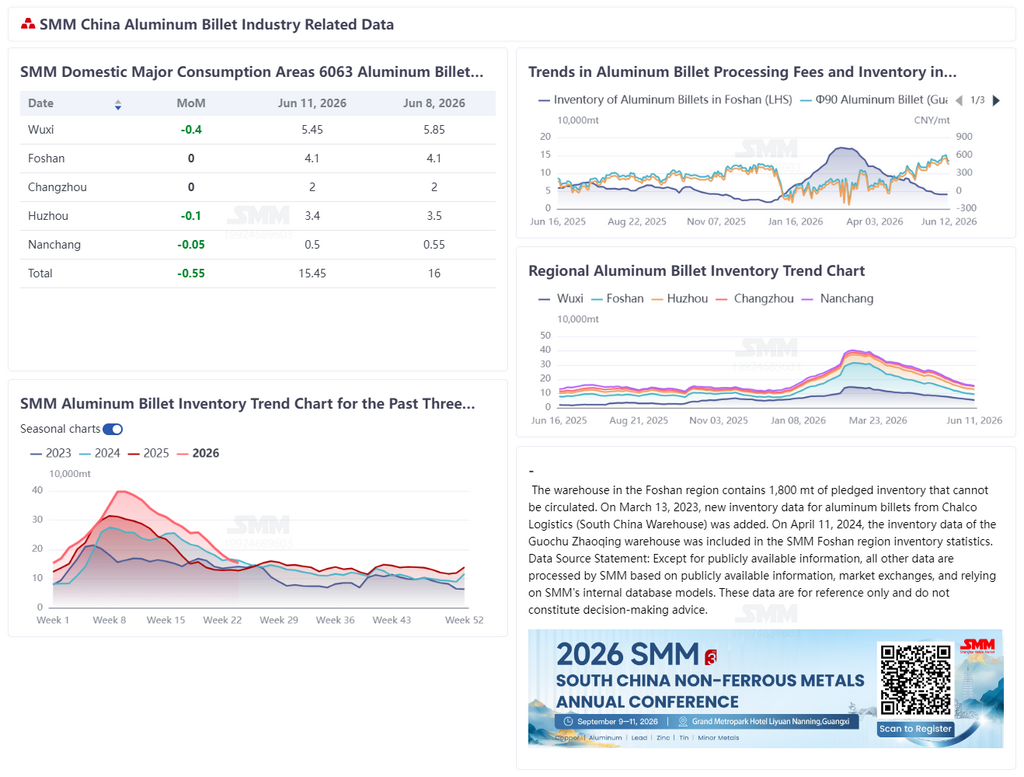

SMM, June 12:

According to SMM data, China's aluminum billet inventory in major consumption regions fell to 154,500 mt on June 11, down 8,000 mt from last Thursday and down 5,500 mt from Monday, with the destocking pace further slowing. From the perspective of warehouse withdrawals, aluminum billet withdrawals recorded 51,700 mt during June 1–8, down 4,100 mt WoW. Withdrawals fell for two consecutive weeks, and market trading sentiment turned cautious. Currently, aluminum billet inventory has fallen to around 150,000 mt, and the destocking speed has visibly slowed. On one hand, affected by elevated processing fees, downstream procurement sentiment was suppressed, and some producers considered starting their own furnaces to produce billets in-house as a substitute for external purchases—a substitution effect on the demand side that weakened rigid demand for aluminum billets. On the other hand, as processing fees continued to recover, producers gradually raised output, and warehouse inflows on the supply side showed a gradual recovery trend. Taken together, aluminum billet inventory is expected to fall further to below 150,000 mt next week, but the destocking speed will likely remain mild. Moving forward, attention should focus on the strength of downstream consumption recovery and the pace of incremental release on the supply side.

During the week, aluminum prices fluctuated after a rapid decline, and processing fees across regions showed a pattern of holding prices firm at high levels. By region, in Foshan, the φ90 aluminum billet processing fee was quoted at 520 yuan/mt and φ120 at 470 yuan/mt, unchanged from last week; in Wuxi, φ90 at 450 yuan/mt and φ120 at 350 yuan/mt, up 80 yuan/mt and 70 yuan/mt respectively from last week; in Nanchang, φ90 at 450 yuan/mt and φ120 at 400 yuan/mt, up 100 yuan/mt from last week. During the week, aluminum prices pulled back sharply, wait-and-see sentiment intensified downstream, and the procurement pace slowed. On the supply side, producers, burdened with high-cost raw materials from the previous period, had a willingness to hold prices firm. However, against the backdrop of slowing destocking speed and weakening marginal demand, upward support for processing fees weakened, resulting in an overall pattern of pulling back from high levels. Next week, aluminum billet processing fees are expected to move sideways within a range. Attention should be paid to the impact of aluminum price fluctuations on processing fees and social inventory destocking. If demand recovery falls short of expectations, processing fees have room to pull back further. The operating rate of aluminum extrusion fell 1.8 percentage points WoW to 55.8% this week, gradually revealing off-season characteristics. For construction extrusion, the recent periodic pullback in aluminum prices approached downstream psychological levels, stimulating some purchase demand release and providing a limited hedge against traditional off-season patterns. However, the persistently weak underlying trend in the property sector remained unchanged, and total aluminum usage in construction continued to face pressure. According to feedback from enterprises in south China, as deliveries of existing large-scale project orders wound down, new orders failed to fill the gap, prompting firms to cut production schedules and reduce raw material stockpiling. Signs of off-season weakness in construction extrusion became increasingly evident.

For industrial extrusion, structural differentiation persisted, but overall resilience outperformed the construction segment. Automotive aluminum extrusion still maintained a relatively high operating rate this week. NEV sales rebounded MoM in May, with mid- and low-end car model consumption volume providing strong support for rigid demand for aluminum extrusion, which can still sustain industry operations in the short term. However, some small and medium-sized enterprises reported that their current industrial extrusion orders on hand can only cover up to mid-June, with insufficient follow-up orders. If no new orders emerge in the latter half of the month, the operating rate will face downward pressure.

Overall, off-season pressure on construction extrusion materialized this week, dragging down the industry’s operating rate. While industrial extrusion still retains resilience, the issue of order gaps among small and medium-sized enterprises has surfaced, which will subsequently weigh on the segment’s overall performance. Under the combined pressure from these two fronts, the aluminum extrusion operating rate is expected to remain under pressure and pull back next week.

![After Peaking at 1.47 Million Mt, Accelerated Pullback—How Far Can China’s Aluminum Ingot Destocking Go? [SMM Analysis]](https://imgqn.smm.cn/production/admin/votes/imagesqsDLb20240416161800.jpeg)