I. Overseas Markets: Driven by Two Core Catalysts – Surging Demand for Stationary Power Generation, Supply Constraints Hinder Aviation Green Hydrogen Rollout

(I) European Off-Grid Stationary Fuel Cells Secure Repeat Bulk Orders; Overseas OEMs Restructure Revenue Mix

Ballard Power Systems, Canada’s leading fuel cell manufacturer, unveiled a landmark repeat order on June 15: a second 15 MW fuel cell system supply contract from a UK renewable off-grid power producer. The order covers 150 sets of 100 kW automotive-grade fuel cell modules, slated for delivery in H2 2026. These modules will be integrated into hydrogen power generators to replace conventional diesel gensets, serving off-grid power needs at construction sites, film production sets, large-scale events, and critical infrastructure.

Underpinning demand remains robust: multiple European nations have rolled out policies phasing out diesel generators for construction and cultural tourism applications. Coupled with prolonged grid connection lead times for industrial parks and data centers, demand for zero-carbon off-grid power sources has expanded rapidly. UK-based GeoPura has deployed Ballard fuel cells at scale to operate charging stations and construction site power supplies, validating the technology’s commercial viability.

Strong earnings reflect booming market momentum. In Q1 2026, Ballard’s stationary fuel cell business posted USD 5.2 million in revenue, skyrocketing 775% year-on-year to become the company’s second-largest revenue segment, trailing only its transit fuel cell division. This repeat order confirms sustainable, replicable growth in the overseas off-grid power segment. A new industry trend has emerged: automotive fuel cell modules are downward-compatible with stationary power applications, enabling manufacturers to amortize production costs across shared assembly lines and unlock profit upside.

Parallel demand is emerging for AI computing backup power. Global tech giants are ramping up investments in hydrogen backup power. Microsoft and Amazon continue to deploy megawatt-scale fuel cell setups for data center power supply. Boasting millisecond load switching capability and zero carbon emissions, hydrogen has become the prime alternative to diesel gensets for AI computing campuses, creating dual demand alongside Europe’s construction and tourism sectors.

(II) UK Launches SAF Policy Consultation; Long-Term Green Hydrogen Demand via PtL Jet Fuel Secured, Yet Severe Short-Term Capacity Gaps Persist

Over the past two weeks, the UK Department for Transport (DFT) officially launched a public consultation on its mandatory sustainable aviation fuel (SAF) blending mandate, focusing on industry-wide capacity assessments for hydrogen-based power-to-liquid (PtL) fuels. The initiative signals two pivotal industry shifts:

Mandatory policy locks in long-term green hydrogen demand. The UK’s SAF blending rules will take effect by end-2026, requiring 0.2% of jet fuel to come from green hydrogen-derived PtL feedstocks by 2028, rising to 3.5% by 2040. Meanwhile, caps will be imposed on waste oil-based HEFA fuel usage, forcing jet fuel producers to comply with regulations via green hydrogen paired with captured CO₂ to synthesize PtL fuels. This opens vast long-term upside for green hydrogen, with the industry widely viewing mandatory PtL blending as a core permanent growth driver for hydrogen demand.

Near-term industrial bottlenecks trigger a transitional industry adjustment phase. The UK currently hosts no commercial-scale PtL jet fuel production facilities. Projects face compounded headwinds including constrained renewable power supply, elevated green hydrogen costs, limited carbon capture feedstock sources, and financing hurdles. Industry stakeholders report production timelines for advanced non-HEFA fuels lag policy targets, prompting government concerns that supply shortages will fail to meet blending obligations. The consultation will evaluate potential adjustments to HEFA volume caps and compliance frameworks. The DFT will consolidate industry feedback in autumn 2026; any policy tweaks could slow near-term investment in PtL projects, though the long-term growth thesis for green hydrogen aviation remains intact.

II. Domestic China Market: Top-Tier Policy Catalysts Land, Commercialization Accelerates Across Segments, Cost Disadvantages Remain a Key Hurdle

(I) Top-Down Policies Unlock New Incentives; Comprehensive Hydrogen Pilots Unleash Full Industrial Chain Potential

At the start of June, three central ministries jointly issued a circular on comprehensive hydrogen application pilots, spurring intense industry discussion over policy implementation details in the subsequent two weeks.

Pilots span the entire industrial chain with amplified financial support. The central government has selected urban agglomerations to carry out four-year demonstration programs, with maximum funding awards of RMB 1.6 billion per cluster. Supported use cases extend beyond traditional fuel cell vehicles to green hydrogen chemical production, hydrogen metallurgy, hydrogen-blended power generation, off-grid energy storage, and hydrogen-powered vessels. Two landmark 2030 targets have been formalized: a national fleet of 100,000 fuel cell vehicles and a retail hydrogen price of RMB 25 per kg for transport, with leading regions targeting RMB 15 per kg, laying out clear long-term scale and cost roadmaps for the sector.

Leading industry experts align on the sector’s development cycle. During FCVC 2026 (June 10–12), Academician Ouyang Minggao stated the hydrogen industry has crossed the “valley of death,” identifying the next five years as a critical window for large-scale commercialization. Wan Gang, former vice chairman of the China Association for Science and Technology, called for accelerated development of wind-solar coupled green hydrogen and cross-regional hydrogen transportation corridors. Aligned policy and industrial consensus have boosted long-term sentiment among primary market investors and A-share hydrogen stock participants.

(II) Segmented Commercialization Gains Traction: Industrial Green Hydrogen, Commercial Vehicles, and Domestic Equipment Exports All Deliver Growth

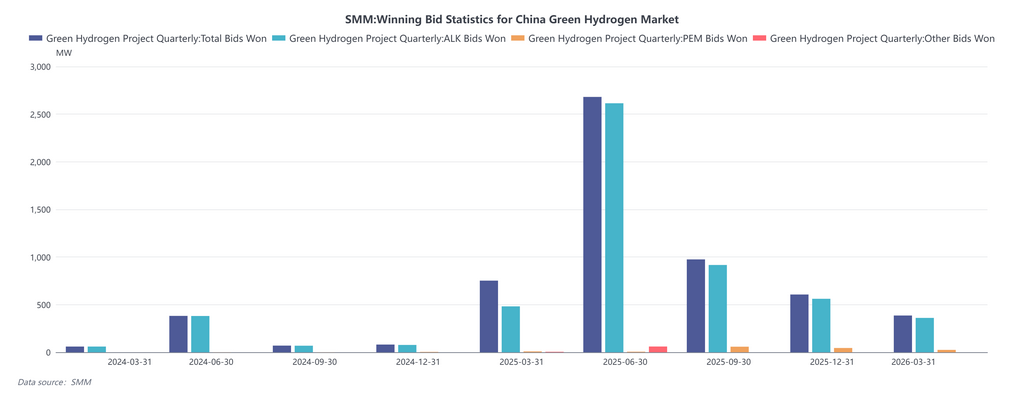

Accelerated large-scale green hydrogen deployment in heavy industry. Ningxia Baofeng’s RMB 13.5 billion green hydrogen-coal chemical integration project has entered commissioning, delivering an annual green hydrogen output of 150,000 tons at production costs below RMB 18 per kg, setting a domestic benchmark for low-cost green hydrogen. Baosteel Zhanjiang’s million-ton hydrogen metallurgy production line has achieved full operational capacity, deploying domestically manufactured hydrogen shaft furnace technology to replace imported equipment. Massive industrial hydrogen consumption is driving upstream demand for electrolyzers. As of end-March, China’s installed renewable hydrogen production capacity exceeded 250,000 tons per annum, doubling from end-2024 levels.

Scaling penetration of fuel cell commercial vehicles and two-wheelers. Regional hydrogen price data updated June 1 shows retail hydrogen prices of RMB 29–38 per kg across major domestic markets, still above the RMB 25 per kg national target. Nevertheless, 49-ton hydrogen heavy-duty trucks have cut hydrogen consumption to 8.5 kg per 100 km, undercutting diesel trucks in operating costs on select trunk haul routes. Hydrogen two-wheeler pilots are expanding rapidly, with tens of thousands of hydrogen light vehicles deployed in Chengdu, Changzhou, and Huangshi. Fast refueling and stable low-temperature driving range have unlocked new civilian niche demand.

Rapid overseas expansion of domestic hydrogen equipment. At the Brazil International Hydrogen Exhibition (June 16–17), a delegation from the Daxing Hydrogen Demonstration Zone in Beijing showcased Chinese electrolyzers and hydrogen heavy-duty trucks to tap Latin American demand. Overseas demand for off-grid power and zero-emission mine power aligns with Ballard’s international order momentum, lifting export growth expectations for domestic fuel cell system and electrolyzer manufacturers.

(III) Core Domestic Market Constraint: Elevated End-User Hydrogen Costs Impede Full-Scale Commercialization

The latest China Hydrogen Price Index shows clean hydrogen priced at RMB 34.34 per kg in the Yangtze River Delta, RMB 38.13 per kg in the Pearl River Delta, and industrial hydrogen at RMB 29.33 per kg in Henan. Only wind- and solar-rich chemical parks in western China have achieved the RMB 18 per kg low-cost green hydrogen threshold. High costs tied to hydrogen storage and refueling infrastructure allocation erode economic viability for transportation and distributed power applications. For the near term, industry growth will remain concentrated in large-scale industrial hydrogen consumption and policy-subsidized pilot projects.

Conclusion

Near-term market catalysts stem from overseas power generation equipment orders, domestic pilot policy rollouts, and surging equipment exports. Over the long run, off-grid hydrogen power and green hydrogen aviation will emerge as the sector’s core high-growth tracks. The industry, however, continues to face headwinds including capacity constraints, prohibitive production costs, and project financing challenges.