SMM February 9:

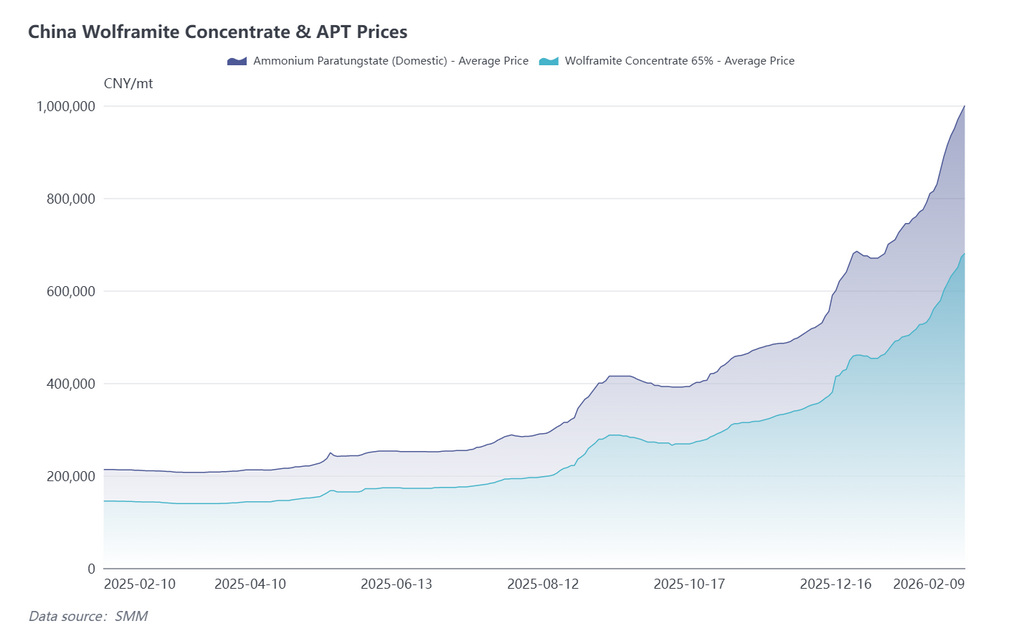

The tight supply situation in the raw material spot market continues to intensify, coupled with the holiday effect brought by the approaching Chinese New Year, the overall market is showing a pattern of "rising prices amid shrinking volume." Additionally, a major tungsten enterprise significantly raised its long-term contract prices, reigniting market bullish sentiment. On February 9, the average price of scheelite concentrate (≥65%) reached a record high of 680,500 yuan/metric ton, indicating a year-to-date increase of over 50%! The average price of APT (domestic) also rose to the historic milestone of 1 million yuan per metric ton on February 9, with a year-to-date increase of 49.25%!

Tungsten enterprise significantly raised its long-term contract purchase prices for the first half of February

Zhangyuan Tungsten Co., Ltd. of Chongyi's prices are as follows: 1. 55% scheelite concentrate: 670,000 yuan per metric ton, up 147,000 yuan per metric ton from the previous round; 2. 55% wolframite concentrate: 669,000 yuan per metric ton, up 147,000 yuan per metric ton from the previous round; 3. Ammonium paratungstate (standard grade zero): 970,000 yuan per metric ton, up 210,000 yuan per metric ton from the previous round.

The Ganzhou Tungsten Industry Association's forecast prices for the tungsten market in February 2026 are: 55% scheelite concentrate at 670,000 yuan per metric ton, up 300,000 yuan per metric ton MoM; APT at 970,000 yuan per metric ton, up 300,000 yuan per metric ton MoM; medium-grain tungsten powder at 1,630 yuan per kg, up 480 yuan per kg MoM. (Prices are for reference only; assume commercial risks accordingly.)

Furthermore, it is understood that some tungsten enterprises have suspended the publication of their long-term contract prices.

Average Price of Ammonium Paratungstate (Domestic) Rises to 1 Million Yuan per Metric Ton, Up Over 49% Year-to-Date

According to SMM price assessments, on February 9, the price range for scheelite concentrate (≥65%) was 680,000-681,000 yuan per metric ton, with an average price of 680,500 yuan per metric ton, up 1.19% from the previous trading day. Compared to the average price of 453,500 yuan per metric ton on December 31, 2025, this new high of 680,500 yuan per metric ton represents an increase of 227,000 yuan per metric ton year-to-date, a gain of 50.05%. Compared to the average price of 142,750 yuan per metric ton on December 31, 2024, the cumulative increase over more than a year reaches as high as 376.71%.

On February 9, the price range for ammonium paratungstate (domestic) was 990,000-1,010,000 yuan per metric ton, with an average price of 1,000,000 yuan per metric ton. Compared to the average price of 670,000 yuan per metric ton on December 31, 2025, this average of 1,000,000 yuan per metric ton represents a year-to-date increase of 49.25%, rising sharply in sync with scheelite concentrate.

Despite the continued sharp rise in tungsten prices, overall market trading activity has not kept pace recently, constrained mainly by multiple factors: First, with the Chinese New Year approaching, traders have become more cautious, focusing purchases on rigid demand, with only limited pre-holiday stockpiling and no large-scale concentrated stockpiling occurring. Second, high tungsten prices have led to both funding pressure and fear of high prices in the market, causing some downstream enterprises to postpone purchases and adopt a wait-and-see attitude. Third, the holiday effect is gradually becoming apparent, with some enterprises already entering a pre-holiday lull, leading to a general pullback in market trading frequency. The cemented carbide industry, a core demand sector for tungsten (accounting for 58% of total demand), is a typical example: affected by the soaring prices of raw materials like tungsten powder, production costs have increased significantly. Furthermore, tungsten materials like tungsten carbide account for over 80% of tool costs, forcing most cemented carbide enterprises to reduce procurement scale and maintain only production for rigid demand, further suppressing overall market trading activity.

Outlook

Looking ahead to the tungsten market outlook, in the short term, the tight spot supply situation on the raw material side is unlikely to ease quickly, and suppliers' reluctance to sell is expected to persist. The tungsten market is likely to maintain its strong upward trend. Key variables brought by the approaching Chinese New Year still require close attention: On one hand, market trading will gradually stagnate during the holiday period, and whether pre-holiday stockpiling demand concentrates will directly influence the short-term price movement pace. On the other hand, post-holiday enterprise work resumption progress, the recovery of raw material supply, and the strength of downstream demand release will determine whether tungsten prices can remain high. Additionally, international market price fluctuations, the signing of enterprise long-term contracts, industry policy direction, and the cost pass-through effect in the cemented carbide industry require continuous monitoring, while remaining vigilant against increased market risks from intensified price fluctuations in the high price range.