I. Event Confirmation: US-Iran MOU Signed and Effective Ahead of Schedule

According to CCTV News, the United States and Iran remotely signed a memorandum of understanding aimed at ending the war and reopening the Strait of Hormuz on June 17, and the agreement has now taken effect. U.S. President Trump personally signed the document. The signing ceremony, originally scheduled for June 19 in Switzerland, was moved up, with both sides accelerating the timeline to reopen the Strait earlier than June 19.

The document, titled the "Islamabad Memorandum of Understanding between the United States of America and the Islamic Republic of Iran," contains 14 articles, with key provisions including:

- Immediate and permanent cessation of military operations on all fronts, including Lebanon;

- The U.S. to immediately begin lifting its naval blockade on Iran, with full completion within 30 days, and vessel traffic to return to pre-war levels;

- Iran to complete demining and other necessary work within 30 days to restore normal passage;

- The U.S. commits to working with regional partners to invest at least $300 billion in Iran's reconstruction;

- The U.S. commits to terminating all sanctions against Iran and unfreezing Iranian assets;

- Iran reaffirms it will not acquire or develop nuclear weapons and agrees to dispose of enriched material stockpiles under IAEA supervision.

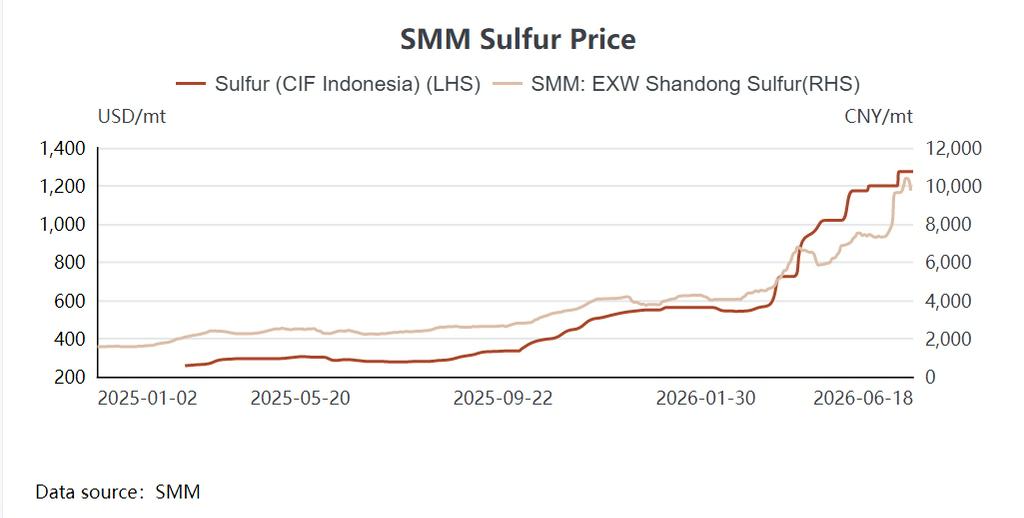

II. Historical Price Review: The Extreme Rally from 4,000 to 12,000

The sulfur price movement in this cycle can be divided into three distinct phases:

Pre-conflict stability (Jan–Feb): SMM EXW Shandong Sulfur traded in the 3,950–4,300 yuan/t range, while SMM CIF Indonesia Sulfur was quoted at $540–570/t, with supply and demand in balance.

Conflict-driven surge (Mar–May): Following the outbreak of the US-Iran conflict in late February, the Strait of Hormuz blockade nearly halted Middle Eastern sulfur supply. SMM EXW Shandong Sulfur surged from around 4,150 yuan/t in early March to above 7,500 yuan/t by late May, while SMM CIF Indonesia Sulfur rose from $540/t to $1,200/t. Domestic port inventory dropped from over 2 million tons at the start of the year to below 900,000 tons by early June.

Panic peak (early June): Prices accelerated to their peak in early June, with SMM EXW Shandong Sulfur hitting 10,707–11,750 yuan/t on June 11–12, and SMM CIF Indonesia Sulfur stabilizing at $1,250–1,300/t. After the ceasefire news broke on June 15, market sentiment reversed sharply, with SMM EXW Shandong Sulfur falling back to 9,507–10,000 yuan/t in a single day.

III. Scenario Analysis: Three Paths After the Agreement

Scenario 1: Baseline (probability ~50%) – Smooth implementation, gradual supply recovery

The agreement has been signed and is effective. The U.S. has begun lifting its naval blockade, and Iran is to complete demining within 30 days. Shipping companies are expected to resume normal passage after 1–2 weeks of observation, with backlogged cargoes gradually arriving at importing markets through mid-to-late July. Domestic port inventory is expected to remain low through the end of July, with gradual recovery starting in August.

Price forecast: SMM CIF Indonesia Sulfur is expected to fall to around $1,000/t within two weeks (early July), break below the $1,000/t mark within three weeks (mid-July), and further decline to $800–900/t by August. SMM EXW Shandong Sulfur is expected to retreat to 6,500–7,000 yuan/t.

Scenario 2: Optimistic (~30%) – Smooth passage, rapid supply recovery

Demining is completed ahead of schedule, shipping recovers quickly, backlogged vessels are cleared rapidly, and Middle Eastern refineries resume production sooner than expected, with large volumes arriving as early as early July.

Price forecast: SMM CIF Indonesia Sulfur will quickly fall below the $1,000/t mark within two weeks and decline to $800–900/t within three weeks. SMM EXW Shandong Sulfur is expected to drop to 5,500–6,500 yuan/t.

Scenario 3: Pessimistic (~20%) – Follow-up talks within 60 days collapse

Both sides have committed to reaching a final agreement within 60 days. If negotiations stall, the conflict could resume.

Price forecast: SMM CIF Indonesia Sulfur will return to above $1,300/t, and SMM EXW Shandong Sulfur will rebound to above 10,000 yuan/t.

IV. Conclusion: Direction Clear, Timing Uncertain

The direction of reopening the Strait of Hormuz is now clear—the agreement has been signed and is effective, the U.S. is lifting its blockade, and Iran is to complete demining within 30 days. The geopolitical premium in sulfur prices will gradually fade. However, the pace of supply recovery remains uncertain—demining progress, shipping safety assessments, clearance of backlogged capacity, normalization of insurance costs, and refinery restart timelines all require time to materialize.

The next 2–4 weeks will be a critical window for sulfur prices, as the market transitions from "geopolitical sentiment pricing" to "fundamental supply-demand pricing." Under the baseline scenario, SMM CIF Indonesia Sulfur is expected to break below the $1,000/t mark within three weeks, though returning to the $800–900/t range will take longer. Going forward, close attention should be paid to demining progress, port arrival schedules, and the direction of final agreement negotiations within the 60-day window.