After the Chinese New Year holiday, China’s aluminum market continued to see an inventory buildup, with social inventory rising लगातार and repeatedly hitting highs for recent years. However, as the traditional peak consumption season gradually got underway, downstream pickup enthusiasm rebounded, pressure from aluminum ingot backlogs eased significantly, and the pace of inventory buildup has already shown signs of slowing. Market expectations for an inventory inflection point in mid-to-late March have gradually strengthened.

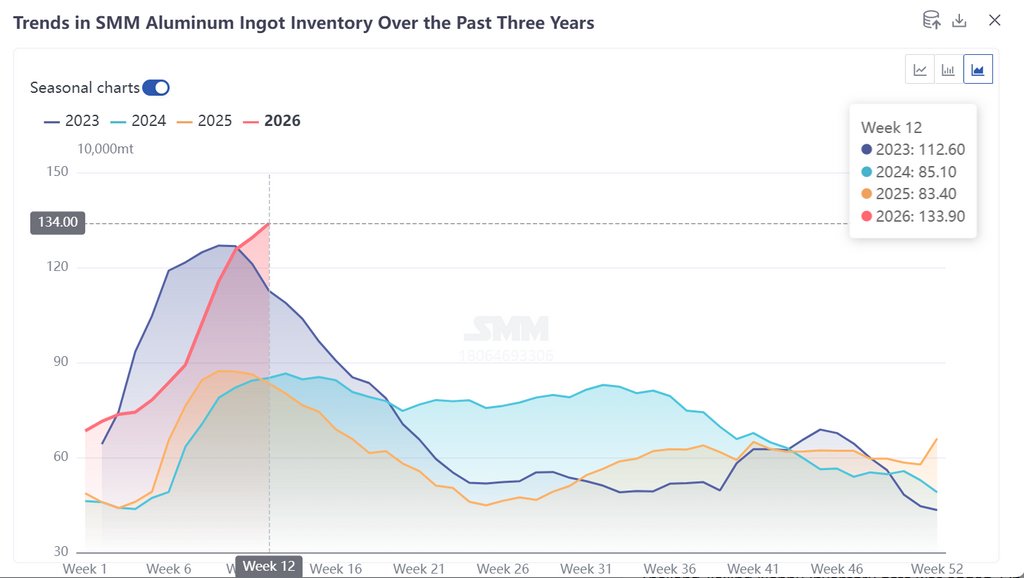

According to SMM statistics, as of March 19, aluminum ingot inventory in China’s major consumption regions stood at 1.339 million mt, up 45,000 mt from last Thursday. Current inventory levels remained in the upper range of the past five years. In terms of the pace of inventory buildup, although the overall rising trend has not changed, clear signs of easing emerged during the week, laying the groundwork for a subsequent inventory inflection point.

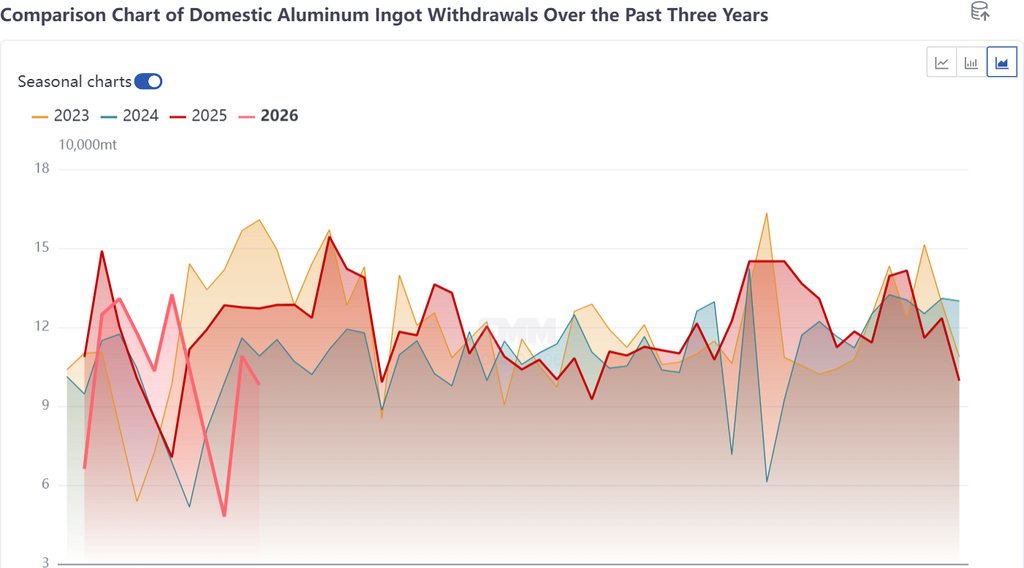

Demand recovery was the core driver behind easing inventory pressure. Before this year’s Chinese New Year, downstream industries showed relatively limited pre-holiday stockpiling. After the holiday, as enterprise operating rates steadily rebounded, end-user rigid-demand orders continued to be released, providing strong support for spot cargo warehouse withdrawals. In addition, as the traditional peak consumption season of “Golden March and Silver April” gradually deepened, purchase willingness among downstream processing enterprises recovered, and spot market trading was generally active, effectively offsetting incremental pressure from the upstream supply side.

From the perspective of regional inventory and cargo backlog conditions, after warehouse withdrawals increased, storage capacity was released, allowing backlogged cargo to be quickly moved into warehouses. As a result, overall pressure in mid-March improved significantly from the earlier period. Warehouses in east China still faced some inventory pressure, but backlog conditions had improved markedly, with current backlog volume at 20,000-30,000 mt (vs. 80,000-100,000 mt in early March). In south China, warehouse withdrawals strengthened notably, opening up room for concentrated warehousing of backlogged cargo. In Foshan, yard backlog volume fell sharply by 35,000 mt from early March to around 5,000 mt. In Gongyi, in-transit cargo volume remained normal, while the recovery in downstream operations drove an increase in pickup volume, keeping backlog volume stable at around 10,000 mt. Regional inventory circulation efficiency gradually improved.

Supply side, China’s aluminum casting ingot volume was expected to remain high in March, and the short-term trend of social inventory buildup will likely continue. The post-holiday inventory peak in this round is expected to reach 1.35-1.4 million mt, in line with previous expectations. However, positive factors in the market are gradually emerging. On the one hand, the overall backlog of aluminum products has already eased significantly, and problems related to sluggish inventory circulation have improved effectively. On the other hand, the pullback in aluminum prices benefited downstream purchasing and further boosted warehouse withdrawal enthusiasm in China’s major consumption regions.

Overall, the post-holiday inventory buildup cycle for aluminum has entered its final stage. As downstream demand continues to recover, spot trading remains active, and backlog pressure gradually eases, the momentum of inventory buildup is weakening continuously. Supported by rigid demand and reinforced by peak-season expectations, China’s aluminum social inventory is expected to reach a trend inflection point in late March. Going forward, continued attention should be paid to downstream operating loads, the pace of order release, and changes in spot trading to verify the strength of the inflection point.