Harga acuan futures baja tahan karat China melonjak ke level tertinggi sejak 2023 pada pekan perdagangan terakhir sebelum libur Hari Buruh, didorong oleh serangkaian gangguan pasokan bahan baku utama. Namun reli ini belum mendapat dukungan meyakinkan dari permintaan fisik, sehingga berpotensi menciptakan volatilitas saat pasar dibuka kembali.

Kontrak baja tahan karat SHFE paling aktif (SS2606) ditutup pada sekitar $2.278/mt (RMB 15.585/mt) pada 30 April, naik sekitar $61/mt (RMB 420/mt) selama sepekan. Pergerakan ini hampir sepenuhnya didorong oleh faktor tekanan biaya — gangguan mendadak pada pasokan skrap dan pemangkasan produksi produsen nikel-kobalt besar — bukan perbaikan konsumsi hilir.

Latar belakang makro: domestik kuat, luar negeri hati-hati

Lingkungan makro menunjukkan gambaran beragam. Di sisi domestik, Biro Statistik Nasional China melaporkan laba perusahaan industri berskala besar naik 15,5% year-on-year pada kuartal pertama, memperkuat narasi pemulihan manufaktur yang tangguh. Data penerimaan pajak dari Kementerian Keuangan menggemakan nada serupa.

Di luar negeri, gambaran kurang mendukung. Federal Reserve AS mempertahankan suku bunga seperti yang diharapkan, tetapi perbedaan pendapat hawkish dari tiga anggota voting — menandakan penolakan terhadap pemangkasan jangka pendek — dan ketidakpastian geopolitik yang berlanjut membebani valuasi forward komoditas secara luas. Namun untuk saat ini, narasi sisi pasokan domestik China mengungguli hambatan eksternal.

Reli futures melampaui pasar fisik

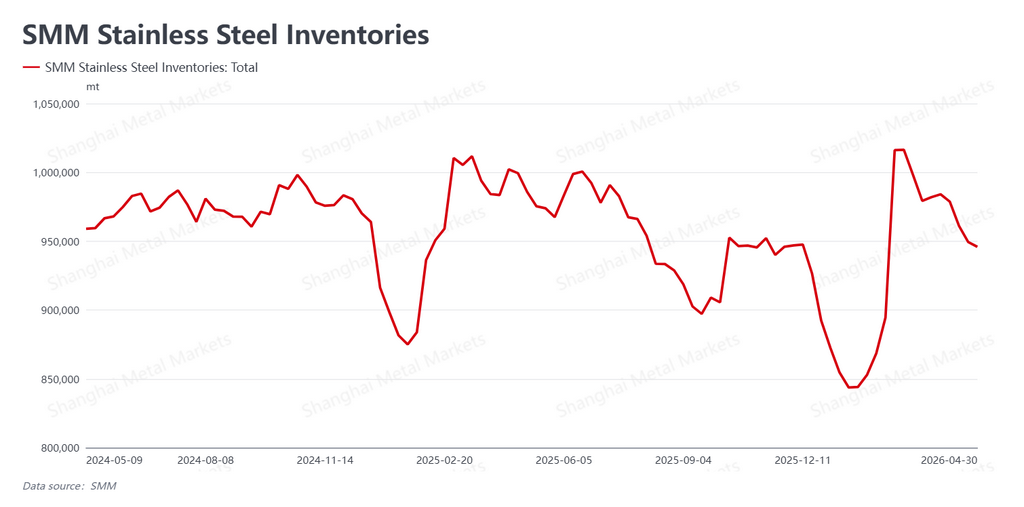

Meskipun pergerakan kuat di papan futures, pasar spot menunjukkan cerita yang lebih hati-hati. Menurut SMM (Shanghai Metals Market), total inventaris pasar turun tipis menjadi 945.900 mt pekan ini, penurunan moderat 3.500 mt. Destocking berlanjut, tetapi dengan laju yang lambat.

Lebih penting lagi, transaksi fisik lemah. Harga futures bergerak terlalu cepat untuk diikuti spot, dan dengan melebarnya selisih harga, pembeli hilir sebagian besar memilih menunggu di pinggir. Selain lonjakan pembelian singkat di awal pekan, volume transaksi memudar. Operasi pemrosesan — slitting, leveling, dan pusat layanan lainnya — melaporkan bisnis yang lesu, tanpa tanda restocking pra-libur yang biasanya menjadi ciri akhir April. Likuiditas spot yang ada sebagian besar didorong oleh arbitrase basis-trade daripada permintaan pengguna akhir yang sesungguhnya.

Singkatnya, futures telah memperhitungkan narasi bullish bahan baku yang belum divalidasi oleh pasar fisik.

Pendorong utama: guncangan pasokan bahan baku

Pergerakan harga pekan ini ditopang oleh dua perkembangan di sisi biaya.

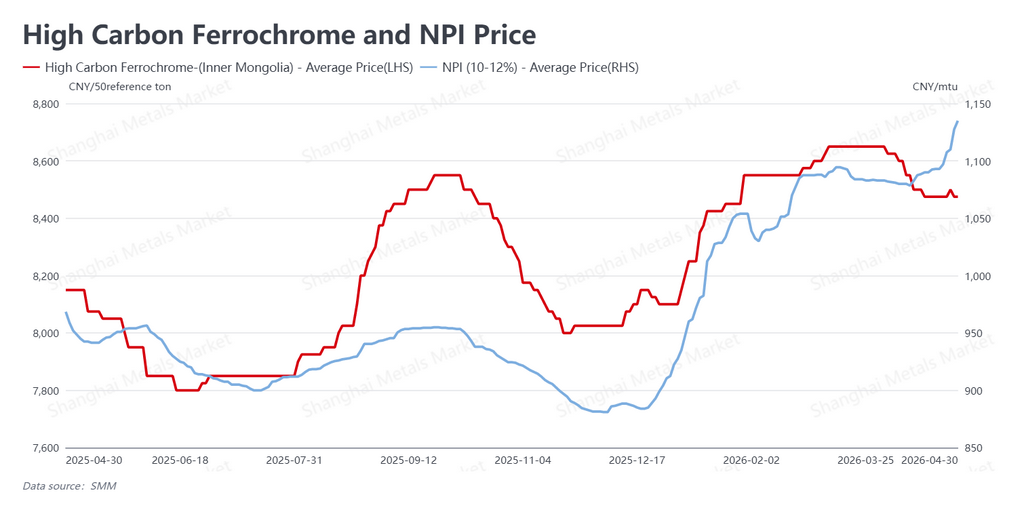

Pertama, pengetatan yang semakin dalam di pasar skrap baja tahan karat China. Kontrol kepatuhan faktur dan pajak yang lebih ketat pada transaksi skrap menimbulkan kekhawatiran jangka menengah-panjang tentang ketersediaan skrap, mendorong pabrik China meningkatkan ketergantungan pada Nickel Pig Iron (NPI) sebagai bahan baku pengganti.

Kedua — dan lebih berdampak langsung — produsen nikel-kobalt terkemuka China mengumumkan penghentian produksi sementara pada sebagian operasinya mulai 1 Mei, dengan alasan kenaikan biaya bahan pembantu dan tekanan tingkat utilisasi tinggi yang berkelanjutan. Penghentian ini diperkirakan mempengaruhi sekitar 50% output perusahaan. Ini mengirimkan sinyal kontraksi pasokan yang jelas melalui kompleks bahan baku.

Sebagai respons, penawaran NPI naik menjadi sekitar $166 per poin nikel (RMB 1.135/poin Ni) selama sepekan. Ferrochrome karbon tinggi bertahan stabil di sekitar $1.239 per 50 base ton (RMB 8.475/50 base ton). Pergeseran naik pada lantai biaya memberikan jangkar fundamental bagi reli futures, meskipun permintaan spot tertinggal.

Prospek: ekspektasi biaya vs. realitas permintaan

Pasar baja tahan karat China menutup "April Perak" yang secara tradisional kuat dengan nada kokoh, ditopang oleh konvergensi kendala pasokan skrap dan pemangkasan produksi di pemain hulu utama. Bersama-sama, faktor-faktor ini telah mengangkat ekspektasi biaya jangka pendek secara signifikan.

Namun ketidaksesuaian antara harga futures yang tinggi dan permintaan spot yang lesu menciptakan ketegangan yang perlu diselesaikan. Saat perdagangan dilanjutkan setelah libur Hari Buruh, pasar menghadapi ujian langsung: dapatkah pembeli fisik menyerap material pada level harga yang lebih tinggi ini, atau akankah kurangnya tindak lanjut hilir memaksa koreksi?

Bagi pelaku industri, risiko utama memasuki Mei adalah volatilitas harga yang tinggi pada level saat ini. Perhatian ketat harus diberikan pada seberapa cepat — atau lambat — pengguna akhir mulai berinteraksi dengan material berharga lebih tinggi di pasar fisik. Hingga itu terjadi, reli ini tetap merupakan pergerakan yang didorong biaya yang mencari konfirmasi dari sisi permintaan.

Ditulis oleh Bruce Chew

Analis Nikel & Baja Tahan Karat, Shanghai Metals Market

Email: bruce.chew@metal.com

Tel: +601167087088