SMM June 12 News:

Metals market:

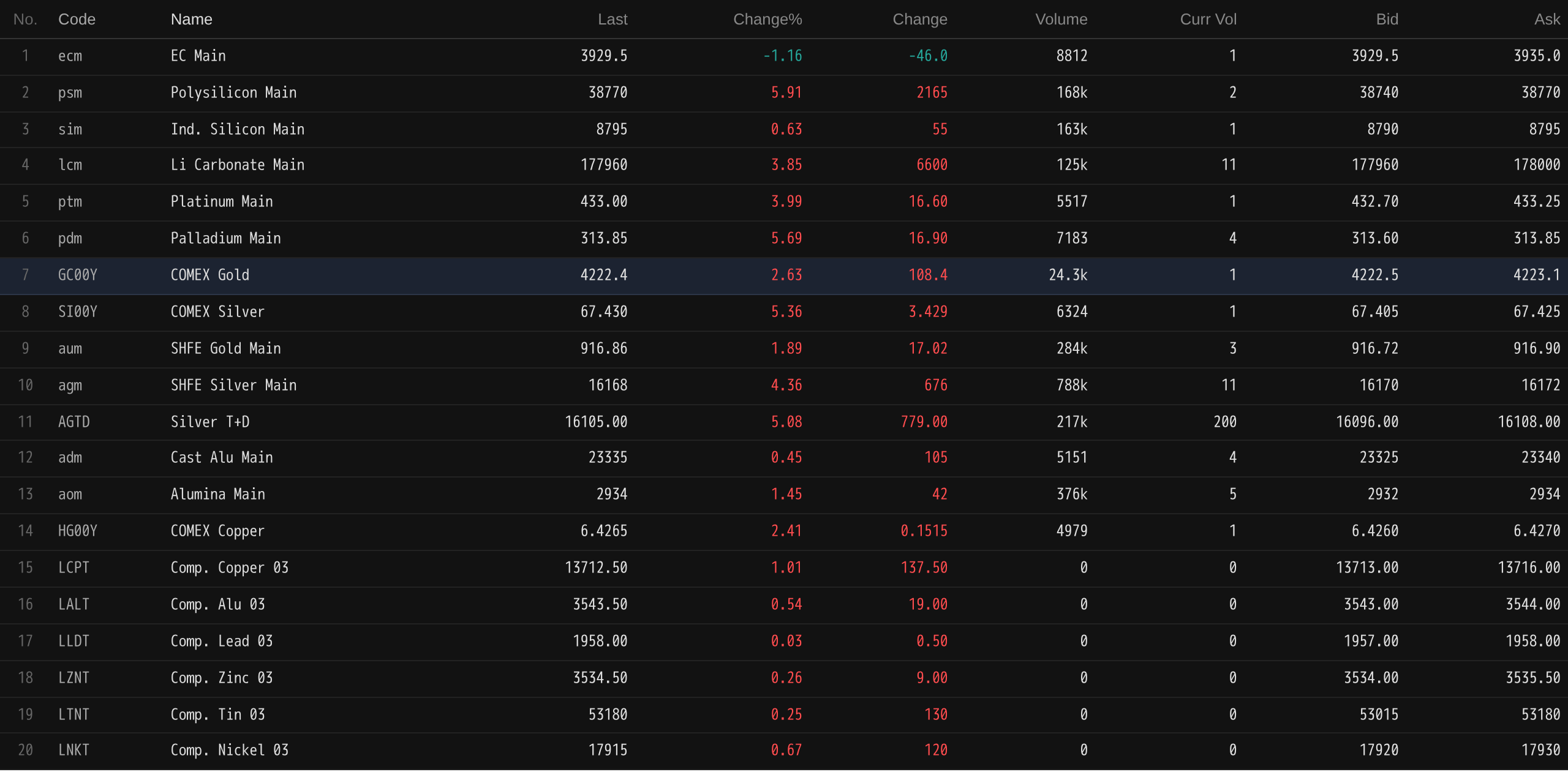

As of the midday close, domestic base metals nearly all rose. SHFE copper rose 1.51%, SHFE tin rose 2.97%. SHFE nickel rose 0.94%. SHFE aluminum rose 1.06%. SHFE zinc rose 0.43%. SHFE lead fell 0.31%.

In addition, casting aluminum linked futures rose 0.45%, alumina most-traded linked futures rose 1.45%. Lithium carbonate most-traded linked futures rose 3.85%. Silicon metal most-traded linked futures rose 0.63%. Polysilicon linked futures rose 5.91%.

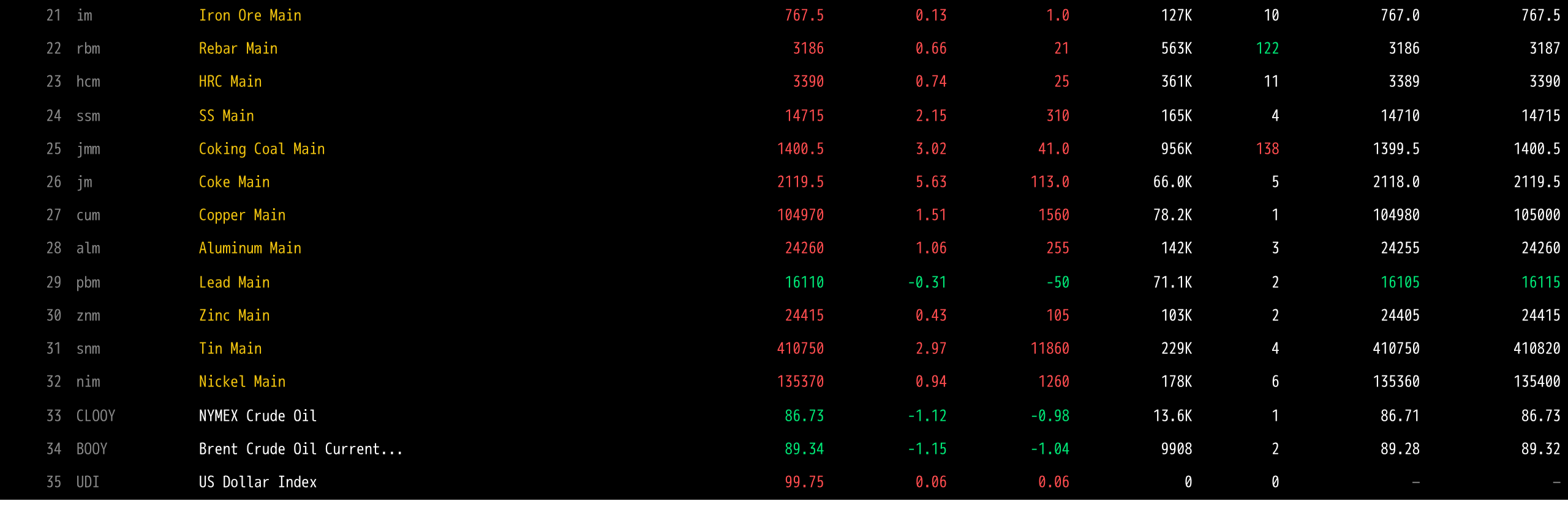

Ferrous metals all rose, iron ore rose 0.13%, rebar rose 0.66%, hot-rolled coil rose 0.74%, stainless steel rose 2.15%. Coking coal and coke: coking coal most-traded contract rose 3.02%, coke most-traded contract rose 5.63%.

Overseas base metals: as of 11:38 AM, LME metals all rose. LME copper rose 1.01%, LME aluminum rose 0.54%, LME lead edged up. LME zinc rose 0.26%, LME tin rose 0.25%, LME nickel rose 0.67%.

Precious metals: as of 11:38 AM, COMEX gold rose 2.63%, COMEX silver rose 5.36%. Domestic precious metals: SHFE gold most-traded linked futures rose 1.89%, SHFE silver most-traded linked futures rose 4.36%.

Furthermore, as of the midday close, platinum most-traded linked futures rose 3.99%, palladium most-traded linked futures rose 5.69%.

As of the midday close, the most-traded Europe container shipping futures contract fell 1.16% to 3,929.5 points.

As of 11:38 AM on June 12, some futures midday quotes:

Spot and fundamentals

Copper: Today, Guangdong #1 copper cathode spot against the front-month contract: high-quality copper reported at 270 yuan/mt up 30 yuan/mt from the previous trading day, standard-quality copper reported at a premium of 210 yuan/mt up 30 yuan/mt, SX-EW copper reported at a premium of 150 yuan/mt up 30 yuan/mt. The average price of Guangdong #1 copper cathode was 104,715 yuan/mt up 1,090 yuan/mt from the previous trading day, and the average price of SX-EW copper was 104,625 yuan/mt up 1,075 yuan/mt. Spot market: Guangdong inventory has declined for 9 consecutive days and has now hit a new low for the year...

Macro front

China:

[PBOC's open market operations net injected 178 billion yuan on the day, and net injected 885.8 billion yuan this week] PBOC conducted 393 billion yuan of 7-day reverse repo operations today, with 215 billion yuan of 7-day reverse repos maturing, resulting in a net injection of 178 billion yuan on the day. This week, PBOC conducted 1,112 billion yuan of 7-day reverse repo operations, with 226.2 billion yuan of 7-day reverse repos maturing, realizing a net injection of 885.8 billion yuan this week. (Jinshi Data APP)

[Guangzhou: Fully Advance the Implementation of Major Projects Such as Intelligent Connected Vehicles and NEVs, Artificial Intelligence, Semiconductors and Integrated Circuits, and Low-Altitude Economy] The “Guangzhou Commerce Development 15th Five-Year Plan (Draft for Public Comments)” was released for public consultation. It highlighted the need to fully advance the implementation of major projects including intelligent connected vehicles and NEVs, ultra-high-definition video and new-type displays, green petrochemicals and new materials, intelligent equipment and robotics, artificial intelligence, semiconductors and integrated circuits, and low-altitude economy, and cultivate a group of leading intermediate product enterprises that are high-tech, manufacturing single champions, and specialized and sophisticated. Promote the accelerated development of intermediate product trade in foreign trade transformation and upgrading bases, and cultivate a number of well-known brands and “chain leader” enterprises. Support enterprises in using technologies such as the industrial internet, big data, and artificial intelligence for digital transformation, improving production efficiency and product quality, and driving the intermediate product trade to leap toward high-end and digital-intelligent development. (Jinshi Data APP)

On the US dollar front:

As of 11:38, the US dollar index rose 0.06% to 99.75. According to CME “FedWatch”: The probability that the US Fed will keep interest rates unchanged through June is 98.5%, and the probability of a cumulative 25bp rate cut is 1.5%. The probability that the US Fed will keep interest rates unchanged through July is 91.3%, the probability of a cumulative 25bp rate hike is 7.4%, and the probability of a cumulative 25bp rate cut is 1.4%. Market expectations for a US Fed rate hike have been pushed back from December this year to January next year, and the possibility of a rate hike this year is no longer fully priced in. (Jinshi Data APP)

Amid sustained inflationary pressure driven by the Iran war, US producer prices in May rose at the fastest pace in more than three years. Data released by the Bureau of Labor Statistics on Thursday showed that the US PPI rose 6.5% YoY in May, the largest increase since November 2022, and rose 1.1% MoM. The core PPI, excluding food and energy, rose 4.9% YoY. The report highlighted the growing damage to the US economy from the energy price shock caused by the closure of the Strait of Hormuz. As the conflict is unlikely to be resolved in the short term, businesses are passing on higher energy and transportation costs, and other goods and services are also becoming more expensive. Combined with data earlier this week showing that consumer prices in May rose at the fastest pace in three years, Thursday's PPI report may further strengthen market expectations for a US Fed rate hike in 2026. As the labour market appears to be regaining growth momentum, the US Fed is shifting its focus to curbing inflation.

Data:

Today will see the release of Germany's final May CPI MoM, UK April GDP 3-month average MoM, UK April manufacturing production MoM, UK April seasonally adjusted trade balance in goods, UK April industrial production MoM, France final May CPI MoM, the US preliminary June 1-year inflation expectations, and the US preliminary June University of Michigan consumer sentiment index. In addition, attention should be paid to: the Huawei Developer Conference, Jun 12-14; Elon Musk's commercial aerospace company SpaceX plans to list on Nasdaq on June 12, 2026.

Crude Oil:

As of 11:38, oil prices fell in both markets, with WTI down 1.12% and Brent down 1.15%. The US and Iran are close to reaching a preliminary agreement on a memorandum of understanding, and oil prices pulled back slightly.

According to CCTV, on June 11 local time, US President Trump posted on the social platform "Truth Social" that, given negotiations with Iran had been submitted to Iran's highest leadership and approved, he had canceled strikes and bombing operations originally scheduled for that evening against Iran.

According to the latest OPEC data, Iran's crude oil production fell 19% last month as the US blockaded the country's ports during the ongoing conflict. Monthly report data released Thursday showed Iran's daily output fell by 546,000 barrels to 2.33 million barrels per day. OPEC's latest monthly report showed the organization on Thursday lowered its 2026 global oil demand growth forecast to 970,000 barrels per day, its second consecutive downward revision. Since the outbreak of the Iran war, the producer group has consistently viewed the conflict's impact on consumption as smaller than other forecasters such as the US Energy Information Administration and the International Energy Agency. Both expect demand to decline in 2026. The report also noted that the oil producer group raised its forecast for 2027 oil demand growth. (Jin10 Data APP)

Spot Market Overview:

►

►

►

►

►

►

►

►

►

►

►

►

![Inventory Hit a New Low, Suppliers Actively Held Prices Firm, Premium Cumulatively Surged by 230 yuan/mt This Week [SMM South China Spot Copper]](https://imgqn.smm.cn/usercenter/CJXfS20251217171710.jpg)

![Semiconductor Counter-Trend Rebound Coupled with Geopolitical Reversal Outside China, SHFE Tin Contract Center Pulled Back [SMM Tin Midday Review]](https://imgqn.smm.cn/usercenter/fMkfI20251217171752.jpg)

![Rising copper prices dampen downstream buying interest, market cools down again [SMM North China spot copper]](https://imgqn.smm.cn/usercenter/fEiiq20251217171711.jpg)