SMM May 11 News:

Metals market:

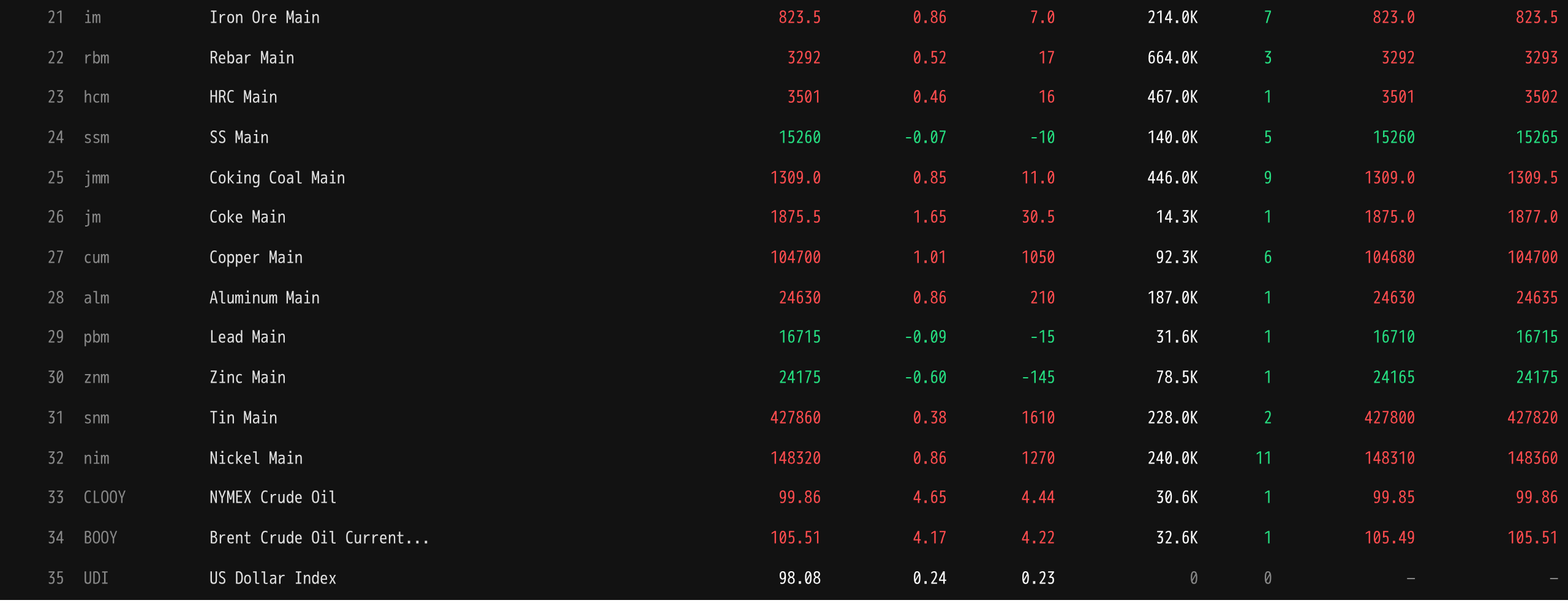

As of the midday close, domestic market base metals mostly rose. SHFE copper was up 1.01%, SHFE aluminum up 0.86%, SHFE lead edged down slightly, SHFE zinc fell 0.6%, SHFE tin was up 0.38%, and SHFE nickel up 0.86%.

In addition, the most-traded casting aluminum futures rose 1.09%, the most-traded alumina contract fell 0.81%, the most-traded lithium carbonate contract rose 3.1%, the most-traded silicon metal contract rose 1.66%, and the most-traded polysilicon futures fell 2.8%.

Ferrous metals mostly rose. Iron ore was up 0.86%, rebar up 0.52%, hot-rolled coil up 0.46%, and stainless steel down 0.07%. Coking coal and coke: the most-traded coking coal contract rose 0.85%, and the most-traded coke contract rose 1.65%.

Overseas market base metals, as of 11:46, LME metals were nearly all up. LME copper rose 0.59%, LME aluminum up 0.67%, LME zinc down 0.31%, LME lead edged up slightly, LME tin up 1.16%, and LME nickel up 1.29%.

Precious metals, as of 11:46, COMEX gold fell 0.77% and COMEX silver rose 0.66%. Domestic market precious metals: the most-traded SHFE gold contract fell 0.96%, and the most-traded SHFE silver contract rose 0.68%.

In addition, as of the midday close, the most-traded platinum futures rose 0.14%, and the most-traded palladium futures fell 0.62%.

As of the midday close, the most-traded Europe containerized freight index contract rose 5.07% to 2,474.5 points.

As of 11:46 on May 11, midday futures quotes for selected contracts:

Spot and Fundamentals

Lead:An SMM survey showed that in April, refined lead supply from secondary lead enterprises edged up MoM, mainly driven by production resumptions at previously idled enterprises and restocking of raw materials to boost output...

Macro Front

China:

[NBS: April CPI Up 1.2% YoY, PPI Up 2.8% YoY, PPI Growth Expanded]NBS data showed that in April 2026, the national consumer price index rose 1.2% YoY. Among them, urban areas were up 1.2% and rural areas up 1.0%; food prices fell 1.6%, while non-food prices rose 1.8%; consumer goods prices rose 1.4%, and services prices rose 0.9%. On average from January to April, the national CPI was up 0.9% YoY. In April, the national CPI rose 0.3% MoM. Among them, urban areas were up 0.3% and rural areas up 0.1%; food prices fell 1.6%, while non-food prices rose 0.7%; consumer goods prices rose 0.1%, and services prices rose 0.5%. In April 2026, national industrial producer ex-factory prices rose 2.8% YoY and 1.7% MoM. Industrial producer purchase prices rose 3.5% YoY and 2.1% MoM. For the January–April average, industrial producer ex-factory prices were up 0.2% from the same period last year, and industrial producer purchase prices were up 0.5%. Dong Lijuan, Chief Statistician of the Urban Division of the National Bureau of Statistics (NBS), interpreted the April 2026 CPI and PPI data. The main characteristics of PPI MoM movements this month were as follows: First, international input factors drove up prices in China's petroleum-related industries. Rising international crude oil prices drove up prices in domestic petroleum-related industries. Specifically, prices in the petroleum and natural gas extraction industry rose 18.5% MoM, petroleum, coal, and other fuel processing industry prices rose 16.4%, chemical raw materials and chemical products manufacturing prices rose 8.3%, chemical fiber manufacturing prices rose 5.6%, and rubber and plastics products industry prices rose 1.7%. Second, increased demand in some domestic industries drove prices higher. Rapid growth in computing power demand and accelerated electrification pushed optical fiber manufacturing prices up 22.5% MoM, external storage devices and components prices up 3.2%, and non-ferrous metal smelting and rolling processing industry prices up 0.2%. Restocking demand for thermal coal was released, combined with increased non-power coal demand from chemical and metallurgical industries, driving coal mining and washing industry prices up 1.9%. Continued advancement of manufacturing equipment upgrades drove increased steel demand, pushing ferrous metals smelting and rolling processing industry prices up 0.6%. Third, competition order in the Chinese market continued to improve, with prices in related industries rising or declines narrowing. Efforts to address "involution-style" competition continued to show results, with lithium-ion battery manufacturing prices up 1.6% MoM, new energy vehicle manufacturing prices down 0.1%, with the decline narrowing by 0.7 percentage points from the previous month.

The PBOC conducted 500 million yuan in 7-day reverse repo operations today. As no reverse repos matured today, a net injection of 500 million yuan was achieved.

US dollar:

As of 11:46, the US dollar index was up 0.24% at 98.08. Data from the US Department of Labor showed that US April non-farm payrolls added 115,000 jobs, far exceeding expectations, thanks to strong corporate earnings and enterprises' effective response to supply chain disruptions triggered by the Iran war. The unemployment rate held steady at 4.3%, in line with economists' expectations. From trade to immigration to tax policy, changes across various fronts posed challenges for enterprises, but most did not resort to large-scale layoffs. At the same time, enterprises appeared to take various intertwined headwinds in stride. Robust consumer demand meant that despite news of high-profile layoffs at well-known companies, low hiring was often accompanied by relatively low levels of layoffs. Data from the Department of Labor and human resources firm ADP earlier this week showed that the job market was stabilizing. Strong hiring in healthcare and social assistance also underpinned overall employment figures. US equities at or near record highs boosted confidence among corporate CEOs. The full impact of the conflict with Iran and the resulting rise in energy prices had yet to manifest in the labour market. Rising US oil prices had put greater pressure on lower-income households, which could dampen travel and services spending, in turn dragging on hiring in sectors such as retail and leisure. The impact of higher oil prices was particularly severe for airlines. However, these effects had yet to show up clearly in monthly employment data. According to the CME "Fed Watch": the probability of the US Fed holding rates unchanged through June was 93.8%, with a 6.2% probability of a cumulative 25 basis point interest rate cut. The probability of the US Fed holding rates unchanged through July was 88.8%, with a 10.8% probability of a cumulative 25 basis point cut and a 0.3% probability of a cumulative 50 basis point cut. (Jin10 Data)

Goldman Sachs expects the US Fed to cut interest rates by 25 basis points each in December 2026 and March 2027, compared with its previous forecast of cuts in September and December this year.

A CITIC Securities research report noted that US nonfarm payrolls in April 2026 came in above expectations, while the unemployment rate of 4.3% was in line with expectations. We believe April data better reflected the current state of the US job market than the previous two months: first, one-off factors diminished in April; second, the enterprise response rate was higher in April; and third, the Birth-death model impact was the smallest among the last four data releases. Demand side, the US labour market in April exhibited overall resilience with marginally increasing layoff pressure. Supply side, the labour force participation rate and employment-population ratio declined, but the prime-age (25–54) participation rate remained stable, suggesting it was not a large-scale exit of core labour force but rather aging and retirement factors dragging down the overall participation rate. Regarding US Fed monetary policy, we maintain our previous view: after Waller takes over, if the Iran situation eases and oil prices pull back, driving inflation expectations lower, the base case for H2 is one interest rate cut of 25 bps.

Other currencies:

Bearish yen positions decreased significantly after Japanese authorities intervened to support the yen, highlighting how official action curbed this crowded trade. According to data from the US Commodity Futures Trading Commission (CFTC), leveraged funds reduced their net short positions on the yen in the week ending May 5. Currently, their net short position in the Japanese yen stood at 61,340 contracts, valued at approximately $4.9 billion, hitting the lowest level in nearly a month. Meanwhile, asset management firms also cut 13,839 short contracts, bringing their open interest down to 10,653 contracts. "Given the intervention risk and strong official warnings, chasing yen shorts near the 160 level has become unattractive," said Stefan Rittner, Senior Portfolio Manager at Allianz Global Investors. He held a neutral stance on the USD/JPY exchange rate. However, he noted that "despite the yen's already cheap valuation, persistent structural headwinds limit the scope for a sustained rebound"; moreover, further intervention risks are expected to rise once the USD/JPY rate approaches its previous highs again. (Jin10 Data)

On the macro front:

Data to be released today include US April existing home sales annualized total and China's April M2 money supply year-on-year. In addition, attention should be paid to: US Treasury Secretary Bessent's visit to Japan, where he will meet with the Japanese Prime Minister, the central bank governor, and the Finance Minister.

Crude oil:

As of 11:46, oil prices in both markets surged significantly, with WTI up 4.65% and Brent up 4.17%. Renewed tensions between the US and Iran supported oil prices.

According to Xinhua News Agency, US President Trump posted on social media on May 10, expressing dissatisfaction with Iran's response, calling it "completely unacceptable." This statement cast a shadow over the already fragile Middle East ceasefire situation. Oil prices jumped sharply after the news broke. (Wallstreetcn)

Data from shipping intelligence firm Kpler showed that two more fully loaded crude oil tankers switched off their trackers while passing through the Strait of Hormuz last week to evade Iranian attacks. Data indicated that the very large crude carrier "Basrah Energy" loaded 2 million barrels of Upper Zakum crude oil from ADNOC's Zirku terminal on May 1 and passed through the Strait of Hormuz on May 6. The vessel discharged its cargo at the Fujairah tanker terminal on May 11. It remained unclear which company chartered the tanker owned and managed by shipping company Sinokor. ADNOC and its buyers had recently dispatched tankers through the Strait of Hormuz on multiple occasions to transport crude oil, in response to the issue of stranded oil in the Persian Gulf caused by Middle East conflicts. Another very large crude carrier, Kiara M, switched off its transponder and departed the Persian Gulf on Sunday, carrying 2 million barrels of Iraqi crude oil. The discharge destination of this San Marino-flagged tanker remained unclear. (Jin Shi Data)

Spot Market Overview:

►

►

►

►

►

►

►

►

►

►

![[SMM Flash News] Indonesia’s ESDM Minister Suspends Planned Royalty Hikes to Re-evaluate Formulas](https://imgqn.smm.cn/usercenter/ipCjz20251217171734.jpeg)

![[SMM Tin News Flash: Toyota to Build New Auto Plant in India with Annual Capacity of 100,000 Units]](https://imgqn.smm.cn/usercenter/gpWpd20251217171734.jpeg)

![Shanghai Spot Copper Premiums Continued Weak Trend, Approaching Delivery Limited Downside Room [SMM Shanghai Spot Copper]](https://imgqn.smm.cn/usercenter/qcyEh20251217171709.jpg)