ArcelorMittal (AM) — 2025 Annual Report Summary

ArcelorMittal, the world's second-largest steel producer, released its 2025 Annual Report in March 2026. During the year, the Group's steelmaking operations experienced a broad-based slowdown: crude steel output in Europe contracted sharply by 6.6% year-on-year, while volumes in India and Brazil also declined. Only North America recorded output growth, driven by the consolidation of an additional steelworks. These dynamics reflect softening apparent steel consumption (ASC) globally, compounded by intensifying competitive pressures. Nonetheless, the Mining segment delivered an outstanding performance — iron ore shipments from Liberia surged 37.5%, providing a meaningful offset to the headwinds in the steelmaking divisions.

I. 2025 Key Production, Shipment & Financial Overview

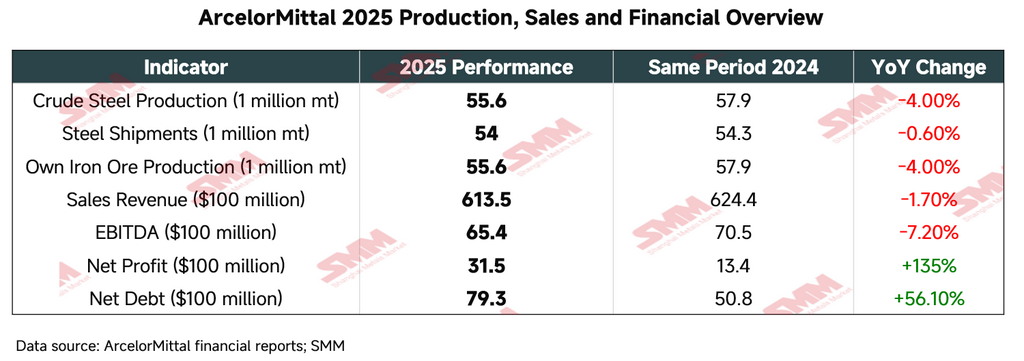

In 2025, ArcelorMittal demonstrated strong operational resilience against the backdrop of subdued global steel demand and complex trade barriers. Portfolio optimisation — notably the full consolidation of the Calvert flat-rolled finishing facility — and robust growth in the iron ore business were the key highlights of the year.

Despite a marginal decline in crude steel production and shipments, net profit expanded materially, primarily driven by non-recurring items — in particular, a US$1.9 billion accounting gain arising from the acquisition of the remaining 50% equity interest in AMNS Calvert. The increase in net debt was principally attributable to the full consolidation of Calvert and other M&A activities.

II. Segment Distribution & Operational Performance

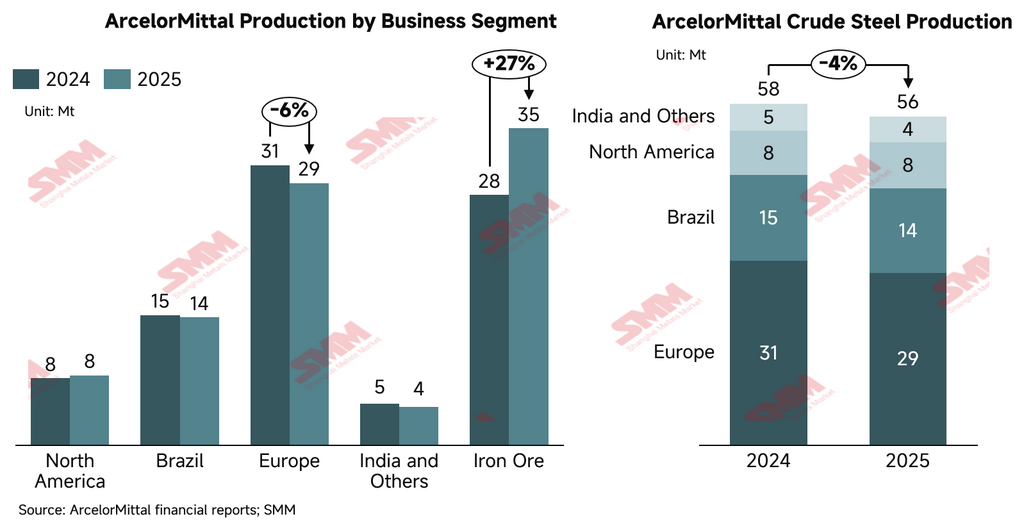

In 2025, ArcelorMittal's global operational footprint underwent significant structural reconfiguration, most notably through the full acquisition of the North American Calvert flat-rolling facility and the divestiture of non-core assets in Bosnia-Herzegovina, further optimising the Group's production and shipment mix. The following presents a detailed comparison of key segment production and shipment data for 2025 versus the prior year:

-

North America

The segment recorded growth in both output and shipments in 2025, primarily benefiting from the full consolidation of the AMNS Calvert facility in the second half of the year, and the recovery of Mexican production following the 2024 labour strike.

-

Crude Steel Production: 7.8 Mt (2024: 7.5 Mt), up 2.9% YoY

-

Steel Shipments: 10.3 Mt (2024: 10.1 Mt), up 2.2% YoY

-

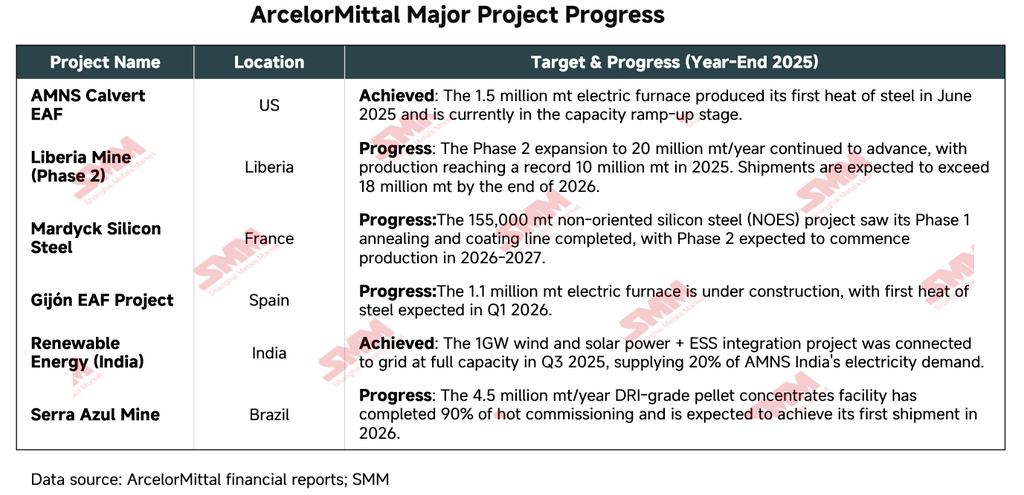

Key Development: The 1.5 Mtpa Electric Arc Furnace (EAF) at the Calvert facility was commissioned in June 2025, enhancing the supply capability of high value-added flat products in the region.

-

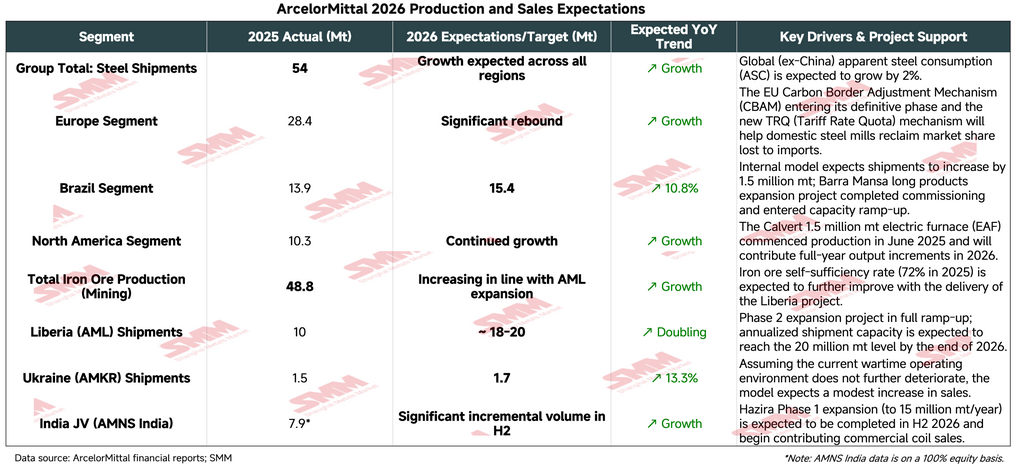

2026 Volume Outlook: Both production and shipments are expected to increase in line with broader regional trends.

-

Growth Driver: The 1.5 Mtpa EAF at Calvert, consolidated in H2 2025, is currently in capacity ramp-up phase and will contribute incremental volumes in 2026.

-

Brazil

Despite margin pressure, the Brazil segment maintained highly stable production and shipment volumes, continuing to serve as a key profitability pillar for the Group.

-

Crude Steel Production: 14.3 Mt (2024: 14.5 Mt), down 1.3% YoY

-

Steel Shipments: 13.9 Mt (2024: 14.1 Mt), down 0.9% YoY

-

Key Development: The Barra Mansa long products mill expansion was commissioned in H2 2025, adding 0.4 Mtpa of high value-added long steel capacity.

-

2026 Volume Outlook: Steel shipments are projected to reach 15.4 Mt in 2026, significantly above the 13.95 Mt recorded in 2025.

-

Growth Driver: Despite demand headwinds in 2025 caused by elevated interest rates and a surge in Chinese imports, the Group holds an optimistic outlook for 2026 growth.

-

Europe

Affected by soft market demand and a planned major reline of Blast Furnace No. 4 at Dunkirk, European crude steel output contracted. However, the smaller decline in shipments indicates relatively resilient market penetration.

-

Crude Steel Production: 29.2 Mt (2024: 31.2 Mt), down 6.6% YoY

-

Steel Shipments: 28.4 Mt (2024: 28.7 Mt), down 0.9% YoY

-

Key Development: The divestiture of the Zenica long products integrated steelworks in Bosnia-Herzegovina was completed in October, reflecting the Group's strategic transition toward lower-carbon assets.

-

2026 Volume Outlook: Shipments are expected to recover and grow.

-

Growth Driver: As the EU Carbon Border Adjustment Mechanism (CBAM) and the revised Tariff Rate Quota (TRQ) regime progressively take effect in 2026, the Group anticipates European domestic steelmakers recapturing market share from import competition.

-

India & Other Joint Ventures

Focus on the strategic joint venture AMNS India (60% equity interest):

-

Crude Steel Production: 7.2 Mt (2024: 7.5 Mt), down 4.5% YoY, impacted by market volatility in H1 and unplanned maintenance outages

-

Steel Shipments: 7.9 Mt (2024: 7.9 Mt), shipments remained resilient

-

Key Development: The Hazira integrated steelworks in India is being expanded to 15 Mtpa capacity. The Group has also announced a long-term greenfield project in Andhra Pradesh with an 8.2 Mtpa capacity target, with the objective of increasing hot-rolled coil (HRC) capacity to 15 Mtpa by H2 2026, providing incremental production and shipment uplift.

-

Crude Steel Production (Other Subsidiaries): 4.3 Mt (2024: 4.6 Mt), down 6.52% YoY

-

Mining

The Mining segment was the Group's strongest growth engine in 2025, driven by the successful ramp-up of the Phase II expansion project in Liberia.

-

Own Iron Ore Production (Mining segment only): 35.3 Mt (2024: 27.9 Mt), up 26.5% YoY

-

Iron Ore Shipments: 36.3 Mt (2024: 26.4 Mt), up 37.5% YoY

-

Key Development: Liberia achieved a record annual shipment of 10 Mt and is progressing steadily toward a 20 Mtpa production target.

2026 Mining Segment Outlook:

-

Liberia (AML):

-

Volume Target: 20 Mtpa shipment target. The Group specifically projects that by end-2026, as the Phase II expansion and the beneficiation plant continue to ramp up, annualised shipments will exceed 18 Mtpa (vs. 10 Mt in 2025).

-

Key Progress: A blended production model combining sinter fines and concentrates from Phase II will support a significant increase in production and shipment volumes, with rail haulage capacity being expanded toward a 30 Mtpa annual throughput target.

-

-

Canada (AMMC):

-

Trend: Stable production maintained. The conversion of the high-grade iron ore pellet plant for Direct Reduced Iron (DRI) production is expected to be completed in Q2 2026.

-

2026 Production & Shipment Outlook Summary

The 2025 production and shipment profile signals ArcelorMittal's strategic pivot toward quality over pure volume. Despite marginal fluctuations in crude steel output in Europe and Brazil, the growth from high value-added assets in North America and low-cost iron ore operations in Liberia is structurally rebuilding the Group's cost and margin base. The Group projects global apparent steel consumption (ASC) ex-China to grow by 2% in 2026. Against this macro backdrop, the Group forecasts an increase in steel production and shipments across all regions in 2026 compared to 2025, underpinned by improvements in operational efficiency and the positive impact of trade protection measures.

III. Production Infrastructure & Process Technology Profile

ArcelorMittal operates a highly diversified asset portfolio spanning the full upstream-to-downstream value chain — from iron ore mining to downstream finishing and processing. As of end-2025, the Group's production process structure is as follows:

-

Process Mix: Basic Oxygen Furnace (BOF) output accounts for 74% (41.2 Mt); Electric Arc Furnace (EAF) accounts for 26% (14.4 Mt).

-

Facility Scale: The Group currently operates 30 Blast Furnaces (BF) and 27 Electric Arc Furnaces (EAF).

-

Capacity Distribution: Europe remains the largest production base, with an annual crude steel capacity of 39.5 Mt (53% of total), followed by Brazil (16.4 Mt) and North America (12.5 Mt).

IV. Raw Material Self-Sufficiency & Supply Chain Integration

The Group maintains a high degree of vertical integration upstream and downstream to hedge against market volatility — a core pillar of its industrial competitive advantage:

-

Iron Ore Supply: Own iron ore production grew 15.1% YoY to 48.8 Mt in 2025. Canada (AMMC) contributed 25.6 Mt, while Liberia (AML) surged to 9.7 Mt.

-

Self-Sufficiency Rates: In 2025, the Group achieved an iron ore self-sufficiency rate of 72%, a coking coal self-sufficiency rate of 91%, and a scrap steel and Direct Reduced Iron (DRI) self-sufficiency rate of 55%.

-

Logistics Capacity: The Group operates 18 deep-water port facilities and associated rail infrastructure, handling over 51 Mt of freight annually.

V. Key Asset Restructuring & Industrial Portfolio Realignment

2025 was a year of deep portfolio optimisation for the Group — divesting weaker assets and concentrating resources in high-growth, high value-added operations.

-

Full Consolidation of Calvert (USA): In June 2025, the Group completed the acquisition of the remaining 50% equity interest in AMNS Calvert (previously a joint venture with Nippon Steel Corporation) at a nominal consideration. The facility is the most advanced flat-rolled steel finishing complex in North America. The newly constructed 1.5 Mtpa EAF produced its first slab in June 2025.

-

Asset Divestitures & Operational Rationalisation:

-

Bosnia-Herzegovina: Completed the sale of the Zenica integrated steelworks and the Prijedor iron ore mine.

-

South Africa: Rationalisation of the long products business and the idling of the Newcastle steelworks were completed by end of January 2026.

-

-

India Expansion: AMNS India remains a core growth engine. The Hazira integrated steelworks is on track to expand capacity to 15 Mtpa by H2 2026.

VI. Major Capital Project Progress (Capex Allocation)

ArcelorMittal is currently in a dual capital expenditure cycle: EAF transition and upstream iron ore capacity expansion. Total capital expenditure in 2025 amounted to US$4.34 billion.

VII. Decarbonisation Pathway & Industrial Technology Upgrade

ArcelorMittal is at a critical juncture in its transition from conventional blast furnace-based integrated steelmaking toward low-carbon process routes:

-

EAF Capacity Expansion: By end-2026, the Group expects to add 3.4 Mtpa of EAF capacity, spanning Gijón and Sestao in Spain, and Calvert in the USA.

-

Key Technology Projects: The 2.0 Mtpa EAF project at Dunkirk, France (€1.3 billion investment) is planned for commissioning in 2029 and is expected to generate carbon emissions at approximately one-third of the level of a conventional blast furnace.

-

Energy Transition: By end-2025, the Group had commissioned 1.6 GW of renewable energy equity capacity, with a further 1.2 GW under construction, primarily in India and South America, with the objective of supplying low-cost clean electricity to steelmaking operations.

-

Carbon Footprint: Absolute carbon emissions declined 3.1% YoY in 2025, representing a cumulative reduction of 47% from the 2018 baseline. It is noteworthy that, given the limited commercial-scale deployment of low-carbon technologies (green hydrogen, Carbon Capture and Storage), the Group's emissions reductions are currently achieved primarily through portfolio restructuring and EAF electrification.

VIII. Additional Key Information

-

Portfolio Optimisation:

-

Full Acquisition of Calvert: By acquiring NSC's 50% equity stake, ArcelorMittal has gained full operational control of North America's most advanced flat-rolled steel finishing complex.

-

Exit from Non-Core Assets: The divestiture of the high-carbon-intensity integrated steelworks at Zenica, Bosnia-Herzegovina, and associated iron ore mines reflects a "decarbonise first, then grow" portfolio strategy.

-

-

Operational Risks:

-

Geopolitical Risk: The Kryvyi Rih steelworks in Ukraine (AMKR) is currently operating at only 35% of rated capacity, facing significant logistics and supply chain disruption.

-

Trade Barriers: US Section 232 tariffs were raised to 50% in 2025, increasing the cost burden on cross-regional material flows.

-

-

2026 Outlook: Global apparent steel consumption (ASC) ex-China is projected to grow 2%. The Group's capital expenditure plan for 2026 is budgeted in the range of US$4.5–5.0 billion, with continued focus on the Liberia iron ore expansion and the electrification of process technology in Europe.

Summary: 2025 was a year of "deepening asset quality" for ArcelorMittal. By converting its core North American joint venture Calvert into a wholly-owned subsidiary, and achieving successful delivery milestones at the Liberia iron ore mine and India's green energy projects, the Group further consolidated its vertically integrated competitive advantages. For investors, the sustainability of free cash flow generation and the recovery of market share under the EU CBAM framework remain the key monitoring indicators over the next one to two years.

![[SMM Steel] South Korea Overtakes China as Brazil’s Largest CRC Supplier](https://imgqn.smm.cn/usercenter/zLhJl20251217171720.jpg)

![[SMM Iron & Steel] Turkish Metal Producers' Foreign Sales Prices Rise 3.31% in April 2026 Amid Persistent Inflation](https://imgqn.smm.cn/usercenter/JdqON20251217171718.png)