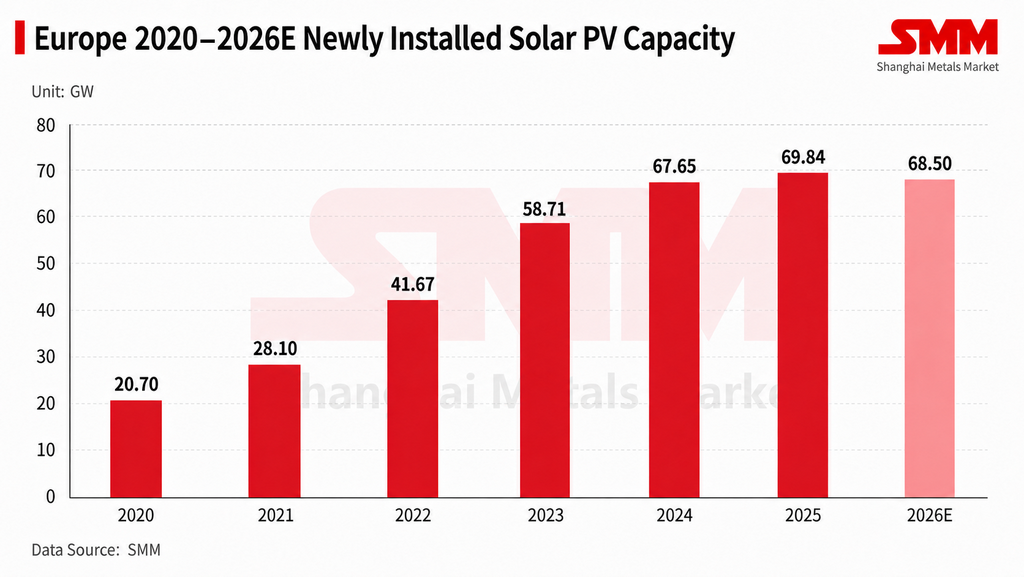

Europe's Solar Market Growth Slows Notably in 2026

Since the start of the year, growth in the European solar market has slowed markedly. SMM expects total new solar installations in the European market to fall to around 68.5GW in 2026, a year on year decline of about 2 percent. Alongside softening demand, multiple EU level supply chain restriction policies continue to advance, including the Net Zero Industry Act (NZIA), the Industrial Accelerator Act (IAA), and restrictive measures targeting inverters from so called high risk countries. These are affecting supply chain selection, project access, and the competitive landscape for enterprises in the European solar sector.

However, the effect of these policies on the European solar market is showing up mainly as a rise in supply chain thresholds, rather than as a direct boost to end market installations. The relevant policies raise requirements around supply chain origin, carbon footprint, and the security of key equipment, which objectively favors European domestic manufacturing and supply chain diversification. But domestic manufacturing costs remain significantly higher than those of imported products, and project returns remain under pressure. In the short term, these policies are functioning more to raise the threshold for market access than to serve as a core driver of growth in end market installations.

Demand structure diverges, with Eastern Europe and the UK and Ireland absorbing part of the increment

Growth in Europe's distributed market has remained relatively steady, while utility scale projects are constrained by factors including project returns, grid connection conditions, grid absorption capacity, and power price volatility, with the pace of some projects being delayed. Compounded by frequent negative electricity prices, elevated financing costs, and longer grid connection timelines, developers are becoming more cautious in advancing new utility scale projects.

At the regional level, this year's incremental demand in the European market has shifted more toward Eastern Europe, the UK, and Ireland. The Eastern European market mainly includes Romania, Ukraine, and Poland, where some markets still present opportunities for project pipeline release and channel expansion. The UK and Ireland are benefiting more from distributed demand and potential policy support going forward. At the same time, shipment pace into traditional core markets such as Germany has slowed, and the center of gravity of European demand is gradually shifting from mature core markets toward incremental regions and distribution channels.

After the end of the summer off season, a modest recovery in demand is expected in the European market from the end of the third quarter into the fourth quarter, but this will be followed by the winter off season, and the pace of demand release in the second half of the year is still unlikely to improve significantly. Under the current geopolitical situation, Europe's push for energy self sufficiency has strengthened, which over the long term favors the logic of renewable energy development. But in the short term, the pace of installations remains constrained by project returns, grid absorption capacity, and the pace of policy implementation, limiting the actual boost to full year installations.

Technology paths accelerate their divergence, demand rises for high power products

The European market is showing relatively clear differentiation by scenario. In the Western European distributed market, back contact (BC) modules have generally outperformed conventional TOPCon products, benefiting mainly from their higher efficiency, better appearance, and distributed customers' greater acceptance of the associated premium. In utility scale power stations, however, the application scale of BC modules remains limited and is still in a market validation phase. Module price, system cost, delivery stability, and long term reliability remain the more critical decision factors for large scale projects.

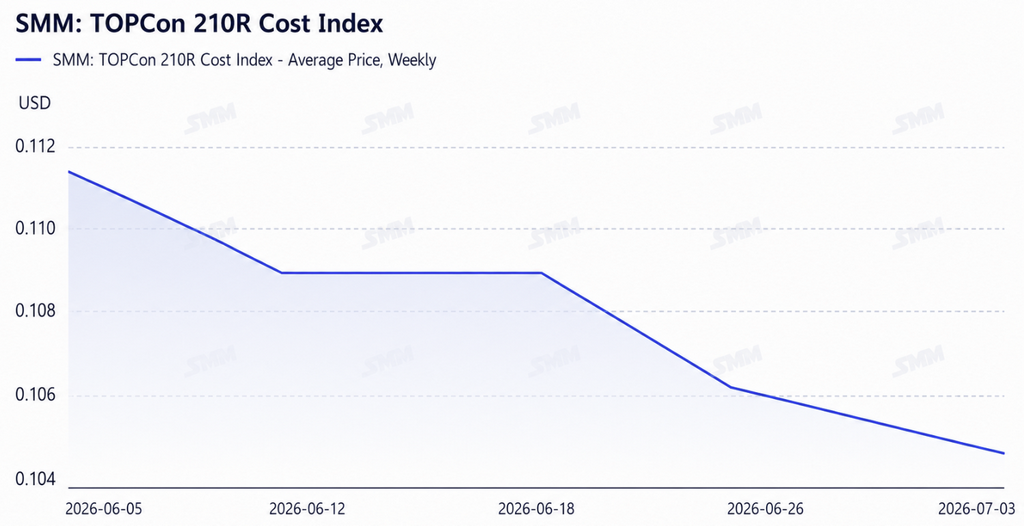

TOPCon currently remains the mainstream technology route at the project level in Europe, but demand for multi busbar, high power products is rising. According to SMM, some developers and EPC contractors hope that the power output of 210R (G12R) modules for projects to be delivered by the end of 2026 can reach around 650W, while the current mainstream power range for modules is still concentrated around 630W. Going forward, power output, efficiency, format compatibility, and stable delivery capability are expected to become important criteria by which project developers select suppliers. This trend is expected to further concentrate demand toward high power products, but in the short term it is unlikely to shift to a single technology route. Enterprises with mass production capability for high power TOPCon will continue to dominate at the project level, while differentiated products such as BC modules will find their place more in distributed and high premium scenarios.

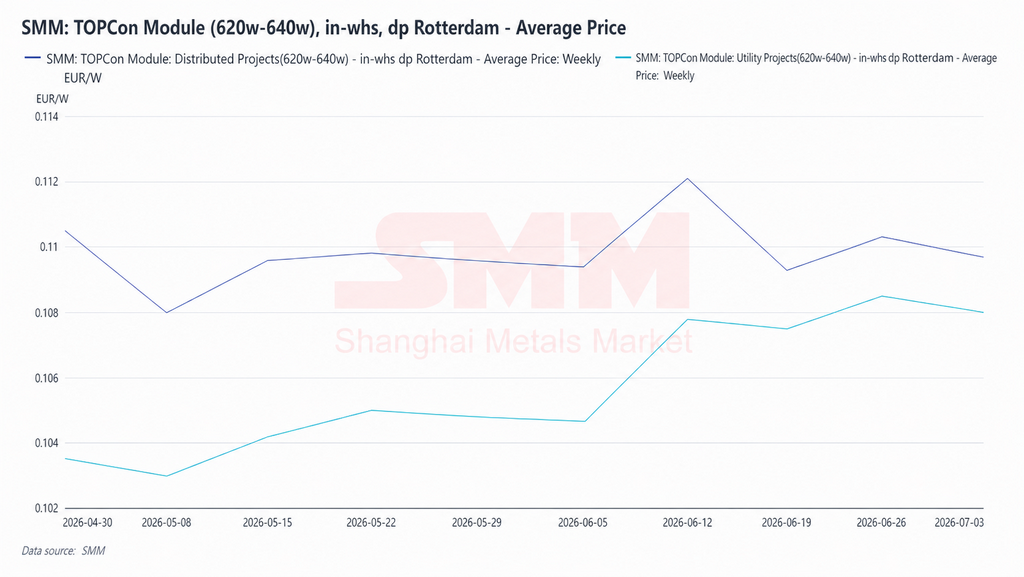

Module prices remain under pressure, with the FOB and European spot price gap widening

The overall European module market remains at a low level of operation, with pressure on FOB export prices being more pronounced. Affected by factors including weaker demand, delayed project progress, and ongoing shipment pressure, some module manufacturers have offered lower prices at various stages in order to maintain order volume, channel share, and cash flow, and price competition remains intense. Industry feedback broadly indicates that loss pressure at the module segment continues, with some low priced orders already approaching the cash cost range for enterprises, and that shipments are more about maintaining cash flow and market presence than pursuing clear profit.

According to SMM, TOPCon module prices in the current European market remain in a relatively pressured range, with competition particularly evident at the project level. At the same time, a phased pullback in the price of silver and other auxiliary materials has also brought module costs down somewhat, reinforcing market expectations for further declines in FOB prices going forward. By comparison, European local spot prices have not fully followed export prices downward in sync, and the gap between the two has widened recently. Beyond inventory costs and the pace of spot turnover, ocean freight rates rising notably from their level earlier in the year is also one of the reasons pushing up landed costs. European local spot prices remain supported in the short term by transportation costs and inventory turnover, and the extent of any further decline is expected to be relatively limited.

If the strength of demand recovery is limited toward the end of the third quarter, and combined with the fourth quarter entering the winter off season, European module prices will still face downward pressure, and the pace of price decline between the export side and the local spot side may continue to diverge. As profitability remains under sustained pressure, expectations of industry consolidation are rising, and enterprises lacking technology iteration capability, channel advantages, and financial support may face further increased operating pressure in the European market going forward.

Enforcement of inverter and Net Zero Industry Act related policies diverges

At the EU level, constraints on the solar supply chain currently center mainly on two areas: first, financing restrictions by financial institutions on inverter projects sourced from so called high risk countries, and second, the implementation of guidance related to Article 28 of the Net Zero Industry Act. In terms of enforcement, the Net Zero Industry Act is targeted more at individual projects, and if the products actually used in a project are inconsistent with what was declared, penalties may follow. The market broadly views this policy as moving forward at a relatively fast pace.

However, because the EU has free trade agreements with a number of regions, products manufactured in those regions can still enter the European project system provided conditions are met. The actual target of the policy's constraints is concentrated more on Chinese supply chains themselves, rather than on all non EU origin products. For suppliers with overseas production capacity, capacity based in free trade agreement regions, or a more complete compliance path, there may be a certain access advantage at the European project level going forward.

Looking at the differences by segment, restrictions on inverters are relatively more workable in practice, mainly because European domestic and non Chinese capacity is relatively abundant, giving project developers more room to choose alternative suppliers. At the module segment, because European domestic manufacturing costs are significantly higher than those of imported products, even with added policy support, large scale reshoring of manufacturing in the short term still faces constraints on economic viability. With European electricity prices currently volatile and project returns already under pressure, in the absence of hard policy restrictions, developers' willingness to purchase high priced domestic modules at scale remains limited. Without sufficient subsidies and a path for costs to fall, domestic module manufacturing is still unlikely to form direct cost competitiveness against Asian supply chains in the short term. The policies are functioning more to drive supply chain origin restructuring and compliance path adjustment, rather than quickly driving large scale ramp up of domestic capacity.

European domestic manufacturing explores differentiated routes, while supply chain support is still being built out

At this exhibition, a considerable proportion of European module manufacturers displayed products related to heterojunction (HJT) technology. In contrast to the route followed by Chinese capacity, which generally centers on iterating TOPCon with continuously rising power output, European domestic module manufacturers are more inclined to maintain their market positioning through differentiated routes such as HJT, low carbon modules, lightweight modules, and anti glare modules.

European enterprises' choice of HJT is more a realistic choice made under a cost disadvantage than purely a technology preference. Domestic manufacturing costs are significantly higher than those of mainstream Chinese products, and it would be difficult to form an advantage by directly entering the already highly scaled and intensely price competitive TOPCon route. HJT differs to some degree from mainstream products in process and product performance, which objectively helps avoid direct price competition. The production process involves relatively fewer high temperature steps, and in theory the energy consumption and carbon footprint per unit of product are lower, which fits reasonably well with the European market's emphasis on low carbon manufacturing and supply chain traceability requirements, giving it a certain narrative space in policy supported projects and the high end distributed market. Some enterprises also view it as the technical foundation for subsequent perovskite tandem cells, since the characteristics of the low temperature process are suited to serving as the bottom layer structure of a tandem cell, and are therefore advancing perovskite research and development in parallel with their HJT deployment. Europe and its surrounding regions also have a certain accumulated industrial base in HJT equipment, and continuing to use existing equipment and process foundations is more coherent than switching entirely to a TOPCon production line.

At present, HJT's share of overall European module shipments remains limited, and the utilization rates and supply stability of most domestic enterprises have not yet formed a scaled advantage. Whether it can be ramped up going forward still depends on efficiency improvements, cost declines, and end customers' acceptance of the associated premium. On perovskite, the research and development of some European enterprises currently remains at the pilot verification stage. Given that European projects generally require relatively long warranty periods, issues around efficiency degradation and long term stability have not yet been fully resolved, and in the short term this remains more a direction for technology reserve, with limited impact on the current supply and demand landscape for modules.

Solar plus storage integration is gradually becoming a focus of attention, as negative electricity prices add to earnings uncertainty

As grid absorption pressure rises in parts of Europe, negative electricity prices are occurring more frequently. Take April 26 of this year as an example: negative prices in parts of Central and Western Europe reached around negative 500 euros per MWh, and the overall lowest price in Europe was even close to negative 2000 euros per MWh. The main reason is the rapid increase in solar installations, with electricity supply during the midday generation peak clearly exceeding the local grid's absorption capacity. Against this backdrop, judging European market demand purely from module shipment data has become insufficient. Storage configuration capability, grid connection conditions, and project returns are becoming important variables affecting the pace at which European solar projects move forward.

The focus of developers, EPC contractors, and investment institutions has gradually shifted from module price alone toward the overall return performance of solar paired with storage, including electricity price volatility, storage arbitrage space, grid connection conditions, project payback period, and long term cash flow stability, with storage's impact on the pace of new installation release becoming more direct. With utility scale project returns under pressure and grid connection difficulty rising, solar plus storage integration is becoming an important area to watch in the European market. If storage configuration can effectively improve project economics and ease curtailment and negative price pressure during certain periods, some delayed European projects still have a chance to restart. But if storage costs, grid connection rules, or electricity pricing mechanisms fail to provide effective support, the pace of demand release in the European solar market may continue to be constrained.

Indian module enterprises have limited competitiveness in the short term, as their path overseas becomes more diversified

Although EU level policy is pushing for diversification of supply chain origin, which objectively creates certain opportunities for non Chinese supply chain regions, feedback from the exhibition and from enterprises indicates that cost and price advantages remain the main threshold for outside enterprises entering the European market. In the short term, it will still be difficult for Indian module enterprises to achieve a substantive increase in share in Europe.

Chinese module enterprises still hold clear advantages in cost, price, delivery capability, and overseas channels, while Indian module enterprises' brand influence, channel foundation, and customer recognition are relatively limited by comparison. Even as policy encourages supply chain diversification, project developers will still prioritize a combination of price, quality, delivery time, and financing conditions when actually procuring. On the Indian domestic side, policy continues to advance restrictions on supply chain access, and annual installation demand is expected to remain at around 40 to 45GW, with capacity expansion not matching the pace of demand growth. Consolidation and concentration toward leading enterprises in the domestic module industry are expected to continue, and while some enterprises still have room to grow under policy support, they also face pressure from rising costs, declining project returns, and a slower short term pace of installations.

As a result, some Indian enterprises have already begun adjusting their overseas strategy, entering the international market more through project development, EPC contracting, investment, or other supporting business segments, rather than relying purely on module products to compete on price. For enterprises with group level resources, project development capability, and financial support capability, going overseas by using projects to bring modules along may be more feasible than competing directly on module price in the European market.

Market Short-term Outlook

Against the combined backdrop of slowing demand growth, the gradual implementation of policy constraints, and intensifying supply chain competition, the European solar market is moving from a past stage centered on installation scale expansion and low price module competition, toward a new stage that places equal weight on technology route differentiation, supply chain compliance, and return structure optimization. In the short term, the European market will still face issues including weak demand release, project delays, price pressure, and relatively high domestic manufacturing costs. A phased demand recovery may occur from the end of the third quarter into the fourth quarter, but this is unlikely to reverse the overall trend of slowing demand for the year. Over the medium to long term, the European solar market still has support from energy transition demand, but the pace of subsequent growth will depend more on the strength of policy implementation, progress in storage configuration, improvement in grid absorption, and the actual progress of domestic manufacturing coming online.

SMM believes that starting in 2026, demand in the European solar market is not disappearing over the long term, but rather that the logic behind how demand is released is changing. Going forward, assessing the European market cannot rely only on module prices and short term shipments, but must also incorporate project returns, storage configuration, policy compliance paths, and progress in supply chain restructuring into a comprehensive evaluation.

Written by:

Ryan Tey Tze Yang | SMM PV Analyst

+60127179370 | ryan.tey@metal.com

![[SMM PV News] Jinko Energy Storage Secures 400 MWh Utility-Scale Energy Storage Project in Eastern Europe at Intersolar, Partnering with Taliva to Advance Energy Infrastructure](https://imgqn.smm.cn/usercenter/FtiwK20251217171741.jpg)

![[SMM PV Flash]Advanced manufacturing moves towards "green", and Canadian Solar Inc. helps Lianxun Instruments build a green energy system.](https://imgqn.smm.cn/usercenter/oytJq20251217171740.jpg)

![[SMM PV Flash] Full-Stack Solutions Linking the World, Risen Energy Empowers Markets Outside China with Professional Services](https://imgqn.smm.cn/usercenter/RGBgE20251217171739.jpg)