SMM, MAY 31 –

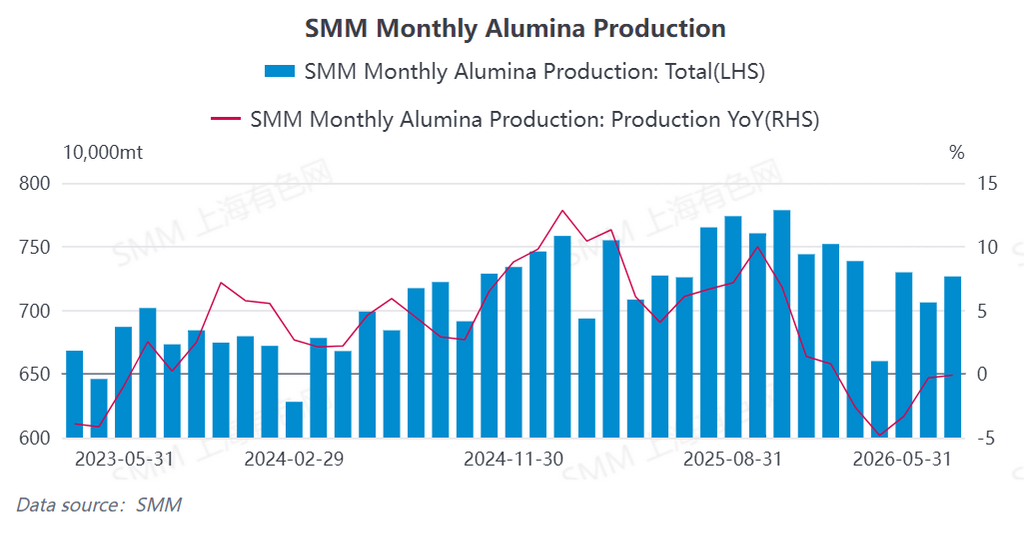

In May 2026, China's metallurgical-grade alumina production increased by 2.8% month-on-month, while edging down 0.19% year-on-year. As of the end of May, the national installed capacity stood at approximately 116.42 million tons, with new capacity commissioning increasing slightly compared to April. However, due to the slow recovery of maintenance work in the Guangxi region, coupled with concentrated maintenance in northern China, overall operating capacity fell by 0.43% month-on-month and decreased by 0.09% year-on-year, failing to sustain high operating levels during the month.

In terms of production structure, average daily output in May declined from April levels. Specifically, in Shanxi and Henan provinces, output dropped due to minor maintenance and some plants yet to fully resume normal production lines. Meanwhile, a major alumina producer in northern China also initiated maintenance, further dragging down overall output in the north. In contrast, the southern region saw a recovery in production, supported by the release of new capacity. In addition, an alumina producer in Guizhou resumed operations, which helped offset the output decline in the north to some extent, preventing a sharp drop in national average daily output.

Looking ahead to June, the supply surplus in the alumina market is expected to intensify. The main driving factors include the continued recovery of capacity in Guangxi, the full release of Phase I of new capacity projects, and the gradual conclusion of maintenance work in northern China. On balance, operating capacity in June is expected to rise to approximately 87.6 million tons, further increasing supply pressure.