SMM News, March 20

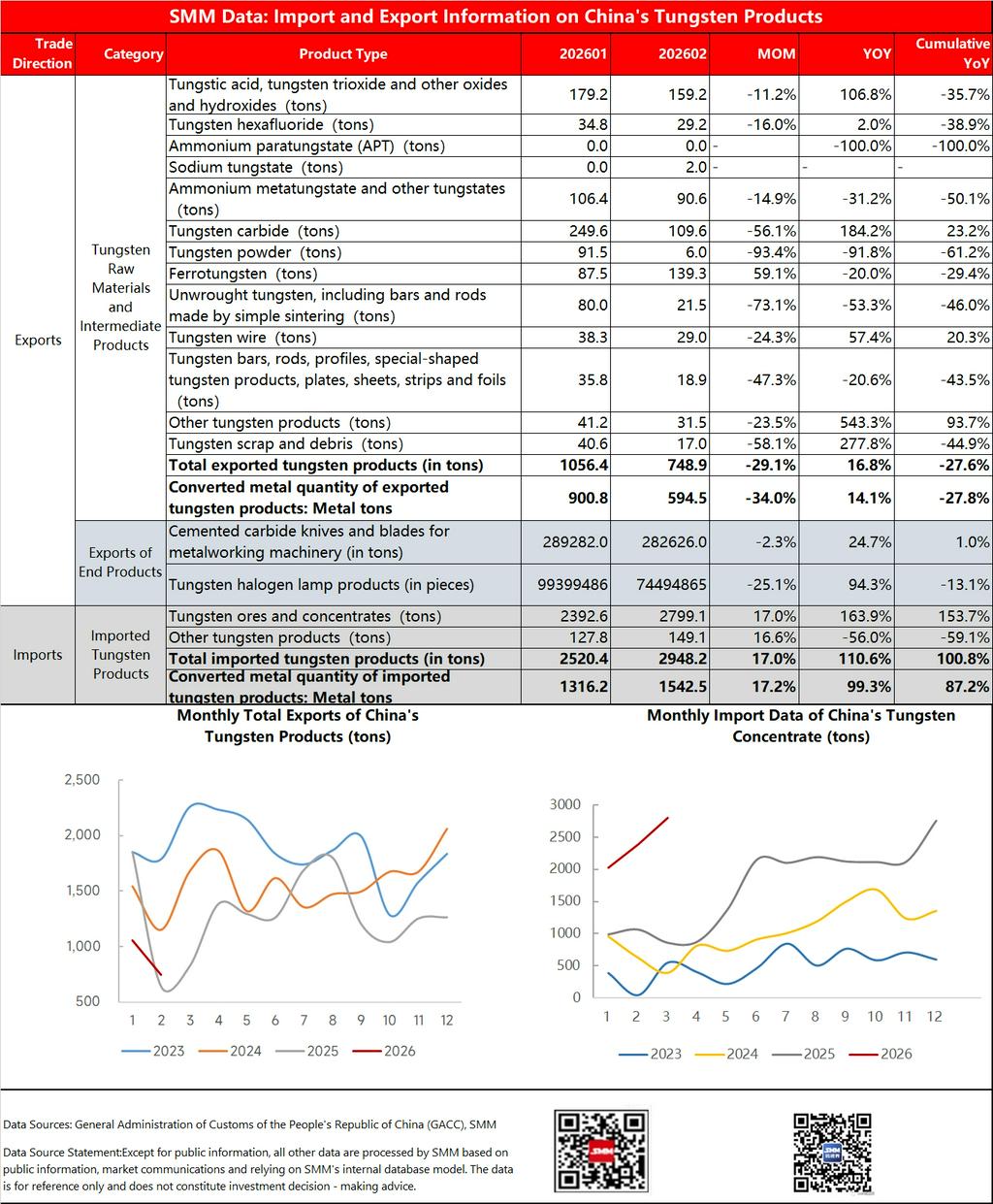

According to customs data, China’s total exports of tungsten smelting products and tungsten materials reached approximately 1,805.3 tonnes in January–February 2026, down 27.6% year on year. Total imports of tungsten concentrate stood at around 5,195.7 tonnes over the same period, surging 153.7% year on year, with the combined volume of imported tungsten products totaling about 5,468.6 tonnes, up 100.8% year on year.

In terms of tungsten metal content, China imported approximately 2,858.7 metric tons of tungsten metal in January–February, an increase of 87.2% year on year, while exporting 1,495.3 metric tons of tungsten metal, down 27.8% year on year. In terms of trade structure, China recorded a net import of 1,363 metric tons of tungsten metal in January–February 2026, compared with a net export of 545 metric tons in the same period last year.

Since export controls were implemented in February 2025, exports of some domestic tungsten smelting products and tungsten materials have trended downward. Amid tightening domestic tungsten ore supply, demand for imported overseas ore resources has risen markedly.

Export Structure Diverges: Raw Materials Contract Sharply, End Products Remain Resilient

Affected by tightened export policies and production halts during the Spring Festival lull, exports of tungsten raw materials and intermediate products saw a steep decline:

- China’s exports of ammonium paratungstate (APT) dropped to zero in January–February.

- Exports of other dual-use items also fell notably, with tungsten powder exports plunging 61.2% year on year.

According to export enterprises, the approval process for dual-use tungsten items is lengthy. Most overseas quotations from enterprises adopt a provisional pricing model, with final prices adjusted based on market prices at the time of actual shipment.

Furthermore, the rapid rally in global tungsten market prices at the end of 2025 led to volatile price gaps between domestic and overseas markets, making it difficult for importers and exporters to lock in profits. Heightened risk aversion among enterprises has resulted in weakened export orders.

On January 6, 2026, the Ministry of Commerce issued an announcement on export controls to Japan, prohibiting the export of dual-use tungsten items to Japanese military-related end-users and for military applications. This policy has also affected exports of certain products to Japan.

Customs data shows that China’s exports of tungsten products and intermediates (excluding cemented carbide) to Japan totaled 303 tonnes in January–February, down 36% year on year, accounting for 16.8% of total national exports. By product, exports of controlled items such as tungsten carbide and tungsten powder to Japan fell to zero in February, while ferrotungsten exports to Japan saw a slight increase. Total exports of tungsten products to Japan are expected to maintain a downward trend going forward.

By destination, South Korea, Japan, and Europe were the main export markets for China’s tungsten products in January–February 2026. Exports to South Korea reached 481 tonnes, surging 165% year on year and accounting for 26.7% of total exports. South Korea overtook Japan to become China’s largest export market for tungsten products. Meanwhile, exports of tungsten intermediates and products to Vietnam, Thailand, and the UK rose by 108%, 133%, and 157% year on year, respectively.

Import Market: Imports Surge, Reliance on Overseas Tungsten Ore Rises

Tungsten Ore & Concentrate

Domestic tungsten prices rose sharply in January–February 2026, prompting ore importers to increase shipments to the Chinese market and driving a substantial jump in tungsten concentrate imports.

Major sources of China’s tungsten concentrate imports included Kazakhstan, Myanmar, and Mongolia. On a year-on-year basis, imports from Vietnam, Rwanda, Nigeria, Bolivia, and Australia grew notably. In particular, tungsten concentrate imports from Vietnam reached approximately 376 tonnes in January–February, accounting for around 7.3% of total imports and soaring 1,092% year on year.

Cemented Carbide Tools for Metalworking Machinery

In January–February 2026:

- China exported 572 tonnes of cemented carbide tools for metalworking machinery, up 1% year on year.

- Imports amounted to 226 tonnes, rising 27.6% year on year.

- Net exports stood at 346 tonnes, down 11.1% year on year.

The decline in exports of domestic cemented carbide tools was driven by several factors:

- Production cuts and logistics disruptions during the Spring Festival holiday, combined with a seasonal lull in procurement in major markets such as Europe and the US, suppressed short-term export deliveries and order volumes.

- Export controls on upstream tungsten raw materials led to temporary tightness in domestic feedstock supply; enterprises prioritized domestic production capacity, restricting export scheduling.

- Weak downstream demand in global machine tool and machining sectors, coupled with intensified regional competition, further weighed on export performance.

While high value-added cutting tools remain resilient over the long term, they face short-term pressure.

Outlook

In the short term, domestic tungsten raw material supply is tightening and import dependence is increasing, maintaining a net import pattern for tungsten ore and other raw materials.

In March, overseas tungsten prices rallied sharply, pushing up export prices of tungsten ore from South America, Africa, and other regions significantly. Lower import margins may reduce future import volumes to China. Meanwhile, stricter customs inspections on imported tungsten ore in some regions are also expected to curb import growth.

On the export side, no relaxation of China’s tungsten export control policies is anticipated in the near term, so exports of tungsten products and intermediates are unlikely to expand substantially. However, the export mix will continue to shift toward non-dual-use items and high value-added products.

Over the medium to long term, export policies will continue to guide the industrial chain toward higher value added and technological advancement, raising the share of end-product exports. Strong growth in tungsten concentrate imports may become the norm. China will need to strengthen resource exploration and recycled tungsten recovery to safeguard industrial chain security.