Data Survei Tingkat Utilisasi Perusahaan Aluminium Sekunder Berdasarkan Wilayah dan Skala pada Maret 2026:

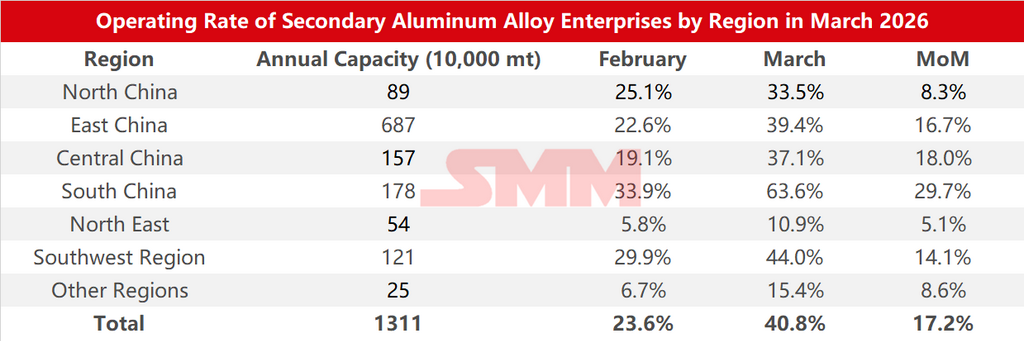

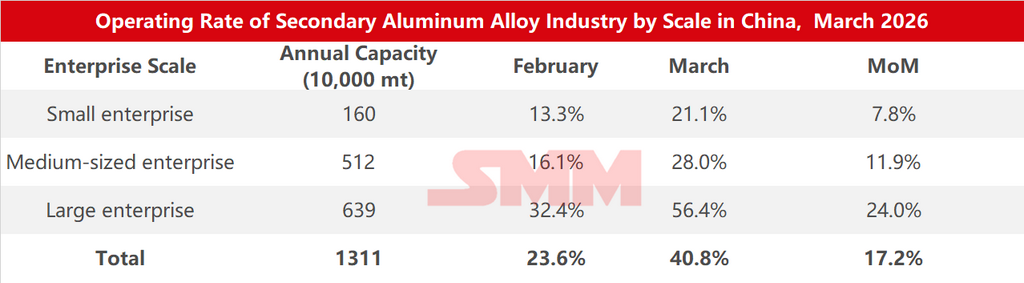

Menurut statistik survei SMM, tingkat utilisasi industri aluminium sekunder pada Maret 2026 mengalami rebound signifikan sebesar 17,2 poin persentase MoM dari Februari menjadi 40,8%, turun 2,1 poin persentase YoY. Tingkat utilisasi di seluruh wilayah pulih secara signifikan pada Maret. Perusahaan umumnya melanjutkan produksi setelah Festival Lampion, dan ditambah dengan pemulihan permintaan hilir secara bersamaan serta pemulihan berkelanjutan pesanan baru, tingkat utilisasi meningkat secara signifikan. Namun, rebound masih terkendala oleh berbagai faktor:

Dari sisi biaya, harga skrap aluminium berfluktuasi di level tinggi. Kebijakan faktur balik yang lebih ketat di Anhui dan wilayah lainnya, serta penghapusan rabat pajak di beberapa daerah, memaksa perusahaan beralih ke sumber daya berfaktur atau impor, sementara pasokan terkait tetap ketat dan harga tetap tinggi, sehingga menekan pelepasan tingkat utilisasi.

Dari sisi permintaan, pergeseran naik pusat harga aluminium pada Maret menekan margin hilir. Sebagian besar perusahaan melakukan pengadaan tepat waktu, dan beberapa secara aktif memangkas pesanan karena kerugian. Gangguan ekspor Timur Tengah dan meredanya subsidi otomotif juga membebani pengiriman. Menurut data CAAM, produksi dan penjualan otomotif pada Maret mencapai 2,917 juta unit dan 2,899 juta unit, masing-masing naik 74,4% dan 60,6% MoM, serta turun 3% dan 0,6% YoY. Produksi dan penjualan kendaraan energi baru (NEV) pada Maret mencapai 1,231 juta unit dan 1,252 juta unit, dengan produksi turun 3,6% YoY dan penjualan naik 1,2% YoY. Secara keseluruhan, produksi dan penjualan otomotif mengalami rebound signifikan MoM pada Maret tetapi sedikit menurun YoY, menunjukkan perbaikan dibandingkan dua bulan pertama. Di antaranya, pasar Tiongkok relatif lesu karena faktor-faktor seperti penyesuaian transisi kebijakan, permintaan yang ditarik ke depan, dan basis tinggi pada periode yang sama tahun lalu, dengan penurunan YoY dua digit. Melihat ke depan pada Q2, efek kebijakan program peningkatan peralatan berskala besar dan tukar tambah barang konsumsi diperkirakan akan terus terasa, mendorong konsumsi otomotif. Namun, perlu juga dicatat bahwa lingkungan eksternal saat ini kompleks dan bergejolak, risiko konflik geopolitik meningkat, harga bahan baku dan komponen utama berfluktuasi di level tinggi, tekanan operasional perusahaan semakin meningkat, momentum permintaan domestik tetap lemah, dan industri masih menghadapi tekanan yang cukup besar.

Pada bulan April, tekanan biaya kemungkinan tidak akan mereda dalam jangka pendek, dan kekuatan pemulihan permintaan penggunaan akhir masih belum pasti. Pesanan industri diperkirakan akan sedikit melemah, dan tingkat utilisasi diperkirakan akan sedikit menurun dari bulan Maret meskipun secara umum tetap stabil.

![Faktor Makro dan Geopolitik Bergema Selama Libur Hari Buruh, LME Mengungguli SHFE untuk Aluminium [Analisis SMM]](https://imgqn.smm.cn/usercenter/XfCZS20251217171655.jpg)

![[SMM Aluminum Flash News] DISA Luncurkan Lini Cetak C5 untuk Tingkatkan Efisiensi Pengecoran](https://imgqn.smm.cn/usercenter/iCOMR20251217171653.jpg)

![[SMM Aluminum Flash News] Korea Selatan Tingkatkan R&D UKM untuk Kurangi Paparan Karbon di Bawah Tekanan CBAM](https://imgqn.smm.cn/usercenter/EVjRH20251217171653.jpg)