SMM, June 11:

Entering June, the petroleum coke market broadly exhibited a pattern of initial decline followed by stabilization, with divergent trends among different varieties. Early in the month, low-sulphur petroleum coke prices were cut in a concentrated manner, intensifying bearish sentiment and generally softening prices across various specifications. In mid-June, domestic major and independent refineries added more maintenance units, causing a phase of contracted commercial volume of domestic petroleum coke. Tight supply lent support and briefly stabilized the market. Entering late June, phased restocking by downstream carbon enterprises largely ended, while the continuous arrival of imported coke at ports and growing expectations of ample port supply significantly quieted spot market trading, and overall petroleum coke prices once again faced downward pressure.

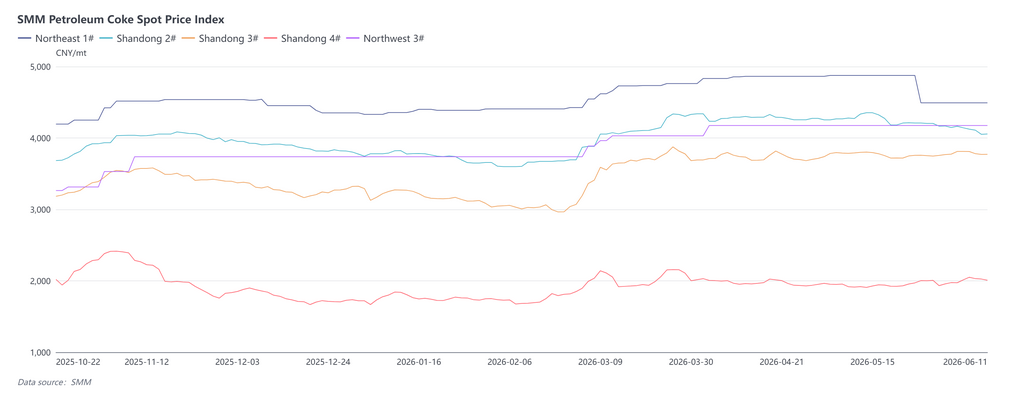

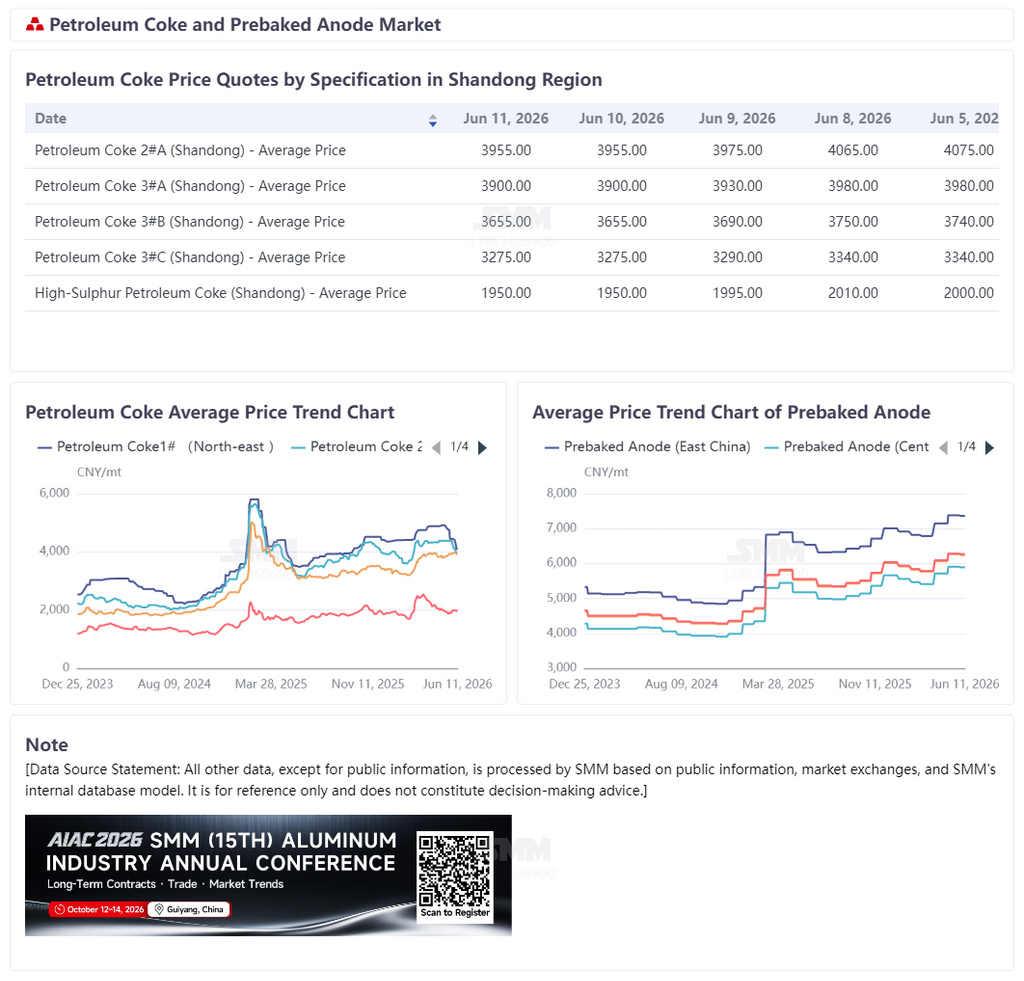

In terms of prices, low-sulphur petroleum coke was the weakest performer in June. At the start of the month, PetroChina lowered low-sulphur coke prices in northeast China generally, and independent refineries saw their low-sulphur coke prices fluctuate downward, with some high-quality resources posting more pronounced price pullbacks. Insufficient purchasing enthusiasm from negative electrode material enterprises and market expectations of increased imported resources were key reasons behind the weakness in the low-sulphur coke market. In contrast, mid and high-sulphur petroleum coke was supported by just-in-time procurement from prebaked anode enterprises, allowing some price recovery in early June, but upward momentum was equally insufficient. SMM’s latest data show that the spot price index for 1# petroleum coke in northeast China closed at 4,491.39 yuan/mt, down 7.88% MoM; the spot price index for 2# petroleum coke in Shandong closed at 4,055.6 yuan/mt, down 3.52% MoM; the spot price index for 3# petroleum coke in Shandong closed at 3,771.42 yuan/mt, up 0.66% MoM; and the spot price index for 4# petroleum coke in Shandong closed at 2,008.26 yuan/mt, up 0.07% MoM.

Supply side, since Q2, domestic refineries have successively entered a concentrated maintenance cycle. Many major and independent refineries conducted maintenance or reduced operating rates on delayed coking units, causing petroleum coke production to decline from earlier levels. In particular, the tightening supply of some mid and high-sulphur petroleum coke resources provided some support to the market. Due to maintenance, domestic petroleum coke supply decreased in phases, and some refineries kept inventories at low levels. However, as downstream demand simultaneously weakened, the favorable impact from supply contraction did not effectively translate into upward price momentum, and the overall market remained focused on digesting inventories and maintaining shipments. Demand side, the prebaked anode industry remained the main pillar of petroleum coke consumption. Currently, China's operating aluminum capacity stays high, and anode enterprises maintain stable overall operations, sustaining rigid demand for petroleum coke. However, raw material inventories at most enterprises are relatively sufficient, and their procurement strategies focus on restocking as needed. In early June, some enterprises restocked intensively, providing periodic support to the market. However, as the month progressed into mid-to-late June, restocking demand gradually subsided, and the procurement pace slowed markedly. Meanwhile, the demand recovery in the anode material industry fell short of expectations, with enterprises maintaining a cautious procurement stance, providing limited support for low-sulphur petroleum coke demand. Other downstream sectors such as graphite electrodes and recarburizers maintained just-in-time procurement, contributing relatively limited incremental demand to the market.

Port side, imported petroleum coke continued to arrive at a high level. According to shipping schedules, imports in June remained sizable, with supplies mainly from the US, Brazil, Russia, Venezuela, Canada, and other countries and regions, covering low-sulphur, mid-sulphur, and high-sulphur sponge coke as well as some shot coke. As imported cargoes gradually arrived and entered market circulation, overall port spot supply was relatively ample. Although some cargoes had yet to be fully released, market expectations for looser supply ahead were growing, exerting some downward pressure on domestic petroleum coke prices.

Overall, the current petroleum coke market dynamics have shifted from supply contraction in mid-month towards demand dominance. The supply boost from refinery maintenance is being offset by increased imports and weakening downstream demand. Market trading activity continued to decline, and some refineries faced increased pressure to sell.

Looking ahead, some refinery maintenance will persist in the short term, but as imported petroleum coke continues to arrive and downstream purchasing interest wanes, the market supply-demand pattern is unlikely to improve significantly. Over the next 1-2 weeks, the domestic petroleum coke market is expected to mainly edge lower amid stability. Low-sulphur petroleum coke prices will face relatively greater downward pressure, while mid and high-sulphur petroleum coke may see limited declines due to rigid demand support from the prebaked anode industry. The overall market will remain in the doldrums.

![Rising Raw Material Costs Squeeze Profits, Aluminum Fluoride Market Stagnant with Stable Prices [SMM Fluoride Salt Weekly Review]](https://imgqn.smm.cn/usercenter/RLjGN20251217171652.jpg)