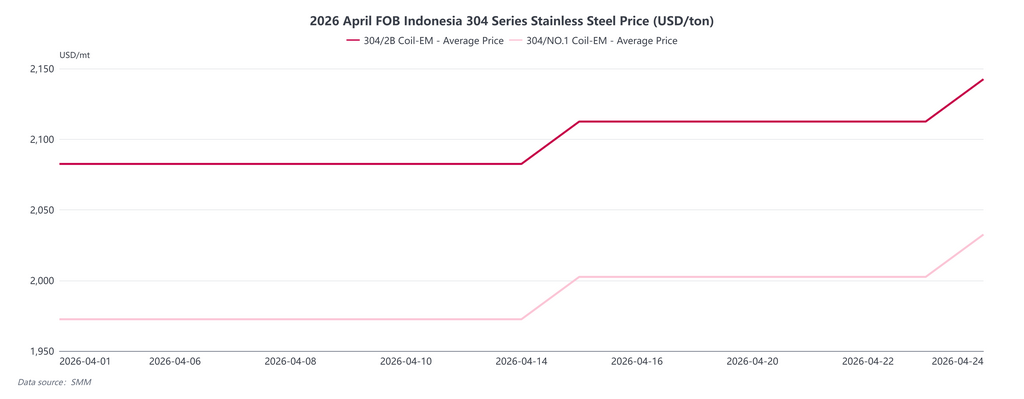

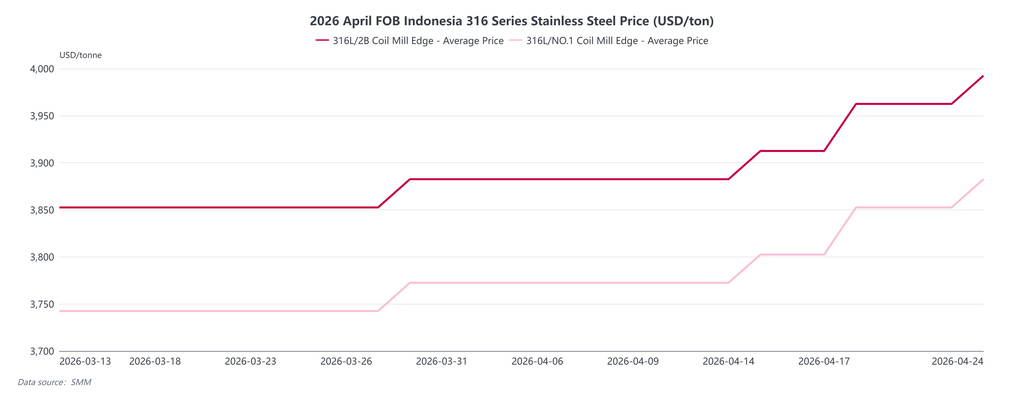

Based on SMM research, the week of April 20 to April 24, 2026, Indonesian stainless steel export prices followed a stable then surging trend. While quotations remained steady early in the week due to prevailing market caution, they collectively rose by USD30/mt by Friday (April 24). This increase was driven by rising nickel ore prices, which pushed NPI (Nickel Pig Iron) production costs higher, lifting FOB Indonesia 300-series prices. Notably, driven by rising global molybdenum costs, 316-series prices are now approaching the USD4,000/mt threshold.

Image 1: Review of FOB Indonesia 304 Stainless Steel Prices in April

Image 2: Review of FOB Indonesia 316 Stainless Steel Prices in April

The upward momentum in overseas stainless steel prices stems from structural tightening at the raw material end. The official implementation of Indonesia’s new Nickel Ore Pricing Formula (HPM), coupled with the announced suspension of operations for maintenance at a major Indonesian nickel mine starting in May, has caused an abrupt tightening of ore supply. This supply crunch is propagating down the value chain, supporting firm NPI quotations and directly inflating the immediate steelmaking costs for mills.

On the demand side, the Southeast Asian downstream market is currently in an inventory depletion phase. Upstream mills maintain a strong stance on pricing, pushing for further hikes toward the end of the week. Conversely, downstream buyers remain resistant to these high price levels, restricting procurement to hand-to-mouth replenishment. According to SMM research, local DDP 304 stainless steel cold-rolled coil (CRC) prices in Malaysia are currently ranging between RM 9.50 and RM 10.50/kg.

The European market has witnessed a slight trend of defensive restocking. The core driver is the impending expiry of the current EU TRQ (Tariff Rate Quota) on June 30. Starting July 1, the updated policy is expected to see quotas slashed by nearly half and potential tax rates doubled. To hedge against high tariff risks in the second half of the year, European traders have recently concentrated purchases on cargoes arriving before the end of June, triggering a counter-seasonal inventory buildup. SMM reports that local DDP 304 CRC prices in Europe are hovering between €2,700 and €2,900/mt.

Market activity in Taiwan, China remains relatively subdued, with buyers prioritizing the consumption of existing stocks and showing little appetite for restocking. Although upstream mills continue to raise April ex-factory prices, pushing local 304 CRC prices to a range of NT$ 69,300 to NT$ 74,000/mt, the wait-and-see sentiment among downstream buyers has overshadowed replenishment needs now that prices have hit historical highs, significantly limiting market liquidity.

Overall transaction dynamics this week reflect a stark imbalance between the upstream and downstream sectors. Upstream mills, driven by cost pressures, remain firm in their pricing strategies, while downstream buyers maintain a cautious stance, sticking to essential-only purchasing.

Given that May list prices have been released and mills remain resolute in their pricing, coupled with the pre-June 30 policy-driven hedging demand in Europe, overseas prices are expected to remain elevated in the short term. SMM anticipates that overseas stainless steel quotations will continue to fluctuate within a high-side range.

![[SMM Analysis] Post-Holiday Rebound Lifts China's Stainless Steel Futures, But Physical Market Tells a Cautious Story](https://imgqn.smm.cn/production/admin/votes/imagesrepls20260424190409.jpeg)

![[SMM Flash] Latest Market Update on Indonesian Sulfur](https://imgqn.smm.cn/usercenter/HfIIS20251217171709.jpg)