[SMM Iron Ore] 4 June - Major Port Inventory Data

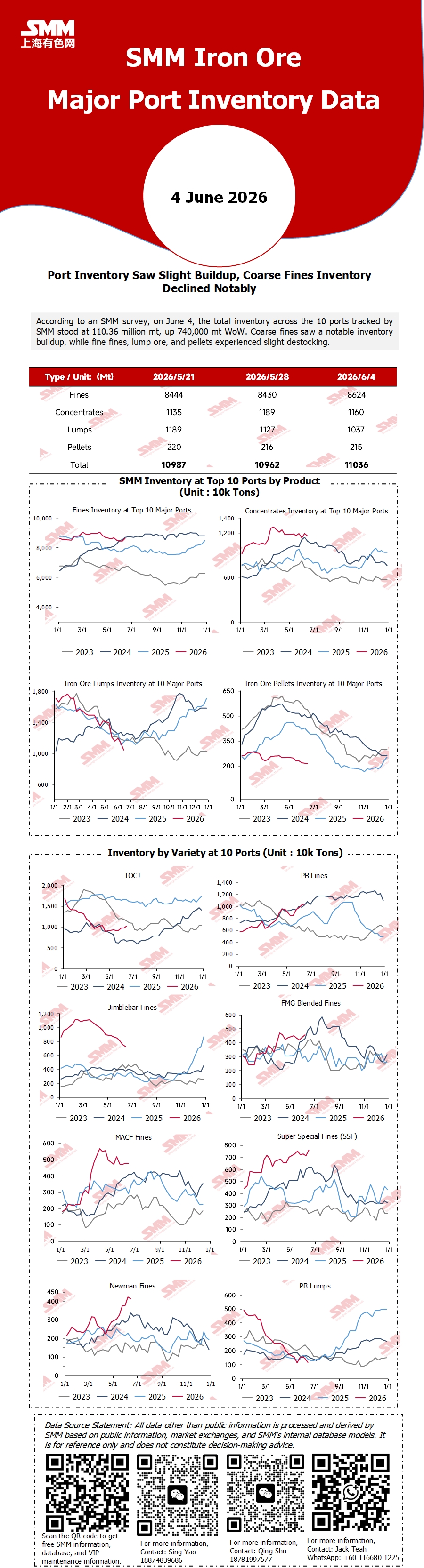

According to an SMM survey, on June 4, the total inventory across the 10 ports tracked by SMM stood at 110.36 million mt, up 740,000 mt WoW. Coarse fines saw a notable inventory buildup, while fine fines, lump ore, and pellets experienced slight destocking.

Data Source Statement: Except for publicly available information, all other data are processed by SMM based on publicly available information, market communication, and relying on SMM‘s internal database model. They are for reference only and do not constitute decision-making recommendations.

For any inquiries or to learn more information, please contact: lemonzhao@smm.cn

For more information on how to access our research reports, please contact:service.en@smm.cn

Related News

![[SMM Iron & Steel] Italy's Assofermet Warns EU Safeguard Measures and CBAM Threaten Downstream Steel Sector](https://imgqn.smm.cn/usercenter/JSngP20251217171719.jpg)

1 min ago

[SMM Iron & Steel] Italy's Assofermet Warns EU Safeguard Measures and CBAM Threaten Downstream Steel Sector

Read More

[SMM Iron & Steel] Italy's Assofermet Warns EU Safeguard Measures and CBAM Threaten Downstream Steel Sector

Italy's metallurgical and steel association, Assofermet, has issued a stark warning regarding the severe impact of the European Union's upcoming trade defense mechanisms on downstream processors and distributors. With the current steel safeguard regime set to expire on July 1, 2026, new provisions will introduce a strict annual duty-free quota of approximately 18.3 million metric tons (mt) for steel imports, and any volumes exceeding this cap will face a punitive 50% duty. Coupled with the mandatory origin tracing for steel melting and pouring, and the full implementation of the Carbon Border Adjustment Mechanism (CBAM) since January 1, 2026, these policies disproportionately favor upstream producers. Assofermet argues that this unbalanced protection will trigger surging raw material costs and reduced sourcing options for the downstream supply chain, which could ultimately suppress overall European steel demand and erode the continent's manufacturing competitiveness on the global stage.

1 min ago

![[SMM Iron & Steel] Prolonged Rail Disruptions Threaten Raw Material Supply for German Steelmakers](https://imgqn.smm.cn/usercenter/VgxkU20251217171719.jpg)

1 min ago

[SMM Iron & Steel] Prolonged Rail Disruptions Threaten Raw Material Supply for German Steelmakers

Read More

[SMM Iron & Steel] Prolonged Rail Disruptions Threaten Raw Material Supply for German Steelmakers

German steelmakers are facing critical logistical challenges as prolonged disruptions in rail freight transport threaten the reliable supply of essential raw materials like iron ore and coal. The German Steel Federation (WV Stahl) reported that ongoing repair works and inadequately prepared detour routes managed by DB InfraGO are jeopardizing plant operations, already resulting in the first instances of production disruptions. Coupled with existing pressures from weak downstream demand, high energy costs, and decarbonization mandates, these logistical bottlenecks present a severe risk to near-term capacity utilization. If network operators fail to promptly stabilize supply routes to major industrial centers, German mills may be forced to further scale back liquid steel output, which could tighten regional flat steel availability and impact local supply balances.

1 min ago

![[SMM Iron & Steel] Global Billet Prices Show Mixed Trends in May Amid Demand Shifts and Supply Realignments](https://imgqn.smm.cn/usercenter/VhIgs20251217171719.jpg)

1 min ago

[SMM Iron & Steel] Global Billet Prices Show Mixed Trends in May Amid Demand Shifts and Supply Realignments

Read More

[SMM Iron & Steel] Global Billet Prices Show Mixed Trends in May Amid Demand Shifts and Supply Realignments

In May 2026, global square billet markets exhibited a generally upward but fragmented trend, with average prices in most regional markets rising by $10–$20 per metric ton (mt). Black Sea FOB billet prices climbed by $13 to reach a 2025-high of $483/t, while Italy's Ex-Works prices increased by $18 to $621/t. Conversely, the Gulf region experienced a slight decline, with prices dropping from $518/t to $514/t. Furthermore, the National Bank of Ukraine forecasts that average billet prices will rise 4.9% year-on-year to $487.7/t FOB Ukraine in 2026. The mixed price movements highlight shifting trade flows; while solid domestic and Iranian demand allowed Russian suppliers to maintain firm pricing despite Turkish buyers seeking $505–$510/t CFR, the broader market lost momentum by late May due to weakening Chinese futures and inflation pressures in ASEAN countries.

1 min ago

Related News

[SMM Iron & Steel] Italy's Assofermet Warns EU Safeguard Measures and CBAM Threaten Downstream Steel Sector

Jun 04, 2026 14:45

[SMM Iron & Steel] Prolonged Rail Disruptions Threaten Raw Material Supply for German Steelmakers

Jun 04, 2026 14:45

[SMM Iron & Steel] Global Billet Prices Show Mixed Trends in May Amid Demand Shifts and Supply Realignments

Jun 04, 2026 14:45

[SMM Iron & Steel] Canada Extends Steel Tariffs and Quotas Until 2027 to Shield Domestic Industry

Jun 04, 2026 14:45