High copper prices, ample supply, weak demand, inventory buildup, weak structure

↓

Falling copper prices, still ample supply, good demand, destocking, slightly stronger structure

↓

Fluctuating copper prices, relatively tight supply, demand fluctuating with copper prices, high probability of destocking, high probability of strengthening structure

Q1 2026 has ended, and April trading days are also about to end. The above two sentences summarize SHFE copper futures and spot market performance. Note that this refers only to copper cathode supply, as China saw significant production increases in 2025. Despite continued ore tightness, production in 2026 has also remained fluctuating at highs, keeping copper cathode supply persistently ample. Demand side, although annual demand showed growth, when broken down to monthly or even daily levels, demand was significantly influenced by copper prices. Amid copper price fluctuations, secondary copper was the "active player" — when copper prices were high, secondary copper shipments increased, benefiting both supply and demand sides; when copper prices fell, secondary copper shipments decreased, reducing some raw material supply for both supply and demand.

So recently the spot market appeared to have tight supply. Smelters began shifting to "high prices with high volumes" in shipments. Against the backdrop of continued destocking and concentrated smelter maintenance, can premiums "heat up"?

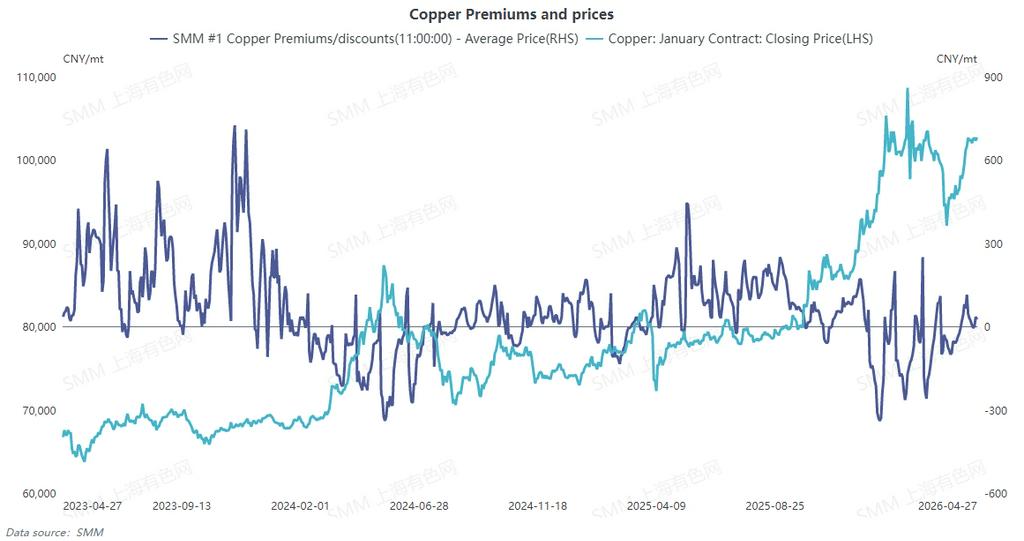

The chart above shows that from a macro perspective, copper prices and Shanghai spot copper premiums exhibited a clear inverse correlation in recent years. However, from a detailed perspective, Shanghai spot copper premiums have recently shown signs of "picking up" under high copper prices.

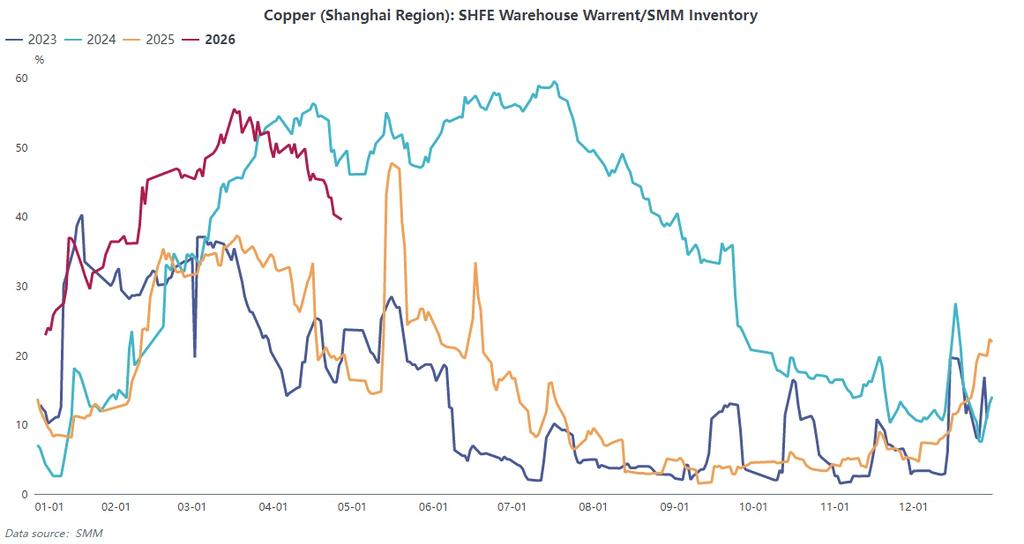

1. Although inventory continued destocking, the current warrant-to-inventory ratio remained elevated (this indicator is highly correlated with structure). The SHFE copper near-month structure has not shown a sustained backwardation structure to provide guidance for future premiums.

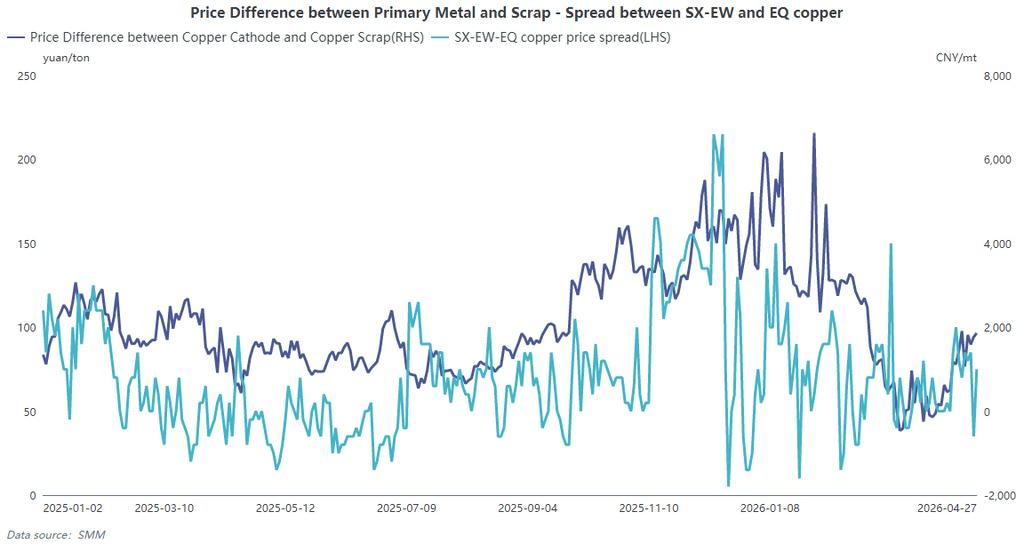

2. Although copper prices returned to highs, overall secondary copper shipment sentiment remained subdued, providing limited supplementation to copper cathode production and consumption. Previously, the price difference between primary metal and scrap was inverted, which favored copper cathode consumption. During this process, non-registered supply supplementation was limited, and the price spread between non-registered and SX-EW copper also narrowed. Imported copper supplementation within the year decreased YoY compared to previous years. Taking DRC as an example, non-registered supply was also diverted. Overall, substitutes for registered copper cathode decreased.

3. Copper cathode supply itself is about to decrease in the coming months, with concentrated maintenance currently underway in the market. Social inventory is expected to further decline.

As inventory decreases and the warrant-to-inventory ratio declines, the far-month structure has already shifted to backwardation. China's spot premiums are also expected to pick up in the near term. It has been observed that Guangdong spot premiums have been consistently higher than other regions nationwide for several consecutive days. Downstream buyers in Jiangsu, Zhejiang, Shanghai, and Anhui have recently tended to purchase from direct producers and traders with inventory who can issue invoices for the current month. Shanghai spot copper premiums are expected to see a small spike before the Labour Day holiday. After the holiday, as domestic supply decreases, premiums are expected to gradually firm up. However, the warrant-to-inventory ratio remains relatively high, and a sustained shift to backwardation in the structure still requires patience.