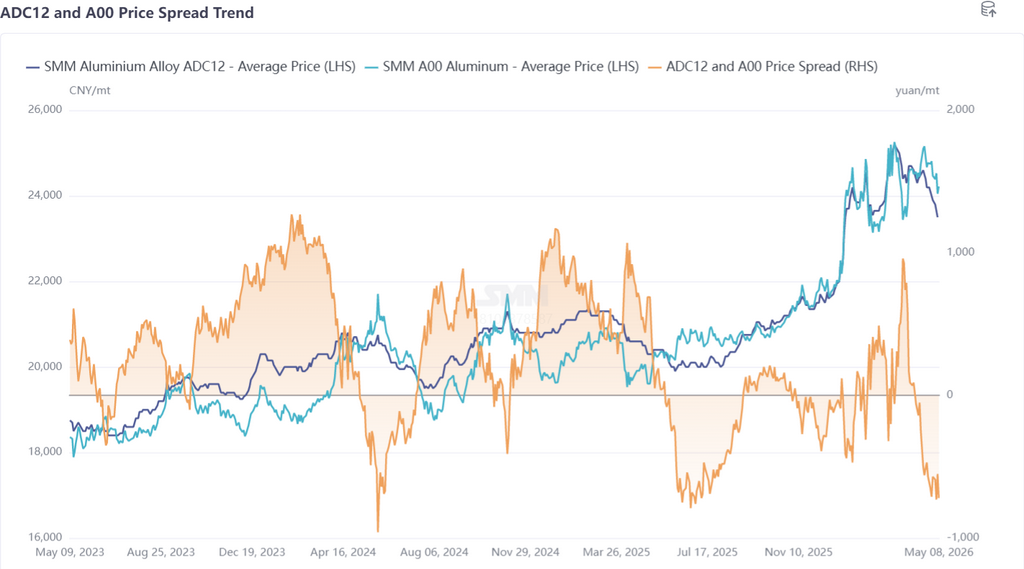

Pertama, tinjauan tren harga paduan aluminium sekunder pada bulan April: Di sisi futures, kontrak paduan aluminium cor yang paling aktif diperdagangkan terlebih dahulu turun kemudian naik pada bulan April, mencapai titik tertinggi 24.250 yuan/mt, sebelum berbalik menjadi tren penurunan berkelanjutan setelah pertengahan bulan. Setelah memasuki Mei, penurunan menyempit, dan kontrak berada dalam kondisi lesu di sekitar 23.000 yuan/mt. Di sisi spot, harga ADC12 secara keseluruhan berada di bawah tekanan pada bulan April, dengan momentum kenaikan memudar di awal bulan dan penurunan melebar setelah pertengahan bulan. Per 8 Mei, SMM ADC12 dikutip pada 23.500 yuan/mt, turun kumulatif 1.200 yuan/mt dari awal April.

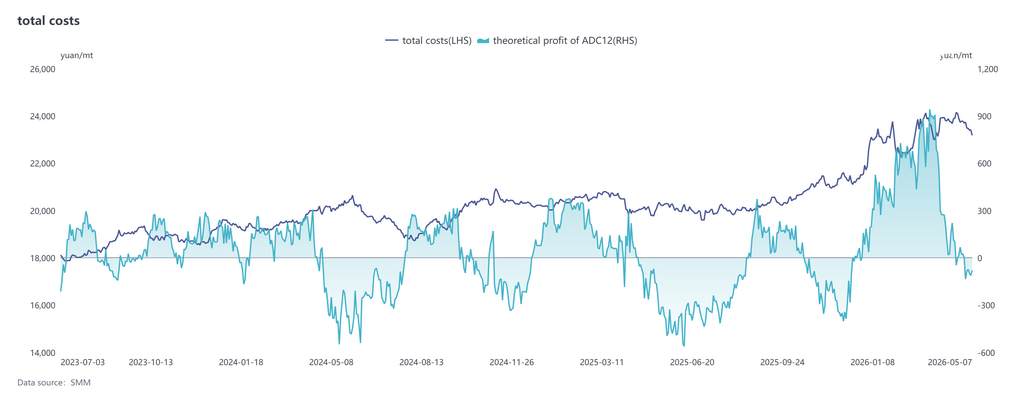

Sisi biaya, menurut data SMM terbaru, total biaya teoritis industri ADC12 naik menjadi 23.787 yuan/mt pada bulan April, sedikit meningkat MoM dari Maret, tetapi kenaikannya menyempit dibandingkan bulan sebelumnya. Dari segi komposisi biaya, skrap aluminium tetap menjadi komponen biaya dominan, dengan biaya per mt naik menjadi 21.569 yuan, dan porsinya sedikit naik menjadi 90,7%; biaya tembaga meningkat sedikit menjadi 835 yuan/mt, dengan porsi tetap di 3,5%; biaya silikon turun sedikit menjadi 478 yuan/mt, dengan porsinya menyusut menjadi 2,0%. Setelah memasuki Mei, harga ADC12 terus menurun, sementara harga skrap aluminium hanya turun sedikit. Laba teoritis industri bergeser dari untung menjadi rugi, dan tekanan operasional perusahaan semakin terasa.

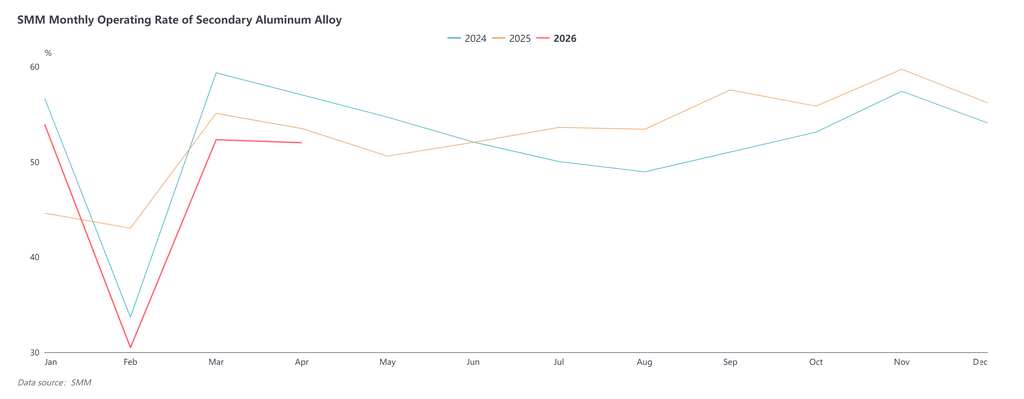

Pada bulan April, tingkat utilisasi industri paduan aluminium sekunder adalah 52,0%, turun tipis 0,3 poin persentase MoM dan turun 1,5 poin persentase YoY, dengan divergensi yang signifikan antar perusahaan. Tingkat utilisasi yang relatif stabil terutama disebabkan oleh: penurunan harga ADC12 yang merangsang kembalinya sebagian pesanan; peningkatan keuntungan ekspor yang mengimbangi pengurangan volume domestik; dan pedagang yang membeli di harga rendah untuk mengisi sebagian celah pesanan. Namun, pemangkasan produksi juga meluas, terutama karena konsumsi yang tidak sesuai ekspektasi, kesulitan dalam pengadaan bahan baku yang memenuhi syarat, dan pembatasan faktur balik, yang memaksa beberapa perusahaan untuk secara pasif mengurangi output. Secara keseluruhan, tingkat utilisasi pada bulan April turun tipis dalam kisaran sempit. Pada bulan Mei, permintaan melanjutkan tren pelemahan yang dimulai sejak pertengahan April, dengan keinginan restocking hilir tetap lemah dan sentimen wait-and-see mendominasi. Berkurangnya pesanan selama libur Hari Buruh membebani produksi, dan ruang pemulihan pasca-libur terbatas. Di bawah berbagai tekanan termasuk musim sepi permintaan, masalah bahan baku, dan masalah faktur, tingkat utilisasi pada bulan Mei masih memiliki ruang untuk penurunan lebih lanjut.

Secara keseluruhan, harga ADC12 pada bulan Mei diperkirakan akan terus dalam pola lesu kisaran sempit, tetapi ruang penurunan relatif terbatas. Di sisi tekanan, permintaan pengguna akhir tetap lemah secara persisten, stok sosial dan stok di pabrik tetap tinggi, fundamental tidak memiliki pendorong positif yang substantif, dan momentum kenaikan harga tidak memadai. Di sisi penopang, biaya bahan baku yang tetap tinggi seperti skrap aluminium, dikombinasikan dengan berkurangnya impor skrap aluminium, memberikan dukungan lantai tertentu bagi harga spot, dan perusahaan memiliki keinginan terbatas untuk memangkas harga secara signifikan. Singkatnya, harga ADC12 pada bulan Mei diperkirakan terutama berfluktuasi turun dalam kisaran sempit. Ke depan, perhatian utama harus diberikan pada dampak transmisi konflik geopolitik Timur Tengah terhadap harga aluminium, perubahan marjinal dalam permintaan pengguna akhir, dan kondisi pasokan skrap aluminium.

![Divergensi Pasar Ingot Aluminium Luar Negeri: Pasar AS Kuat, Sementara Jepang dan Thailand Lemah [Analisis SMM]](https://imgqn.smm.cn/usercenter/kVTpA20251217171654.jpg)