》Check SMM copper quotes, data, and market analysis

》Subscribe to view historical spot prices of SMM metals

The mid-year negotiations between Antofagasta and smelters in China, Japan, and South Korea are approaching, with Antofagasta set to commence mid-year negotiations with smelters. Judging from the current situation, the outlook for buyers is not optimistic.

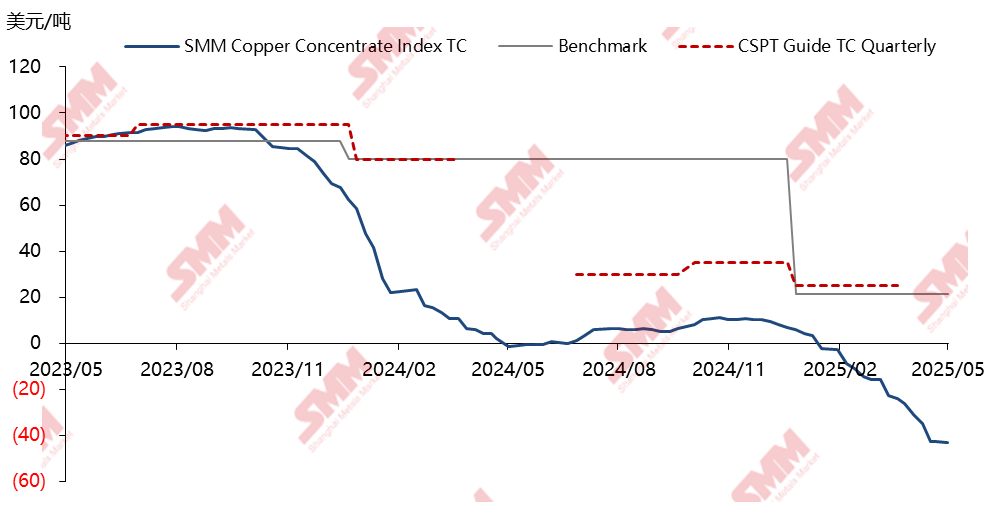

Firstly, it can be easily observed in the spot market that the sharp decline in TC is due to the surge in demand for copper concentrates from global copper smelters. Smelters have initiated a "resource battle," vying for limited spot resources at lower RC to secure cathode copper production. Since 2025, the spot market for copper concentrates has polarized, with active and concentrated procurement by top-tier smelters, while mid-tier and smaller smelters have adopted a more passive approach.

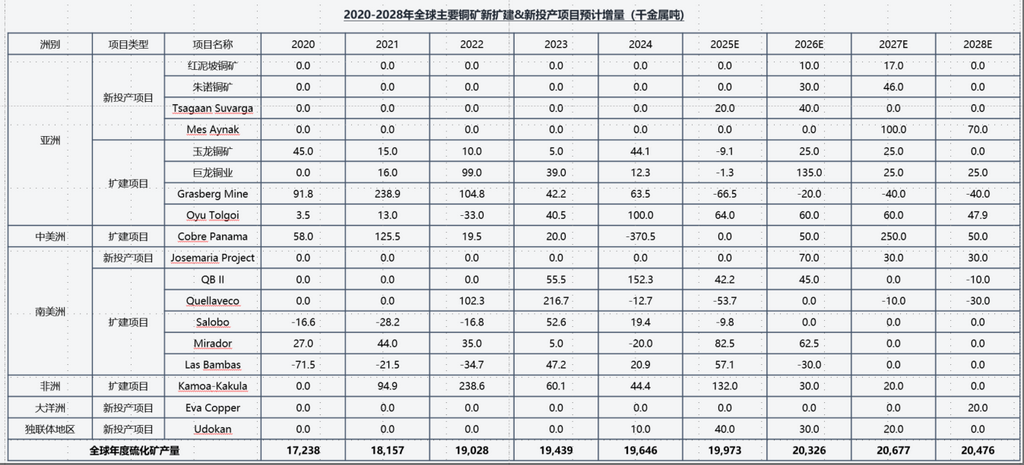

Secondly, from the fundamentals side, based on the production information disclosed by listed miners and combined with SMM's insights, the expected global sulfide ore production in 2025 falls short of expectations at 19.973 million mt in metal content, and the expected increase in sulfide ore supply in 2025 is also below expectations at only 327,000 mt in metal content.

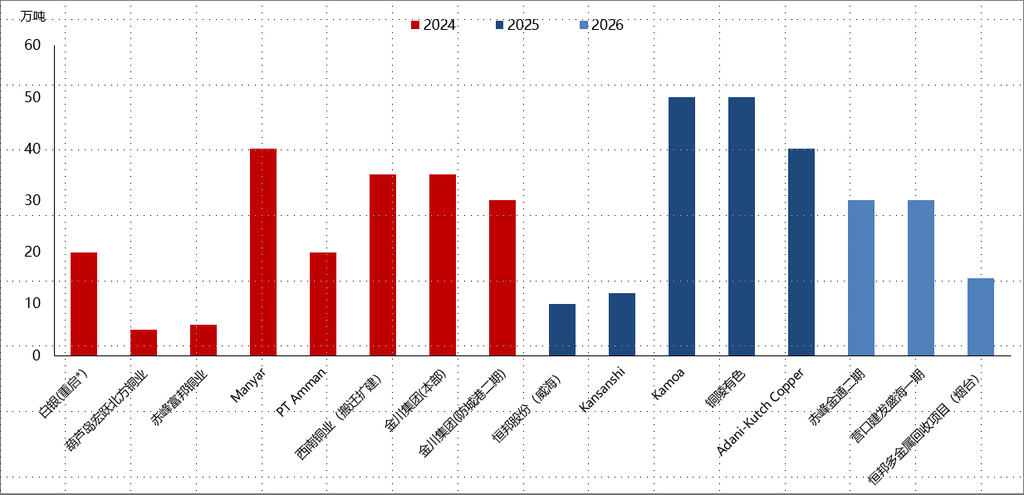

On the demand side, with the continuous advancement of smelter projects, the demand for copper concentrates continues to rise. As shown in the figure below, the global copper smelting capacity is expected to increase by a total of 4.28 million mt from 2024 to 2026. In addition, there are foreseeable copper smelting projects in the future, including Kunming Jinshui Copper Industry, Henan Jinli Gold and Lead Group Co., Ltd., Phase I of Hunan Yuneng, and Hubei Qiangxing New Material Technology Co., Ltd. Potential future copper smelting projects also include Zijin Mining's Ya'an Smelter, Minmetals Copper's Hunan Smelter, Kaz Minerals' new project, and the Russian Nickel Sino-foreign cooperative project, among others. It is evident that the future supply pressure on copper concentrates will be significant.

In summary, given the dire spot market conditions and the imbalanced supply-demand balance, SMM believes the following challenges will arise:

- The upcoming long-term contract negotiations will become more difficult. The mid-year negotiations between Antofagasta and smelters are set to commence at month-end, while BHP's spot tender will close on May 20. Miners are strategically "setting the tone," which will adversely affect the negotiations.

- The decline in spot TC for copper concentrates is difficult to curb, let alone reverse. Since May 2025, there has been a stabilization trend in spot TC for copper concentrates, with spot transaction TC for smelters/traders struggling to break through the midpoint of negative $40. Although there has been "bottom support" for TC recently, against the backdrop of an imbalanced supply-demand balance for copper concentrates, the continued deterioration of spot TC is only a matter of time.

- Production-oriented enterprises and international traders in the copper industry may encounter risk events. High raw material prices have led to a decline in the cost-effectiveness of raw materials and losses for production-oriented enterprises, further exacerbating corporate cash flow situations. The combination of an economic downturn cycle and a copper concentrates supply deficit cycle has exposed participants in China's copper concentrates market to the challenges of increased credit risks and operational risks.

》Click to view the SMM Copper Industry Chain Database

![BC Copper Retreated After Rapid Rise with Sharp Decline, Geopolitical and Data Under Pressure Narrowing Inversion [SMM BC Copper Commentary]](https://imgqn.smm.cn/usercenter/KytYP20251217171712.jpg)