In 2025, the global NEV and new-type energy storage markets continued to surge. Chinese lithium battery enterprises, leveraging their technological expertise and scale advantages, continued to dominate the global supply chain. Recently, China's publicly listed lithium battery companies released their 2025 annual reports in a concentrated manner. Based on the collection and compilation of publicly available data, this report examines the production, shipments, and sales of China's lithium battery industry throughout 2025, providing insights into industry development trends.

The analysis selected publicly listed companies that disclosed specific battery cell production and sales data, including CATL, EVE, Gotion High-tech, Sunwoda, REPT Battero, and Zenergy. On one hand, these enterprises are highly representative of the industry, spanning from the absolute leader to strong emerging players. On the other hand, this is a period when publicly listed firms are intensively releasing their 2025 annual reports and Q1 2026 quarterly reports, making these companies' data the most up-to-date and reliable, accurately reflecting the current state of the industry. Additionally, some other publicly listed lithium battery companies only disclosed financial revenue figures in their annual reports without publishing specific physical production and sales data in capacity (GWh) or energy (Ah). To ensure the accuracy and comparability of the report's data dimensions, we specifically selected these enterprises that publicly and transparently disclosed their specific production and sales capacity data.

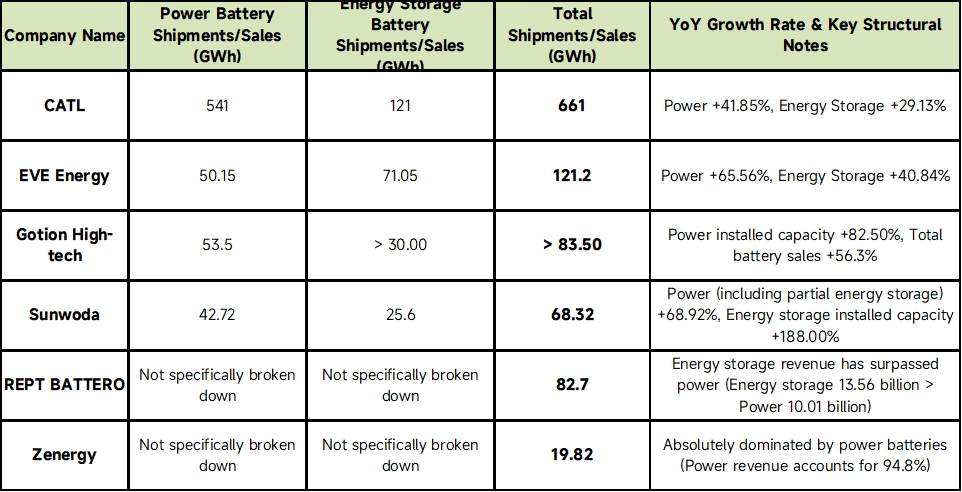

I. Overview of 2025 Production and Sales Data of Core Lithium Battery Enterprises

The following data was collected and compiled from the publicly released annual reports of each enterprise:

(Data source: Annual reports of respective companies)

(Note: REPT Battero and Zenergy did not break down specific EV and ESS physical volumes in GWh in their annual reports, but their distinctly different strategic focuses can be clearly identified from total sales and revenue structures.)

II. Industry Summary and Future Outlook

Based on the above annual report data and the current macro backdrop of China's lithium battery industry, the following market development trends are identified for 2025 and beyond:

1 Strong sales and production, energy storage becoming a parallel main battlefield

In 2025, production and sales data of China's mainstream lithium battery enterprises all showed double-digit or even triple-digit YoY high growth (e.g., Gotion High-tech power battery +82.5%, Sunwoda energy storage +188%). Overall, the industry's "dual-engine" structure has fully taken shape: NEVs hold the fundamental base, while ESS batteries have transformed from a "side business" into a core business pillar for multiple enterprises (e.g., EVE, REPT Battero). Production volumes slightly exceeded sales volumes across companies, maintaining a healthy inventory turnover state, reflecting strong confidence in future demand.

2 Technology development: large capacity and high C-rate becoming mainstream

Behind the surge in production and sales, technology iteration is the core driver.

Power battery: High C-rate fast charging batteries (e.g., 4C/5C ultra-fast charging), high energy density solutions, and dedicated batteries for PHEV/range-extended car models are thriving; meanwhile, enterprises are accelerating deployment toward semi-solid/all-solid-state battery and other frontier technologies.

ESS battery: Battery cell capacity is evolving toward larger sizes (e.g., 314Ah, 588Ah or even higher), pursuing longer cycle life (over 15,000 cycles) and higher system energy efficiency to reduce levelized cost of energy (LCOE) over the full life cycle.

3 Price and market competition intensifying: volume compensating for price, scale-driven cost reduction

Although the above enterprises achieved explosive growth in production and sales volumes, the industry generally faces brutal "price wars" and cost reduction pressure. After upstream lithium carbonate and other raw material prices pulled back, battery cell per-watt-hour prices in 2025 are basically at historical low ranges. Against this backdrop, the core survival logic for enterprises has shifted to "volume compensating for price" and "scale-driven cost reduction." Giants like CATL maintain profit margins through supply chain advantages, while other enterprises offset the risk of price declines through shipments growth rates of over 50%.

![[Lithium Battery: Wanrun New Energy Adjusts Repurchase Plan For 100,000-Ton Cathode Material Project]](https://imgqn.smm.cn/usercenter/JSjkr20251217171728.jpg)