SMM News: September 10, Japan's famous business weekly magazine "Toyo economy" released an album article "China and Japan 50 areas of enterprise strength thoroughly showdown", made a comparison between China and Japan in 50 areas. In the end, China won 28, Japan 21, and a draw. Surprisingly, in this list, both manufacturing powers, as the world's largest steel country is inferior to Japan in terms of comprehensive competitiveness, and the transformation of Chinese steel companies is still in progress.

Key words: industrial transformation and upgrading; merger and reorganization; industrial concentration; trade war

There are many similarities in the background of transformation and upgrading of iron and steel industry between China and Japan.

In the macro environment, the economic growth rate has slowed down obviously, the growth center has become a consensus, the demographic dividend has an inflection point, the comparative cost advantage of labor force has gradually disappeared, the foreign trade is under pressure from the United States, and exports are under great pressure. The government has taken the initiative to implement the industrial adjustment policy to promote the adjustment and upgrading of the industrial structure. The industry itself has also entered the production capacity stage, steel prices rose to improve the operating conditions of enterprises.

1. It has become a consensus that the economic growth has slowed down and the growth center has moved downward.

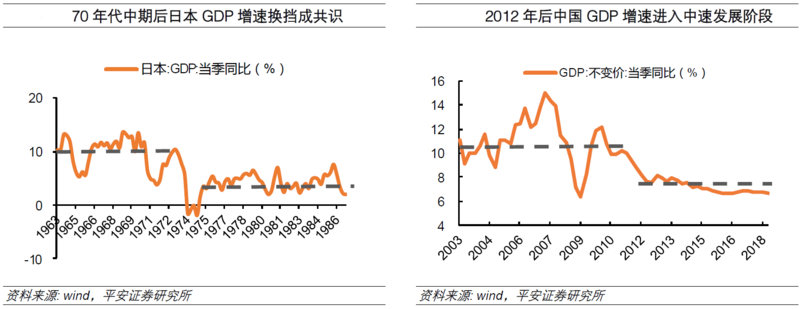

After the Izano boom in 1973, Japan became the third largest economy after the United States and the former Soviet Union. Subsequently, the Japanese economy experienced a sharp decline in economic growth over the past few years, and entered a period of medium-and low-speed stable growth, and it has become a consensus that the economy has grown at a medium-and low-speed rate. The "Pingcheng boom", which began at the end of 1986, appeared in such a context. Similarly, after 2012, China's GDP growth rate has entered a medium-speed development stage, domestic economic development has gradually entered a "new normal", and the downward shift of the economic growth center has become a social consensus.

2. Under the pressure of US trade, foreign trade and exports are under great pressure.

Since the 1950s, the trade friction between the United States and Japan has been continuous, at first mainly concentrated in the textile field, to the 1960s, the field of trade friction gradually expanded to the iron and steel industry and other manufacturing fields. On May 25, 1989, the Bush administration listed Japan as one of the three major countries engaged in unfair trade, and the trade conflict between the two countries reached its peak. Under pressure from the United States, Japan took the initiative to appreciate the yen after the Plaza Agreement, leading to a reversal of the trend of sustained high growth in its trade surplus.

Since China's accession to the WTO in 2001, the total amount of Sino-US trade and the amount of Sino-US trade frictions have been on the rise. In particular, when a trade war broke out between China and the United States in 2018, the two sides imposed high import tariffs on each other to push the issue of trade friction between China and the United States to a climax. In this context, China's foreign trade exports are facing great pressure.

There are great differences in the development of iron and steel industry between China and Japan.

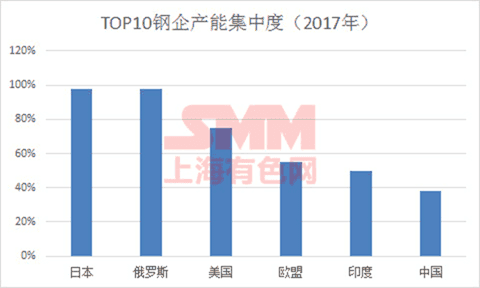

In the incremental space of iron and steel industry, China is obviously higher than Japan, the dependence of China's iron and steel industry on overseas markets is much lower than that of Japan, and the structure of iron and steel products in China is dominated by construction materials, while Japan is dominated by manufacturing materials. In the face of the trade pressure of the United States, the yen chooses to appreciate, while the RMB is relatively in the channel of devaluation, which has different effects on iron and steel exports. In terms of industrial concentration, the average CR4 of Japanese iron and steel industry is 60%, but China is far from each other. In the same period, Japan has played a leading role in the development of metallurgical technology in the world, but China is still catching up.

1. China still has the absolute advantage in crude steel output, but the innovation ability is insufficient.

The output of crude steel in China is 50% of that in the world and eight times that in Japan. Japan's Ministry of economy, Trade and Industry expects Japan's crude steel production to benefit from strong demand from the domestic automotive, industrial and construction machinery industries in the fourth quarter, and is expected to achieve year-on-year growth. Japan's Ministry of economy, Trade and Industry predicted that Japan's crude steel production would rise to 26.45 million tons in the fourth quarter, up 0.2 percent from a year earlier, while production fell slightly in the third quarter from a year earlier. In terms of crude steel production, Japan also faces pursuit from India, which is overtaking Japan as the second largest crude steel producer, according to the latest statistics.

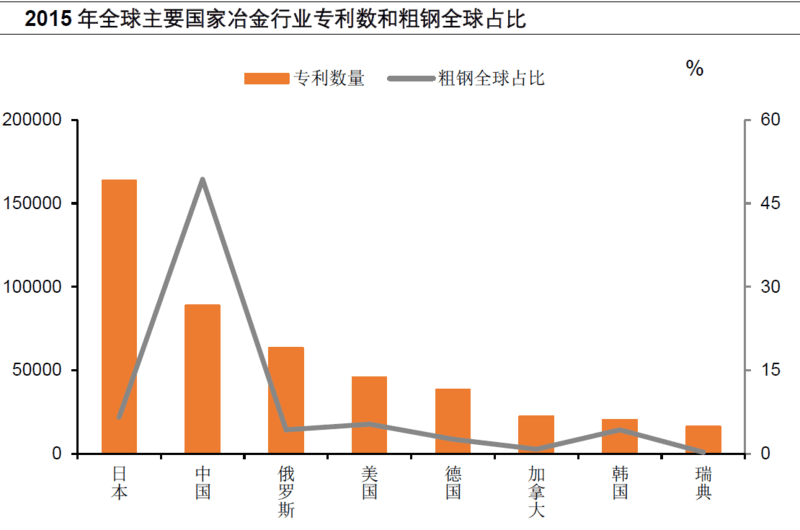

It's not the same in terms of scale. However, Japan is ahead in the technology of advanced steel. Because Japanese steel companies and automobile manufacturers cooperate very well, they can design and manufacture advanced steel according to the needs of users. This is not as long as there is advanced equipment to have advanced technology. In comparison, at present, the output scale of crude steel in China is leading in the world, and the most advanced equipment in the world has been introduced, but the innovative ability represented by the original technical invention and equipment is not outstanding. It does not match its own size and industry transformation and upgrading requirements. Taking the patent invention data as an example, the number of patents in China's iron and steel industry in 2015 was only 54% of that in Japan, which did not reach the ability to lead the world metallurgical industry.

2. Different domestic demand structure leads to great difference in product structure

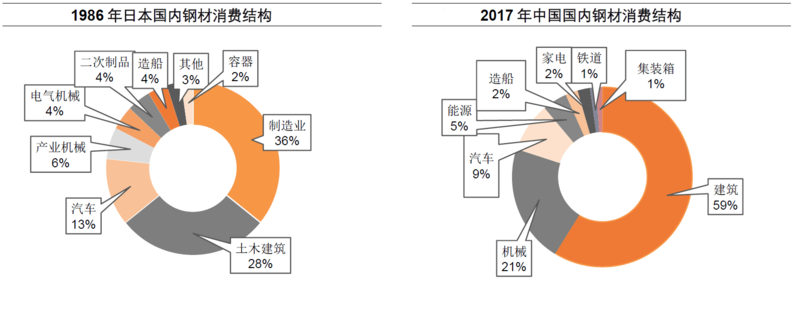

There are great differences in steel demand structure between China and Japan, which leads to great differences in steel product structure. In 1986, manufacturing accounted for the highest 36% of Japan's steel consumption structure. In 2017, China's steel consumption was the most dependent on the construction industry, reaching 59%. The difference in the structure of downstream demand also leads to the difference in the structure of steel products: flat wood was mainly used in Japan during the Pingcheng boom period. In 1990, the proportion of flat wood in Japan reached 56%, while that of long wood was only 30%. In 2017, the proportion of long steel products in China's steel product structure was as high as 44%, while that of flat steel products was only 39%.

The high dependence of China's steel consumption on the construction industry also reflects that not only the Chinese economy, but also the high dependence of China's steel industry on real estate has had a negative impact on the development of the industry. The continuous rise in real estate prices and the rising proportion of real estate in GDP have a negative impact on the macroeconomic structure: in recent years, the growth of China's manufacturing industry has continued to decline. Real estate growth continues to rise, real estate prices are too high to increase the cost of the downstream real economy, due to the attraction of high real estate prices, a large number of funds have entered the real estate market, the capital chain is tight, and residents' consumption is tightened. At the same time, real estate has the attribute of financial collateral, mortgage risk increases systemic risk. At present, the estimated construction cost is less than expected, indicating the long-term abnormal development of the real estate industry chain, a large number of funds are used for land purchase, in fact, the joint income obtained by the tourism manufacturing industry continues to decline.

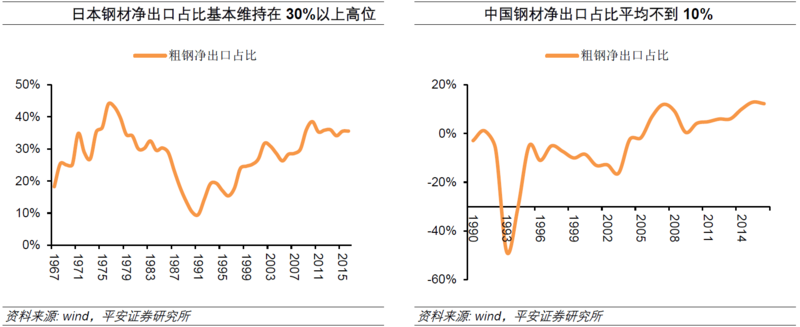

3. There are differences in the degree of dependence of the steel industry between China and Japan on overseas markets.

Japan's domestic market is narrow and its consumption capacity is insufficient, so foreign demand accounts for a large proportion of the demand of Japan's iron and steel industry and has a high degree of dependence on overseas markets. However, China's domestic market is huge, and the regional economic development is uneven, domestic demand occupies the main position of iron and steel consumption, the overseas market is only as a supplement to the domestic market, and the degree of dependence on the overseas market is low.

What is the reference for the development of China's iron and steel industry from the road of transformation and upgrading of Japanese iron and steel industry?

Japan's iron and steel industry has mainly adopted the following measures to promote industrial transformation and upgrading: to adapt to the trend of domestic industrial structure adjustment, to actively carry out product structure adjustment and technological upgrading, to transfer production capacity to overseas investment, and to improve the pattern of domestic supply and demand. The industry actively promotes capacity removal to improve capacity utilization; the government actively expands domestic demand, industry transformation and upgrading get help.

1. Industry merger and reorganization is expected to accelerate

From the experience of transformation and upgrading in Japan, a higher degree of industry concentration can make better use of limited production and pressure storage, technological innovation and market voice to maintain higher product prices and profits. Over the past two decades, the concentration of China's iron and steel industry has always been at a relatively low level, leading to major issues such as the ability to control resources, orderly market competition, elimination of backward production capacity, technological R & D and innovation, energy conservation, consumption reduction, emission reduction, and so on. Lack of effective industry binding force and self-discipline ability, competitive price reduction among enterprises, market prices ups and downs. Improving the degree of industrial concentration has become a strategic measure to enhance the international competitiveness of China's iron and steel industry, save social costs and optimize the allocation of resources.

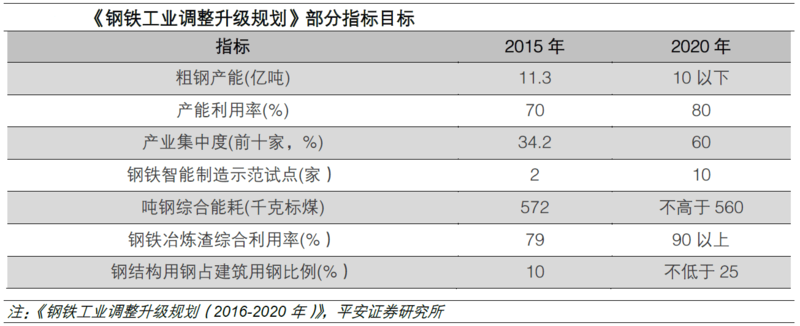

According to the 13th five-year Plan issued by the Ministry of Industry and Information Technology, the concentration of the top 10 key steel enterprises has increased to 60 percent from the current 34.2 percent, an increase of more than 25 percentage points. With the completion of the merger of Baosteel WISCO, the merger of local iron and steel state-owned enterprises will become possible; in the future, if the industry concentration is further concentrated, the leading enterprises will receive the excess benefits brought by supply centralization.

M & A fund in iron and steel industry has gradually become the main body of marketization and capitalization of iron and steel industry integration. Relying on iron and steel and the integration and expansion of upstream and downstream industrial chain, iron and steel fund plays a more and more important role in the M & A of iron and steel industry, which will accelerate the upgrading of national iron and steel industry concentration and the optimization and upgrading of the whole industry.

Hebei Province, as a major steel production province in China, the integration planning of the iron and steel industry is relatively clear. As early as 2016, the 13th five-year Plan for Industrial Transformation and upgrading in Hebei Province pointed out that we should speed up the joint restructuring and relocation of enterprises. By 2020, the "2310" industrial pattern will be formed, led by two major groups of Hegang and Shougang, supported by three local iron and steel groups of Qian'an, Fengnan and Wu'an, and supplemented by 10 characteristic iron and steel enterprises, so as to realize the transformation from a major iron and steel province to a strong iron and steel province. In 2018, the work Plan for the removal of production capacity in the Iron and Steel Industry in Hebei Province (2018-2020) pointed out that by 2020, the number of iron and steel smelting enterprises in Hebei Province will be reduced to about 60, and the production capacity of the top 15 enterprises will account for more than 90% of the total capacity of the province. Among them, Tangshan City plans to integrate the city's iron and steel enterprises to less than 30 by 2020 and to about 25 by 2025. Wu'an City plans to integrate and reorganize 14 iron and steel enterprises into 5 to 6 iron and steel enterprise groups by 2020. Handan will focus on promoting the integration and reorganization of four iron and steel enterprises: Baoxin Iron and Steel Co., Ltd., Jinan Iron and Steel Co., Ltd., Taihang Iron and Steel Co., Ltd., and Yongyang Special Steel Company.

The iron and steel industry in Jiangsu Province actively promotes the "134th" pattern, that is, a super-large iron and steel enterprise group with Shagang as the first echelon (50 million tons); Three super-large iron and steel enterprise groups with Zhongtian, coastal and Xuzhou as the second echelon (more than 20 million tons), and four characteristic iron and steel enterprise groups with Nanjing Iron and Steel, Xingcheng, Tiangong and Delong as the third echelon. The first four iron and steel enterprises strive for more than 80 percent of the province's crude steel production capacity, and the top eight strive to reach 100 percent of the province's crude steel production capacity. Anyang City, Henan Province plans to integrate the number of iron and steel enterprises from 11 to 4 by 2020, forming a fully functional group of raw material protection, smelting, rolling and intensive processing industries.

In the era of "post-capacity removal", the key development task of the iron and steel industry has been transformed into deleveraging and merger and reorganization. With the help of the relevant iron and steel industry integration funds and the implementation of regional integration plans, the leading enterprises in the iron and steel industry will further enhance their ability to integrate high-quality production capacity and accelerate mergers and restructurings. We will raise the high-quality development of the iron and steel industry to a new level.

2. Supply side: supply side reform continues for 19 years is expected to continue to reduce production capacity

In 1978, the Ministry of Trade and Industry of Japan formulated and promulgated the interim measures for the Stability of specific depressed Industries (referred to as the Special Security Act), which explicitly designated the flat electric furnace steelmaking industry as a structural depression industry. The depressed industries are required to listen to the views of the review committee, announce the basic plan for stabilization, and take the initiative to follow the basic plan for stabilization to phase out production capacity and equipment. In 1983, the Ministry of Trade, Trade and Industry of Japan further promulgated the interim measures Act on the improvement of specific Industrial structure (referred to as the "property structure Law") as an alternative to the Special Security Act. The "production structure Law" roughly continues the main contents of the "Special Security Law", retains the open-hearth furnace and electric furnace steel manufacturing industry as a designated industry, and continues to require the elimination of backward production capacity equipment, and at the same time, it has also added the content of promoting the adjustment of the industrial structure.

In order to adapt to the new form of industrial development, on May 8, 2015, the State Council officially issued "made in China 2025" to comprehensively promote the implementation of the manufacturing power strategy. In order to promote the development of the iron and steel industry, on February 4, 2016, the State Council issued the "opinions of the State Council on resolving excess capacity and realizing the Development of extrication from difficulties in the Iron and Steel Industry" (Guofa [2016] No. 6). It is clearly pointed out that it is necessary to "reduce the crude steel production capacity by 100-150 million tons in five years" and "establish a long-term mechanism for market-oriented adjustment of production capacity, so as to optimize the structure of the iron and steel industry, extricate itself from difficulties and upgrade, and improve quality and efficiency." On November 14, 2016, the Ministry of Industry and Information Technology officially issued the Iron and Steel Industry Adjustment and upgrading Plan (2016-2020), which clearly defined the adjustment and upgrading objectives of the iron and steel industry during the 13th five-year Plan period.

It is expected to continue to reduce production capacity in 19 years. The target of eliminating production capacity in the iron and steel industry in 2018 is 30 million tons. From January to July, it has completed the reduction of crude steel production capacity of 24.7 million tons, more than 80 per cent of the annual task of 30 million tons, and is expected to complete the pressure and energy reduction task within the year in accordance with the planned target. Although there is no clear target for 19 years of capacity removal, but the peak steel demand has passed, the steel industry still faces the problem of relative overcapacity, 19 years is expected to continue to reduce steel capacity.

Enlightenment from the Transformation and upgrading of Japanese Iron and Steel Industry

At a time when China is cutting excess capacity, Chinese companies that have survived the capacity cuts will be stronger, will move towards higher-grade steel over time, and Japan will not always lead in technology under the effect of scale. According to the chairman of Nippon Steel, "I can feel the breathing of Chinese companies behind me." Throughout the history of transformation and upgrading of Japanese iron and steel industry, it can bring the following enlightenment to the transformation of China's iron and steel industry:

1. Continue to promote supply-side reform and capacity removal;

2. To further enhance the concentration of the industry and optimize the allocation of resources;

3. Grasp the strategic opportunity of "Belt and Road Initiative" and speed up the global layout of iron and steel production capacity;

4. Changing the mode of development to realize low-carbon green manufacturing and sustainable development;

5. Make great efforts to develop intelligent manufacturing technology and realize the breakthrough of scientific and technological innovation.