REAL ESTATE will continue indefinitely. Unfortunately, the gold supply disconnect that took place in 2011 is a big RED WARNING LIGHT that the something is seriously wrong.

When the broader stock, bond and real estate markets start to crack and drop like a rock, watch for the gold price and the mining shares to head in the opposite direction.

![Platinum Prices Fluctuated Downward Intraday, and Spot Market Transactions Continued to Weaken [SMM Daily Review]](https://imgqn.smm.cn/usercenter/obeMy20251217171735.jpg)

![Silver Prices Remained in the Doldrums as Month-End Approached, Suppliers Were Reluctant to Sell and Waited on the Sidelines, and Market Transactions Were Thin [SMM Daily Review]](https://imgqn.smm.cn/usercenter/ipCjz20251217171734.jpeg)