Berita SMM 11 Juli:

Pada semester pertama 2025, industri kimia fosfor mengalami fluktuasi harga dan penyesuaian kapasitas yang signifikan, terutama dipengaruhi oleh kondisi ekonomi global, pasokan bahan baku, dan meningkatnya permintaan energi baru. Di sisi permintaan, konsumsi sumber daya fosfor di sektor energi baru terus meningkat. Penggunaan asam fosfat dan MAP industri dalam industri bahan katoda LFP, serta fosfor kuning dalam LiPF6 (bahan baku elektrolit utama), mengalami peningkatan volume penggunaan yang cukup besar dibandingkan periode yang sama tahun lalu.

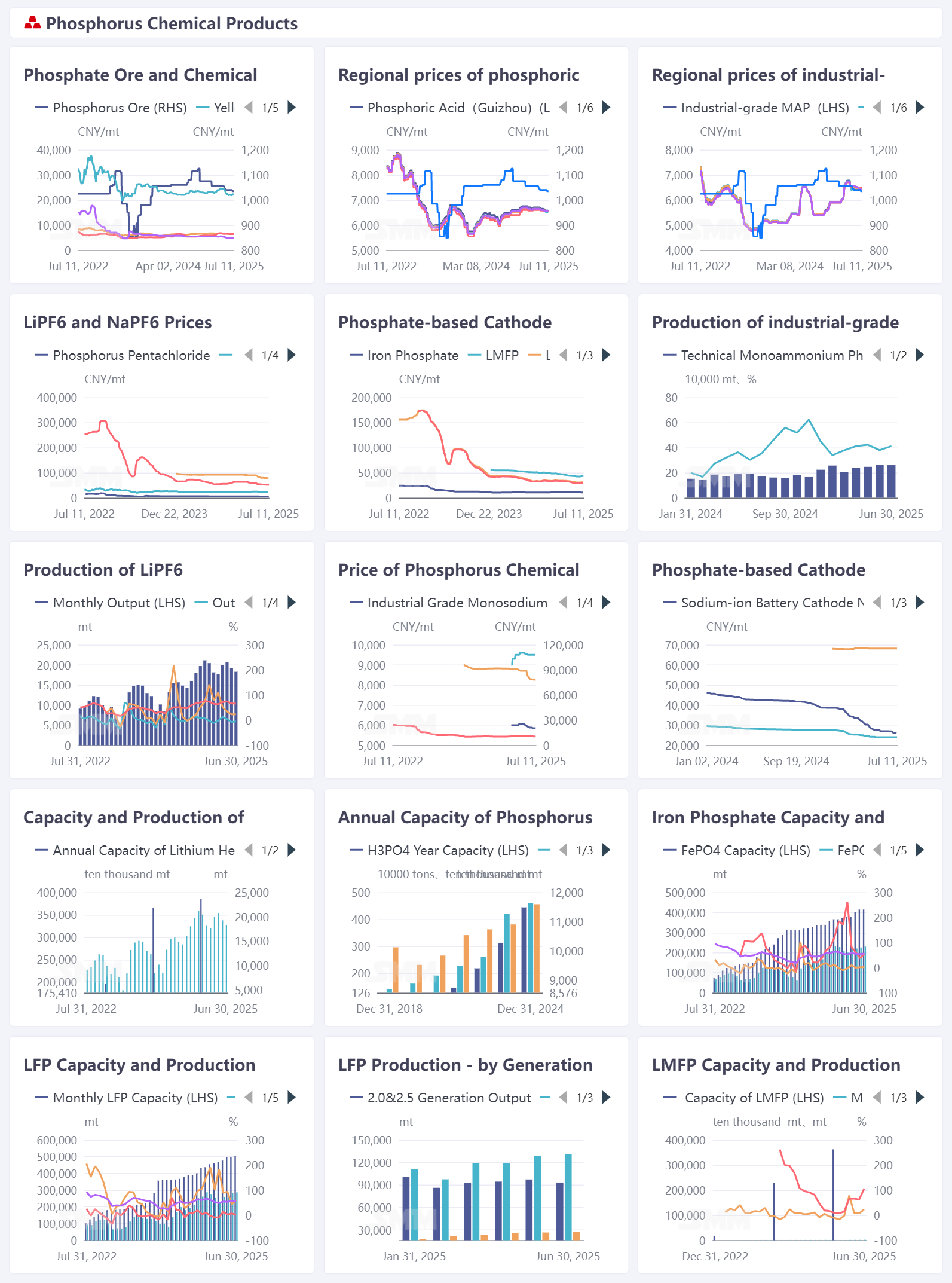

I. Tinjauan Harga Produk Kimia Fosfor

Pada semester pertama 2025, harga produk kimia fosfor menunjukkan tren yang berbeda. Harga bijih fosfat dan asam fosfat berfluktuasi di berbagai wilayah, mencerminkan perbedaan penawaran-permintaan regional. Pergerakan harga MAP industri dipengaruhi oleh permintaan dan biaya hilir, menunjukkan beberapa volatilitas. Harga produk seperti LiPF6 disesuaikan dengan pola penawaran-permintaan pasar, umumnya mencari keseimbangan dalam siklus industri, menunjukkan efek transmisi rantai industri energi baru.

Bijih fosfat: Harga awalnya naik kemudian turun. Harga awal tahun tinggi karena pasokan yang ketat tetapi kemudian menurun karena permintaan yang melemah. Harga bijih fosfat diperkirakan akan tetap tinggi sepanjang tahun, dengan penambang menikmati keuntungan yang kuat.

Asam fosfat: Perbedaan harga regional cukup besar, dengan harga keseluruhan stabil dengan tren menurun yang ringan pada semester pertama. Harga MAP industri menunjukkan fluktuasi musiman yang dipengaruhi oleh sektor pupuk musim panen pertanian, memuncak pada bulan Maret-April dan stabil dengan tren menurun pada bulan Mei-Juni.

II. Kapasitas di Bawah Dinamika Penawaran-Permintaan

Di sisi kapasitas, kapasitas sumber daya fosfor tahunan dan kapasitas khusus segmen seperti LFP terus berkembang, dengan perusahaan secara aktif menempatkan fasilitas produksi, secara bertahap mewujudkan efek skala industri. Data produksi menunjukkan variasi bertahap dalam output untuk produk seperti LiPF6 dan LFP, yang erat terkait dengan permintaan energi baru hilir (misalnya, baterai listrik, ESS), dengan output meningkat selama musim permintaan puncak, sementara juga dipengaruhi oleh pasokan bahan baku dan penjadwalan produksi.

Industri kimia fosfor sangat terintegrasi dengan rantai industri baterai lithium, mendukung sistem bahan baterai lithium mulai dari bahan katoda berbasis fosfor hingga elektrolit seperti LiPF6. Pergeseran dalam proporsi konsumsi produk seperti MAP kelas industri di sektor energi baru mencerminkan dorongan yang semakin besar dari industri energi baru terhadap bahan kimia fosfor, sementara fluktuasi harga bahan baku kimia fosfor berdampak secara terbalik pada biaya bahan baterai lithium dan pola persaingan pasar. III. Prospek untuk Paruh Kedua 2025

Di paruh pertama 2025, pasar produk kimia fosfor mengalami fluktuasi harga dan perubahan permintaan, tetapi mempertahankan tren pertumbuhan secara keseluruhan.

Dalam jangka pendek, perlu diperhatikan dorongan permintaan untuk produk kimia fosfor di paruh kedua 2025 (H2) yang didorong oleh musim puncak aplikasi energi baru di hilir (seperti musim puncak produksi dan penjualan NEV, serta pembangunan proyek penyimpanan energi yang terpusat), serta perubahan harga dan keuntungan yang dihasilkan oleh persaingan pasar yang semakin ketat setelah rilis kapasitas.

Dalam jangka panjang, dengan perkembangan terus-menerus industri energi baru, permintaan untuk bahan baterai lithium berbasis fosfor dengan kepadatan energi tinggi dan keamanan tinggi diperkirakan akan meningkat. Perusahaan kimia fosfor perlu fokus pada penelitian dan pengembangan teknologi (seperti mengoptimalkan kinerja bahan katoda berbasis fosfor) dan kolaborasi rantai industri (menstabilkan pasokan hulu dan hilir) untuk beradaptasi dengan peningkatan industri energi baru. Pada saat yang sama, mereka juga perlu mengatasi tantangan seperti kelebihan kapasitas dan persyaratan perlindungan lingkungan yang lebih ketat untuk mencapai pembangunan berkelanjutan.

![[Analisis SMM] Zimbabwe berencana menggunakan sumber daya alam sebagai jaminan, bekerja sama dengan China untuk memajukan proyek infrastruktur.](https://imgqn.smm.cn/usercenter/fblvS20251217171729.png)