Data: SHFE, pergerakan pasar DCE (09 Jun)

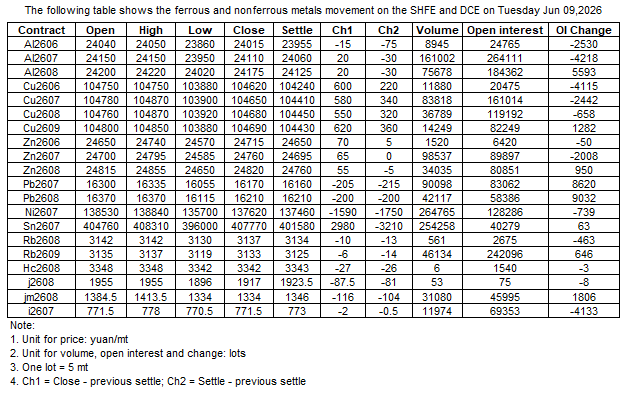

Tabel berikut menunjukkan pergerakan logam besi dan non-besi di SHFE dan DCE pada 09 Juni 2026

Pernyataan Sumber Data: Kecuali informasi yang tersedia untuk publik, semua data lainnya diproses oleh SMM berdasarkan informasi publik, komunikasi pasar, dan mengandalkan model database internal SMM. Hanya untuk referensi dan tidak menjadi rekomendasi pengambilan keputusan.

Untuk pertanyaan atau informasi lebih lanjut, silakan hubungi: lemonzhao@smm.cn

Untuk informasi lebih lanjut tentang cara mengakses laporan penelitian kami, hubungi:service.en@smm.cn

Berita Terkait

![[Southern Taiwan steel mills turn to direct negotiations to revive rebar sales]](https://imgqn.smm.cn/usercenter/crVox20251217171717.jpg)

1 menit yang lalu

[Southern Taiwan steel mills turn to direct negotiations to revive rebar sales]

Baca Selengkapnya

[Southern Taiwan steel mills turn to direct negotiations to revive rebar sales]

Rebar producers in southern Taiwan have stopped issuing official price quotes this week, shifting to flexible individual negotiations to attract buyers. Distributors have lowered retail rates in response to the sluggish market. The trading pause threatens to extend market stagnation to a ninth consecutive week without significant deals. Mills face severe order shortages and rising inventory backlogs from delayed shipments, leaving producers open to any offer without a fixed baseline. Despite this, distributor interest remains minimal. After two months of inventory reduction, most smaller traders are depleted, leaving only large-scale distributors still operational.

1 menit yang lalu

![[AISI: US raw steel production in week ending July 4 rises w-o-w, y-o-y]](https://imgqn.smm.cn/usercenter/FGavQ20251217171717.jpg)

1 menit yang lalu

[AISI: US raw steel production in week ending July 4 rises w-o-w, y-o-y]

Baca Selengkapnya

[AISI: US raw steel production in week ending July 4 rises w-o-w, y-o-y]

US raw steel output reached 1.856 million net tons (approx 1.684 million tonnes) for the week ending July 4, 2026, at an 80.4% capability utilization rate. This represented a 4.3% increase from 1.780 million net tons (78.9%) in the same period last year, and a 0.8% increase from the previous week's 1.842 million net tons (79.8%). Year-to-date production through July 4 totaled 48.112 million net tons (approx 43.65 million tonnes) at 78.8% utilization, up 6.0% from 45.400 million net tons (76.8%) in the same period last year.

1 menit yang lalu

![[SMM Steel] Domestic Mills Slashing Prices Fails to Stimulate Buying; Wait-and-See Stance Dominates Vietnam HRC Market](https://imgqn.smm.cn/usercenter/mpffV20251217171715.jpg)

4 menit yang lalu

[SMM Steel] Domestic Mills Slashing Prices Fails to Stimulate Buying; Wait-and-See Stance Dominates Vietnam HRC Market

Baca Selengkapnya

[SMM Steel] Domestic Mills Slashing Prices Fails to Stimulate Buying; Wait-and-See Stance Dominates Vietnam HRC Market

[Vietnam] ASEAN hot-rolled coil (HRC) import offers ticked down to 535 USD/tonne CFR this week, with overall regional trading activity remaining deeply subdued in the thick of the seasonal doldrums. Facing an intersection of weak end-user demand and competitive import alternatives, local producers in Vietnam have been forced to lower their quotes to stimulate sales. However, as the substantial price reductions by the two major domestic mills last week were widely anticipated and import offers from international traders continue to hold a price advantage, local buyers showed little urgency to restock and largely maintain a strict wait-and-see stance. Notably, only isolated Indian HRC deals were reported closed at 525 USD/tonne CFR recently. Overall, given the reality of high regional inventory levels and sluggish downstream consumption, flat steel prices in Vietnam and neighboring nations will continue to face near-term headwinds.

4 menit yang lalu

Berita Terkait

[Southern Taiwan steel mills turn to direct negotiations to revive rebar sales]

Jul 07, 2026 16:47

[AISI: US raw steel production in week ending July 4 rises w-o-w, y-o-y]

Jul 07, 2026 16:47

[SMM Steel] Domestic Mills Slashing Prices Fails to Stimulate Buying; Wait-and-See Stance Dominates Vietnam HRC Market

Jul 07, 2026 16:43

[Jepang Berencana Menerapkan Bea Masuk Antidumping Sementara untuk Baja Tahan Karat Canai Dingin dari Tiongkok dan Taiwan]

Jul 07, 2026 16:36