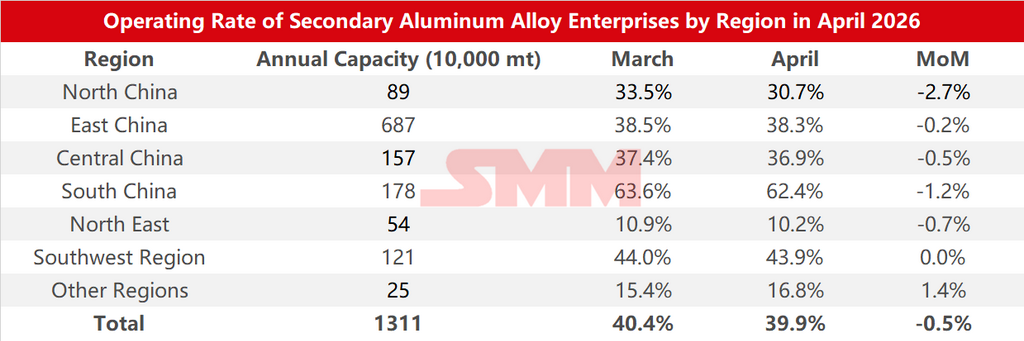

Data Survei Tingkat Utilisasi Perusahaan Aluminium Sekunder Berdasarkan Wilayah pada April 2026:

Menurut statistik survei SMM, tingkat utilisasi industri aluminium sekunder pada April 2026 turun tipis 0,5 poin persentase MoM dari Maret menjadi 39,9%.

Divergensi produksi antarperusahaan terlihat jelas pada April. Tingkat utilisasi yang relatif stabil terutama ditopang oleh tiga faktor: pertama, pusat harga spot ADC12 bergeser turun pada April, menstimulasi sebagian klien yang sensitif terhadap harga dan mendorong pemulihan parsial permintaan pesanan;

Kedua, selisih harga antara pasar domestik dan luar negeri terus melebar, meningkatkan keuntungan ekspor. Beberapa perusahaan secara aktif menyesuaikan struktur pesanan dan meningkatkan proporsi ekspor, mengimbangi tekanan dari penurunan pesanan domestik;

Ketiga, di tengah melemahnya harga spot, pedagang masuk pasar dengan harga rendah untuk membeli ingot paduan, sebagian mengisi celah pesanan yang disebabkan oleh melemahnya konsumsi pengguna akhir.

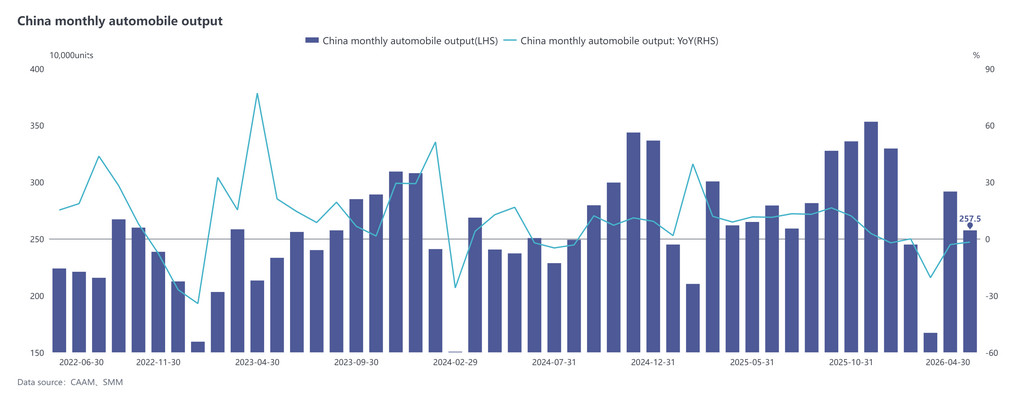

Namun, pemangkasan produksi juga cukup meluas di seluruh industri, terutama disebabkan oleh melemahnya konsumsi pengguna akhir. Menurut data CAAM, produksi dan penjualan mobil pada April masing-masing mencapai 2,575 juta unit dan 2,526 juta unit, turun 11,7% dan 12,9% MoM, serta turun 1,7% dan 2,5% YoY. Tekanan pada permintaan pengguna akhir menyebabkan kontraksi pesanan di pabrik aluminium sekunder dan meningkatnya tekanan penjualan, yang secara pasif menekan tingkat utilisasi. Namun, beberapa perusahaan tidak menyesuaikan laju produksi mereka, dan ketidaksesuaian antara produksi dan penjualan mengakibatkan akumulasi persediaan produk jadi yang berkelanjutan.

Tekanan bahan baku juga tidak boleh diabaikan. Pada awal April, kenaikan harga aluminium primer mendorong naiknya biaya skrap aluminium. Pengawasan yang lebih ketat terhadap faktur balik, dikombinasikan dengan selisih harga terbalik antara pasar domestik dan luar negeri, menyebabkan pasokan barang berfaktur ketat dan volume sirkulasi pasar rendah. Dari pertengahan April dan seterusnya, harga aluminium berbalik turun, tetapi skrap aluminium hanya turun sedikit karena pemasok menahan penjualan, menyebabkan keseimbangan laba-rugi teoretis industri bergeser dari untung menjadi rugi, semakin menyoroti tekanan operasional pada perusahaan. Dalam kondisi ini, beberapa perusahaan terpaksa mengurangi beban atau bahkan menghentikan produksi karena pasokan bahan baku yang tidak mencukupi atau kendala kebijakan kepatuhan.

Secara keseluruhan, divergensi produksi antarperusahaan di industri paduan aluminium sekunder cukup signifikan pada April, dengan tingkat operasi keseluruhan turun tipis dalam kisaran sempit.

Memasuki Mei, permintaan melanjutkan tren pelemahan sejak pertengahan April, dan pola lesu ini kemungkinan tidak akan berubah dalam jangka pendek. Perusahaan hilir memiliki ekspektasi hati-hati terhadap prospek pasar, menilai harga belum mencapai titik rendah bertahap, dengan keinginan restocking yang lemah dan sentimen wait-and-see terus mendominasi pasar. Pengurangan pesanan bertahap selama libur Hari Buruh secara langsung membebani produksi perusahaan. Meskipun tingkat utilisasi sedikit rebound setelah libur, pemulihannya terbatas. Di bawah tekanan gabungan dari musim sepi permintaan yang berkepanjangan, pasokan bahan baku yang sesuai kepatuhan yang ketat, dan pembatasan faktur balik, tingkat utilisasi keseluruhan industri pada Mei masih memiliki ruang untuk penurunan lebih lanjut.

![Harga Aluminium Merosot dan Melemah, Selisih Harga Spot-Futures Melonjak Tajam [Tinjauan Harian Aluminium Spot Tiongkok Selatan SMM]](https://imgqn.smm.cn/usercenter/uoPaX20251217171651.jpg)

![[Berita Kilat Aluminium SMM] GeT Alloys Ganti Minyak Bakar Berat dengan Bahan Bakar Berasal dari Ban dalam Daur Ulang Aluminium](https://imgqn.smm.cn/usercenter/tYQzs20251217171653.jpg)

![[SMM Aluminum Flash News] Woodside Menandatangani Perjanjian Pasokan Gas dengan Alcoa untuk Mendukung Produksi Alumina](https://imgqn.smm.cn/usercenter/EVjRH20251217171653.jpg)