》View SMM Silicon Product Prices

》Subscribe to View Historical Price Trends of SMM Metal Spot

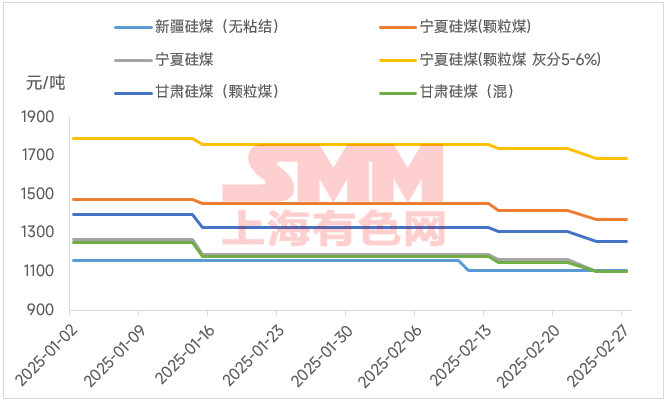

Recently, the price of silicon coal, a raw material for silicon metal, has continued to decline, with the most significant drops observed in Ningxia and Gansu. Currently, silicon coal prices have fallen to relatively low levels in recent years.

Based on the current market conditions for silicon metal, it can be seen that most silicon metal plants are still struggling below the cost line. The low silicon prices have also led to a lack of enthusiasm for production among silicon plants. The overall operating rate of the silicon metal industry remains at a low level, and under the influence of low operating rates, the demand for silicon coal as a raw material from silicon metal plants is naturally weak. Moreover, silicon coal in Ningxia relies heavily on demand from silicon plants in south-west China. Under the dual pressure of low silicon prices and high costs during the dry season, the overall operating rate of silicon metal plants in south-west China remains extremely low, resulting in minimal demand for silicon coal as a raw material.

In addition to the persistently weak demand, the cost support for silicon coal has also continued to weaken. The price of coking coal has been declining, and most silicon coal plants in Ningxia and Gansu use a combination of two types of coal for production. As coking coal prices fall and silicon coal demand remains weak, mine-mouth raw coal prices have been continuously adjusted downward, leading to a decline in silicon coal costs and a corresponding drop in silicon coal prices.

Since the beginning of 2025, silicon coal prices in many regions have been adjusted downward, with the most frequent and significant adjustments occurring in Ningxia. As of now, silicon coal prices in Ningxia have been reduced three times this year. Granular silicon coal prices have cumulatively decreased by 105 yuan/mt, with current prices ranging from 1,290 to 1,450 yuan/mt, while mixed coal prices have cumulatively decreased by 165 yuan/mt, with current prices ranging from 1,090 to 1,120 yuan/mt.

Although silicon coal prices have been reduced multiple times, the actual cost reduction for downstream silicon metal production has been minimal. Currently, the silicon coal primarily used in the all-coal process is non-caking silicon coal from Xinjiang, and its price has only decreased by 50 yuan since 2025, resulting in a cost reduction of less than 100 yuan for silicon metal production. For plants in north China using a coal-coke mixed process, petroleum coke prices have seen multiple increases since early 2025. Overall, the cost reduction driven by the decline in silicon coal prices is quite limited, and silicon metal plants are still facing significant production pressure.

![[SMM Iron & Steel] US Raw Steel Production Rises 8.8% YoY in Week Ending May 30, 2026](https://imgqn.smm.cn/usercenter/gmcdk20251217171720.jpg)