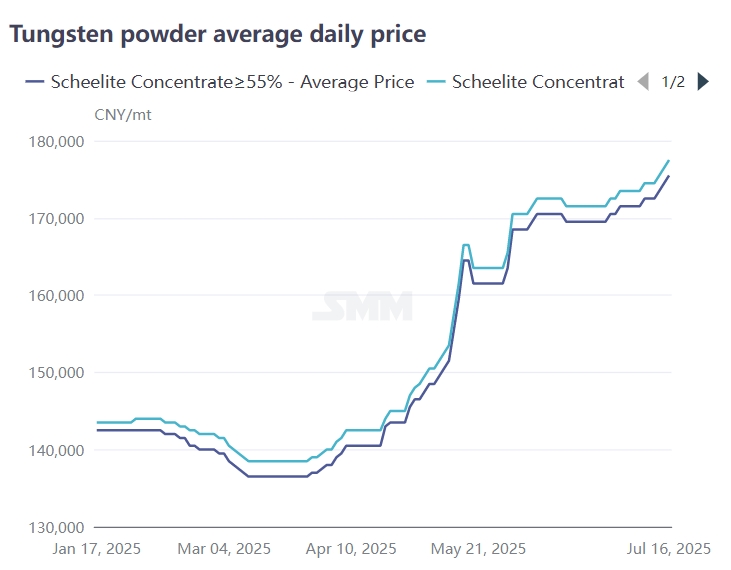

SMM News on July 16:

Since the start of July, the tungsten market has once again been driven by tight supply at the ore end, with prices climbing upward. The circulation of tungsten concentrate in the market is relatively tight, making it difficult for downstream enterprises to replenish inventories. The transaction price of bulk orders has been rising steadily. As of today, the SMM price of 65% black tungsten concentrate is reported at 178,500 yuan per standard ton, an increase of about 25% compared with the beginning of the year; the price of 65% white tungsten concentrate is 177,500 yuan per standard ton, up 25.4% from the start of this year. Driven by the rapid rise in upstream ore prices, downstream tungsten products such as ammonium paratungstate and tungsten powder have also entered an upward channel. As of today, the SMM price of ammonium paratungstate is 261,000 yuan per ton, a 24% increase from the beginning of the year; the price of tungsten carbide powder is 376.5 yuan per kilogram, up 23.3% from the start of the year. The tungsten market has started a high-price transmission from upstream to downstream.

Long-term order aspect:

In the first ten days of July, the long-term orders of major domestic tungsten enterprises for the first half of July showed an upward trend. Among them, the ore end price was increased by 1,000-2,500 yuan per standard ton compared with the second half of June. The increase in the long-term order purchase price of ore by major tungsten enterprises to some extent reflects the tightness of tungsten ore, driving up the market's bullish sentiment.

Overseas tungsten market: The overseas tungsten market maintained an upward trend in July. After China imposed export controls on ammonium paratungstate and tungsten carbide in February this year, the circulation of overseas tungsten markets has been tight. As of today, European ferrotungsten is priced at 52-52.6 US dollars per kilogram of tungsten (equivalent to 260,700-263,000 yuan per metric ton); European APT is 460-485 US dollars per ton unit, equivalent to 291,500-307,400 yuan per ton, showing a large price difference with the domestic market.

Tungsten ore supply side:

The newly revised "Mineral Resources Law of the People's Republic of China" came into effect on July 1 this year. The new law lists tungsten as a strategic mineral resource and implements a protective mining system. In addition, the new law requires mining right holders to carry out ecological restoration of mining areas in accordance with the approved ecological restoration plan for mining areas, and clarifies that the costs for ecological restoration of mining areas by enterprises shall be included in production costs. This has increased the environmental protection costs of tungsten mining enterprises. Some small and medium-sized mines in Jiangxi, Hunan and other regions that fail to meet environmental protection standards or have excessively high transformation costs have suspended production or reduced output, raising concerns about market supply. The circulation of spot goods in the market has tightened, and downstream bullish sentiment has driven up the willingness to replenish inventories, leading to a rise in the transaction focus.

In addition, large tungsten enterprises mostly adopt an integrated model of mining-smelting-deep processing. These enterprises have relatively concentrated tungsten concentrate, but most of it is for self-use. Moreover, as tungsten ore resources become increasingly tight, large enterprises have increased their demand for external procurement, stimulating the rise in ore prices.

Downstream demand: In July, traditional manufacturing industries such as domestic infrastructure, mechanical processing, and metal cutting generally entered the off-season. Coupled with the suppression of high prices in the tungsten raw material market, the demand for tungsten products in these industries has declined. Some cemented carbide enterprises reported that orders for tungsten products in the fields of CNC blades, milling machine tools, and electronic manufacturing have decreased by about 10%-20% month-on-month.

Demand in the military industry is promising. Tungsten, with its excellent properties, plays an important role in military equipment and is widely used in ammunition preparation, weapons and equipment, aerospace components, tungsten steel armor, etc. According to the 2025 central and local fiscal budget draft report, China's national defense expenditure in 2025 will be 1.784665 trillion yuan, an increase of 7.2%. This marks the third consecutive year that China's defense expenditure has maintained a 7.2% growth rate. According to the report released by the Stockholm International Peace Research Institute (SIPRI) on April 28, 2025, global military expenditure reached 2.72 trillion US dollars in 2024, an increase of 9.4% compared with 2023, the largest year-on-year increase since the end of the Cold War. The growing demand in the military industry is beneficial to the demand for tungsten.

In the short term, the main driving factors for this round of rising tungsten market are still the restrictions on mining quotas, tight supply at the upstream ore end, and rigid demand in emerging fields such as the military industry. At present, the prices of upstream products such as tungsten concentrate are consolidating at a high level, while the inversion range in the downstream ammonium paratungstate and powder sectors is expanding. Without significant growth in terminal demand, the prices of these intermediate tungsten products are difficult to rise rapidly. If there is a reduction in production in the downstream powder sector, it will also curb the upward momentum of upstream raw materials. In the short term, the upstream and downstream of the tungsten market are in a game, and the market will mainly consolidate at a high level.

In the medium and long term, the tungsten market may be constrained by the problem of tight ore resources for a long time. This will mean that some downstream processing enterprises without ore resources will bear high raw material costs for a long time, leading to the flow of industry orders to leading enterprises, and the industrial concentration may show an increasing trend. In addition, the slow growth in traditional demand areas has also forced the industry to switch to orders in emerging fields and the military industry.