Recently, disruptions caused by the shutdown of the Strait of Hormuz have significantly driven up logistics and raw material costs across the copper smelting supply chain in the Democratic Republic of the Congo (DRC). Field research shows that the all-in logistics cost from hydrometallurgical plants in the DRC to the ports of Durban and Dar es Salaam currently stands at roughly US$270–330/t, with freight rates on some southbound routes rising by a further US$20–40/t from earlier levels. At the same time, sulfuric acid supply in the region remains tight. Ex-works sulfuric acid prices are currently around US$850/t, while delivered prices (DDP) have broadly risen to US$1,000–1,400/t. Sulfur prices have also remained elevated, with DAP quotations at around US$1,500–1,700/t and DDP quotations at around US$2,000–2,300/t. Under the dual squeeze of raw materials and logistics, operating pressure on local smelters has increased markedly.

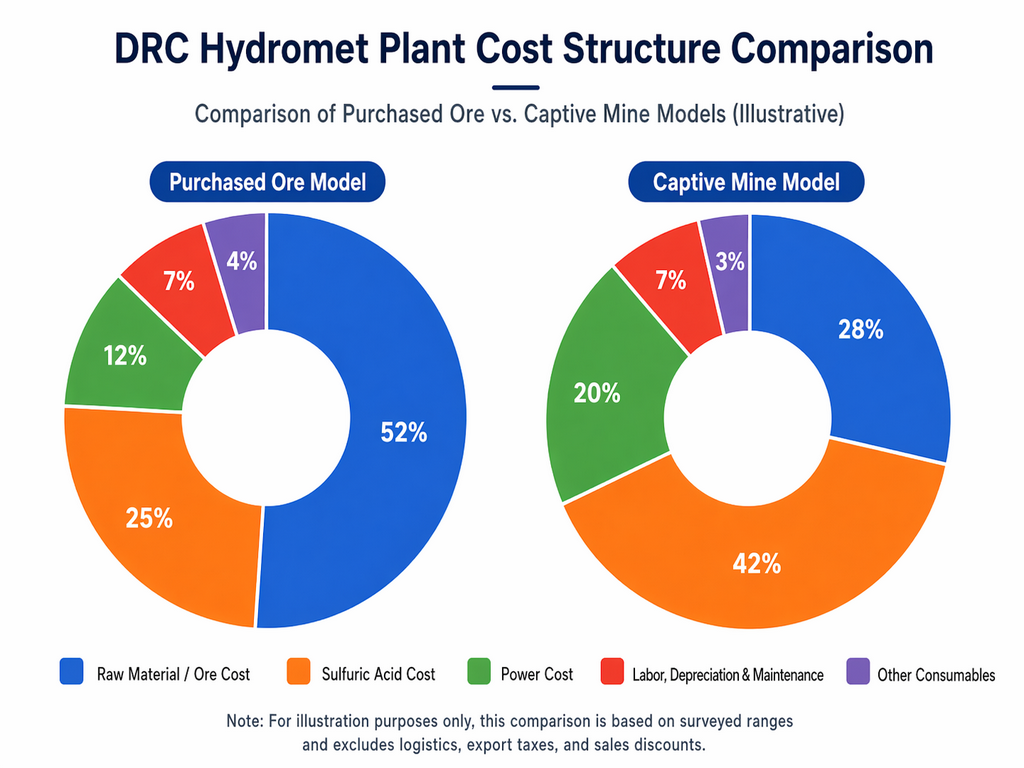

From a cost-structure perspective, the main pressures facing hydrometallurgical plants in the DRC are still concentrated in three areas: ore, sulfuric acid, and power. Based on the surveyed ranges, the cost of purchased ore is estimated at around US$6,000–7,000 per tonne of contained metal. Sulfuric acid consumption per tonne of copper generally falls within 2–5 tonnes, with the mainstream level around 3–4 tonnes. Power consumption per tonne of copper is roughly 2,600–3,500 kWh, with the mainstream range at about 2,600–3,000 kWh. Although some producers can still access grid power at a nominal US$0.10–0.14/kWh, unstable electricity supply means that actual marginal power costs rely more heavily on diesel generation and self-supplied power systems. Diesel-based power generation costs have generally risen to US$0.80–0.95/kWh, while diesel prices are mostly concentrated at US$3.1–3.4/litre. Against this backdrop, producers are broadly facing the real pressure of rising raw material costs and higher cash production costs.

However, based on the current findings of the survey, refined copper output in the DRC has not yet seen widespread production cuts or shutdowns. Most smelters reported that sulfur inventories are still at relatively safe levels, generally remaining above the three-week safety threshold, and are therefore not yet sufficient to disrupt continuous production in the short term. At the same time, earlier stockpiling of materials and in-house acid production capacity have, to some extent, offset the short-term impact of transport disruptions. As a result, the current situation is characterized more by rising costs and squeezed margins than by immediate large-scale production suspensions.

What deserves particular attention is that transport disruptions are now being transmitted into inventories. The survey indicates that both refined copper inventories at smelter sites and refined copper inventories at ports have begun to accumulate to varying degrees. On the one hand, lower transport efficiency has slowed shipment flows. On the other hand, the share of long-term contracts signed for 2026 has declined compared with previous periods, leaving smelters with more spot material available for sale, while downstream offtake capacity has been weaker than in prior years. Under the combined pressure of slower shipments and persistently high raw material prices, producers are generally facing greater pressure on collections and cash flow. As a result, some plants have gradually shifted their sales strategies away from a firmer pricing stance toward a stronger focus on destocking and cash recovery.

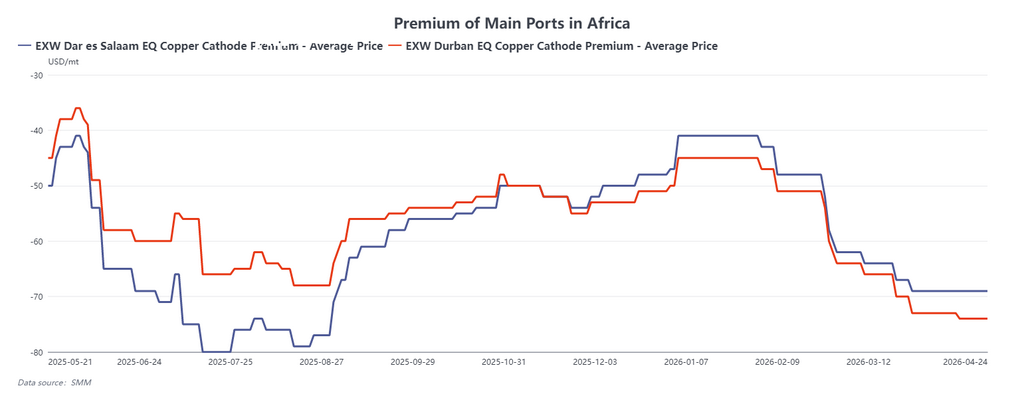

Against this backdrop, spot premiums for refined copper in the DRC have been on a downward trend since the end of the first quarter. At present, FCA tender prices at major smelters in the Kolwezi–Lubumbashi region have already fallen back to around US$-410/t, while some spot offers for small-lot cargoes have declined further to US$-440/t to US$-430/t. In addition, sellers have imposed special requirements in their offering terms regarding truck dispatch and cargo pick-up timing. Although the production side has not yet seen broad-based shutdowns or cuts, the build-up of spot material, rising selling pressure, and weaker willingness from buyers to accept high-priced cargoes have gradually shifted the market from an earlier tight balance to a phase of relative looseness. In other words, the dominant factor affecting spot premiums is no longer simply whether supply is being reduced, but increasingly the actual selling behavior driven by inventories, collections, and cash flow pressure. If disruptions in the Strait of Hormuz continue, logistics recovery falls short of expectations, and inventories at plant sites keep building, spot premiums for refined copper in the DRC may remain under further pressure.

Overall, the impact of the Strait of Hormuz shutdown on the copper smelting chain in the DRC is currently reflected in three main aspects. First, freight rates and sulfuric acid and sulfur prices have risen significantly, placing clear pressure on the cost side for producers. Second, output has remained broadly stable in the short term, with sulfur inventories still above the safety line, meaning that widespread shutdowns or production cuts have not yet been triggered. Third, transport disruptions, combined with a lower share of long-term contracts, have led to growing spot inventories and increased pressure on shipments and cash collections, which in turn has weighed on spot premiums for refined copper. Under a pattern of elevated costs and sales-side pressure, the operational focus of hydrometallurgical plants in the DRC may increasingly shift toward balancing inventory management, cash flow security, and raw material supply assurance.