June 17

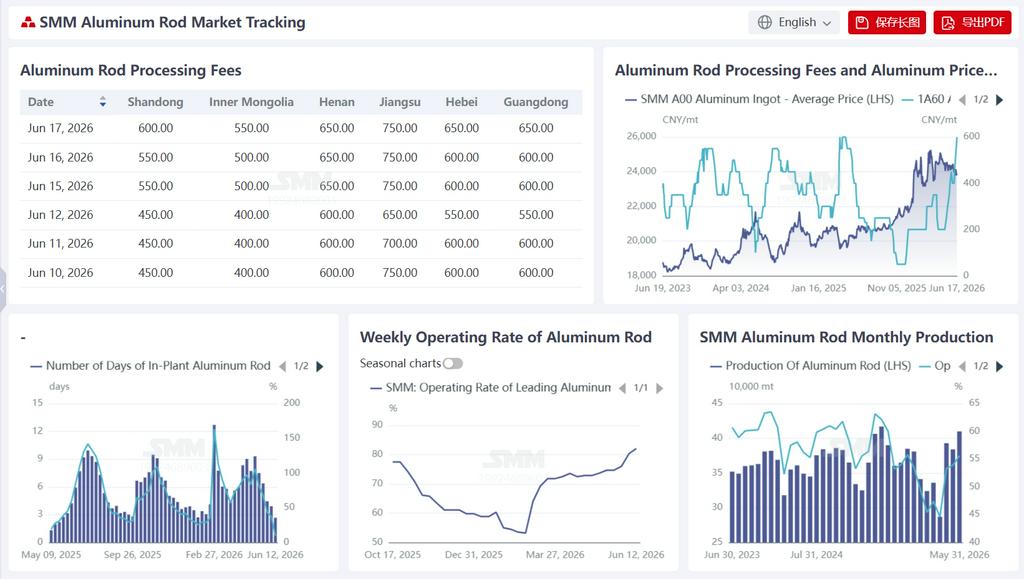

According to SMM statistics, as of June 12, in-factory inventory days for aluminum rod in China stood at 2.66 days, a sharp decline of 1.25 days WoW from 3.91 days on June 5, with the inventory ratio plunging from 37.45% to 9.28%, a drop of 28.17 percentage points. During the same period, the weekly operating rate of the aluminum wire and cable industry recorded 82.10%, up 1.76 percentage points WoW, climbing for the third consecutive week and staying at a high for the year. The rapid destocking was mainly driven by the resonance of sustained release of export orders for aluminum stranded wire and concentrated production schedules of State Grid orders, causing temporary tightness in aluminum rod supply. At the same time, the retreat in aluminum prices improved profit margins for previously won orders, prompting enterprises to voluntarily raise production loads and accelerate shipments, further speeding up inventory depletion. The strengthening operating rate was boosted by easing cost-side pressure, profit recovery on existing grid orders, and the sustained boost from high export prosperity. In the short term, inventory is expected to have further room for destocking, but the pace will gradually narrow; the operating rate will stay high, supported by both domestic and external demand, but attention should be paid to the risk of a retreat from highs if export orders show signs of marginal weakening.

During the week, aluminum prices broadly fluctuated downward in the doldrums, with the center shifting down about 200 yuan/mt from the start of the previous week, directly benefiting aluminum rod processing fees — lower aluminum prices reduce downstream procurement cost thresholds, repair profit margins for previously won low-priced orders, stimulate restocking and production willingness, and in turn push processing fees higher. As of June 16, aluminum rod processing fees were reported at 750 yuan/mt in Jiangsu, up 50 yuan/mt from last Tuesday (700 yuan/mt on June 9); 650 yuan/mt in Henan, up 100 yuan/mt from last Tuesday (550 yuan/mt); 550 yuan/mt in Shandong, up 100 yuan/mt from last Tuesday (450 yuan/mt); 500 yuan/mt in Inner Mongolia, up 100 yuan/mt from last Tuesday (400 yuan/mt); while both Hebei and Guangdong reported 600 yuan/mt, flat from last Tuesday. Behind the widespread increase in processing fees was continued tightness in aluminum rod supply, fueled by the dual boost from export orders and State Grid orders, with traders holding spot cargo and holding prices firm. In the near term, processing fees remain supported by high operating rates and low inventories, but caution is warranted over potential erosion of export order profits from LME aluminum weakness and a narrowing price spread between Chinese and overseas markets. If export enthusiasm cools, the rise in processing fees could face temporary pressure. This week, the operating rate of China's aluminum wire and cable industry recorded 82.10%, up 1.76 percentage points WoW. During the week, the industry's operating rate continued to strengthen, mainly because the recent decline in aluminum prices eased cost-side pressure on raw materials, and profit margins on power grid orders that enterprises had previously held improved marginally. This prompted manufacturers to proactively increase production loads, with capacity utilization rates edging up. In terms of orders, the third batch of material tenders for ultra-high voltage (UHV) projects was completed, with a total bidding volume of 19,400 mt for aluminum conductor steel reinforced (ACSR), and deliveries spanning from October 2026 to August 2027, providing some support for subsequent production schedules. Meanwhile, the list of winning bidders for the second batch of UHV materials was officially announced on June 8, resulting in 111,000 mt of conductor orders, further solidifying medium- to long-term order backlogs. Although domestic end-use demand for the power grid is currently in a lull after the concentrated cargo pick-up period, the decline in aluminum prices has spurred enterprises' willingness to produce against their existing orders, and coupled with export orders remaining high, the combined force of domestic and external demand has pushed the industry's operating rate up steadily. The domestic aluminum wire and cable operating rate is expected to hold up well in the short term.

![Active selling in the market; transactions far from ideal [SMM South China Spot Aluminum Daily Review]](https://imgqn.smm.cn/usercenter/uoPaX20251217171651.jpg)