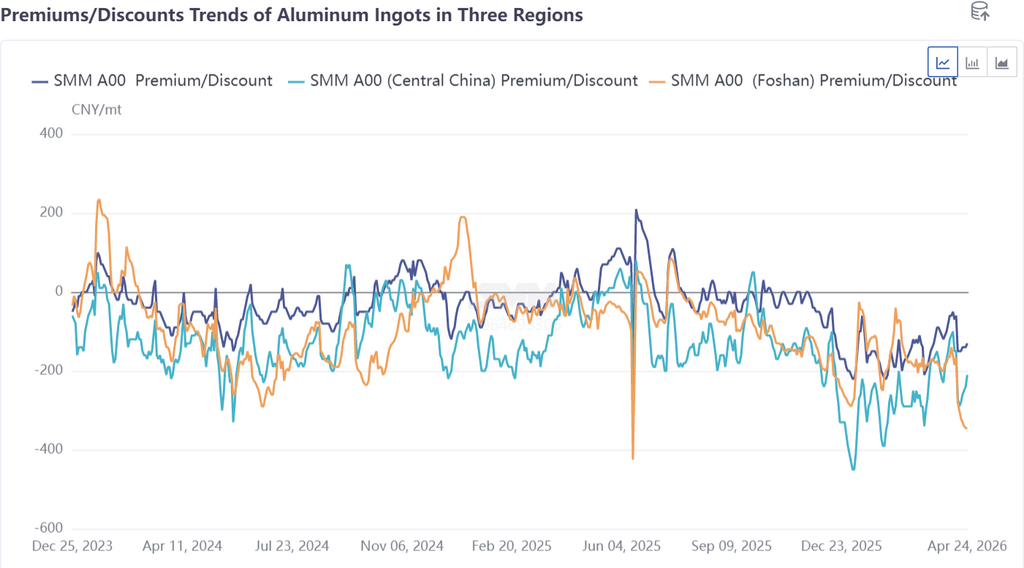

As regional inventory divergence intensified, the spot price spread between south China and east China continued to widen, and the price conditions for cross-regional cargo flows have preliminarily taken shape. As of April 24, mainstream prices in the south China market — SMM A00 aluminum (Foshan) — were at a discount of 345 yuan/mt against the 2605 contract, while mainstream prices in the east China market — SMM A00 aluminum — were at a discount of 130 yuan/mt against the 2605 contract. The price spread between the two regions exceeded 200 yuan/mt, covering shipping, short-haul transport, and logistics costs, officially opening up the transfer window between Guangdong and Shanghai.

This week, end-users in the east China aluminum market largely maintained just-in-time procurement. Ahead of the Labour Day holiday, downstream players and traders stockpiled in advance, boosting market trading activity. After aluminum prices plunged from highs and then rebounded, downstream willingness to restock on dips was moderate, driving warehouse withdrawals to rebound WoW. The spot market exhibited characteristics of "rigid demand underpinning, stockpiling warming up, and discounts narrowing." On the south China market front, spot trading sentiment remained extremely weak this week. As the impact of tax invoice reductions continued to ferment, risk-averse sentiment in the market was strong. Even long-term contract execution experienced some fluctuations. Traders only maintained just-in-time procurement, and downstream enthusiasm toward falling aluminum prices was equally limited. The loose market circulation pattern remained unchanged, and the deep discount situation showed no signs of recovery for the time being.

From the perspective of cargo flow direction, some upstream producers in south-west China have already taken the lead in adjusting their shipping strategies, reducing deliveries to the Foshan area and redirecting cargo to the higher-priced east China market. However, the loose circulation pattern in the south China market remained unchanged, the impact of tax invoice reductions continued to ferment, traders' risk-averse sentiment was strong, long-term contract execution fluctuated, and downstream purchase willingness was weak, making it difficult to repair discounts in the short term. In contrast, the east China market saw stable end-user rigid demand, pre-holiday stockpiling demand kicked off, trading activity improved, spot discounts narrowed slightly, and the attractiveness to external cargo sources increased.

SMM believes that the widening Guangdong-Shanghai price spread is a direct reflection of regional supply-demand mismatch. Cross-regional transfers will gradually ease inventory pressure in south China and increase cargo options available in east China, but it will be difficult to change the high inventory pattern in both regions in the short term. In particular, inventory pressure and inventory buildup expectations in east China after the holiday remain strong. Going forward, continued attention should be paid to the sustainability of the price spread, logistics efficiency, and the intensity of upstream shipping adjustments. If the price spread stays high, the scale of cargo flows from south China to east China may further expand.

![[SMM Aluminum Flash News] India’s Leading Recycler CMR Green Technologies IPO Subscribed Over 127 Times](https://imgqn.smm.cn/usercenter/EVjRH20251217171653.jpg)

![[SMM Aluminum Flash News] India Emerges as a Key Global Aluminum Hub Beyond China](https://imgqn.smm.cn/usercenter/VTjoW20251217171653.jpg)

![[SMM Aluminum Flash News] Russian Aluminium Share in LME Warehouses Rises to 93% as Indian Stocks Exit](https://imgqn.smm.cn/usercenter/tXCfs20251217171653.jpg)